36Kr Holdings Advances Profitability with Strategic Service Expansion Amid Regulatory and Market Challenges

36Kr leverages its comprehensive New Economy content platform and diversified business services to capitalize on China’s evolving digital economy, while navigating regulatory complexities.

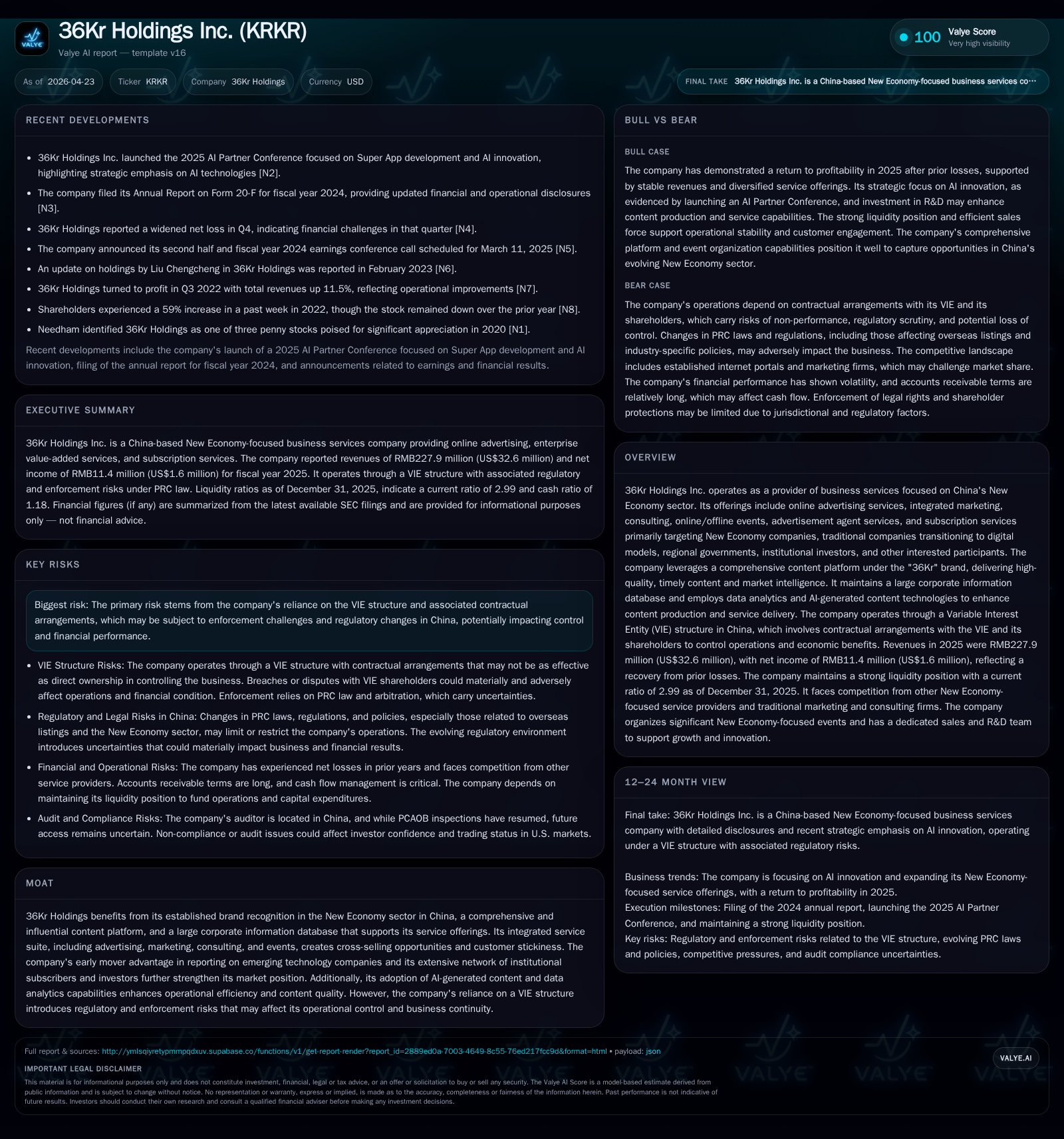

In its latest quarterly filing dated March 17, 2026, 36Kr Holdings reaffirmed its operational control via its Variable Interest Entity (VIE) structure and continues to generate modest profitability after a period of heavy losses. Its business model, anchored in providing integrated advertising, marketing, consulting, subscription, and event services focused on China’s New Economy sector, benefits from strong brand recognition and an extensive corporate information database. Despite competitive pressures from major internet portals and traditional service providers, 36Kr’s cross-selling capabilities and data-driven content production support continued customer engagement. Growth is driven by increasing digitization among regional governments and traditional firms transitioning to new economic models, though regulatory uncertainty around VIE arrangements remains a key risk. Financially, the company improved from net losses to net income of RMB11.4 million in 2025 while maintaining disciplined cost control and sustaining adequate liquidity.

Recent Operating Update

36Kr Holdings Inc.'s latest SEC filing (6-K) dated March 17, 2026 ([S2]) reaffirms that the company continues operating under its established Variable Interest Entity (VIE) structure in China. This report did not announce significant new initiatives but confirmed compliance with filing requirements and ongoing operations continuity. The VIE arrangement remains central to how 36Kr exercises control over its Chinese subsidiaries despite not having direct ownership—an arrangement that carries regulatory risk but currently supports the group’s business continuity.

The annual 20-F filed April 23, 2026 ([S1]) supplements this interim update with richer business model context and detailed financial disclosures through fiscal year 2025, anchoring near-term developments in a broader strategic frame.

Business Model

36Kr operates primarily as a multifaceted service provider targeting China's "New Economy," a term that broadly covers tech-driven startups, innovative traditional enterprises adopting digital transformation strategies, institutional investors focused on emerging markets, and regional governments aiming to digitize economic infrastructure ([S3], [S6], [S17]).

The core revenue streams include:

- Online Advertising Services: Targeted campaigns for both emerging New Economy firms and established companies seeking brand enhancement.

- Enterprise Value-Added Services: Integrated marketing strategies, consulting services facilitating digital adaptation for traditional firms, advertisement agent services including procurement and financing support for clients’ media buys.

- Online/Offline Events: Large-scale summits, forums, and live-streamed industry gatherings providing branding platforms and networking.

- Subscription Services: Institutional subscription offerings (V-club) provide premium market intelligence tailored to sophisticated investors.

Underpinning these offerings is the "36Kr" content platform delivering authoritative insights across technology, consumer sectors, healthcare, new energy, media, entertainment, and more ([S7], [S12], [S16]). The firm employs AI-assisted content production methods combined with extensive corporate data analytics housed in a proprietary information database which augments content relevance and aids in customer targeting ().

Cross-selling capabilities emerge naturally as customers drawn in by advertising or events are often receptive to consulting or subscription products—creating synergy across the product suite. The sales force of specialized personnel versed in New Economy sector dynamics bolsters client acquisition and retention ([S6]).

Crucially for startups benefiting from the platform, 36Kr builds brand visibility early while mature clients receive increasingly sophisticated marketing solutions—establishing a customer lifecycle approach within the New Economy ecosystem ([S3]). Regional governments represent a growing segment wherein digital promotional services aid local economic development policies ([S17]).

Industry Structure and Competitive Position

China's New Economy-focused business services market is fragmented yet intensely competitive. Key competitors include large internet portals such as Sina and Tencent News that offer content-based advertising backed by massive traffic pools ([S7]). Traditional marketing agencies also vie for enterprise value-added service revenues.

However, 36Kr distinguishes itself through:

- Specialization: Focused coverage on New Economy sectors positions it distinctively as an authority rather than a broad generalist.

- Integrated Offering: Uncommon breadth enables synergistic sales across advertising, events, consulting, and subscriptions.

- Data Analytics: Proprietary databases enable tailored content delivery enhancing user engagement.

- Brand Recognition: Early reportage on now-leading startups (e.g., ByteDance) underscores market credibility ([S7]).

- Community Effects: A self-reinforcing ecosystem cultivates loyalty among users spanning startups to investors ().

These moats support reasonably low customer acquisition costs despite competitive pressure ([S1]). Nonetheless, the sector’s rapid evolution means sustaining differentiation requires continuous innovation especially against tech verticals of dominant internet giants.

Growth Drivers and Constraints

Drivers:

- Digital Transformation Demand: Both regional governments increasing investment in digitizing economies and traditional companies seeking New Economy integration underpin service demand growth ([S17]).

- Expanding Investor Community: Institutional subscribers seek improved analytics and curated exposure leading to deeper adoption of subscription services.

- Content Expansion & AI Integration: Enhancing content quality via AI-driven production scales reach without commensurate cost increases ().

- Cross-Selling & Monetization Diversification: Moving beyond advertising into consulting events strengthens revenue resilience.

Constraints:

- Regulatory Uncertainty Surrounding VIE Structure: As contracts enforce control rather than equity ownership directorships pose legal vulnerabilities if PRC authorities change stance or enforcement intensifies ([S15], ).

- Economic Cyclicality & Seasonality: Chinese New Year reduces first-quarter revenues notably due to lowered marketing spend typical in online advertising segments ([S1]).

- Competitive Pressures: Large rival platforms continue innovating requiring constant enhancements from 36Kr's side.

- Accounts Receivable & Capital Controls: Extended payment terms (up to 270 days) require vigilant collection efforts; PRC capital regulations limit offshore fund transfer flexibility ([S4], [S9], ).

What to Watch Next

Key execution points include:

- Continued improvement in monetization mix with emphasis on elevating subscription conversion rates from user base.

- Monitoring regulatory developments affecting VIE contracts and cybersecurity review obligations particularly given recent tightening by CAC authorities ([S15]).

- Business events calendar indicating scale & participation metrics reflecting market influence expansion.

- Cost management trajectories especially across R&D headcount following prior restructurings impacting product innovation capacity.

- Cash flow trends supported by disciplined collection of accounts receivable fortifying operational liquidity amid working capital demands ([S4], [S9]).

Any announcements regarding alternative organizational structures reducing dependency on VIE arrangements or enhanced licensing approvals would be material catalysts.

Financial Profile

Fiscal year ended December 31, 2025 marked a financial inflection point where 36Kr transitioned from substantial net losses into net profitability: net income reached RMB11.4 million (USD $1.6 million), compared with a net loss of RMB140.8 million the prior year ([S1], [F1]). This was driven by stable revenue of RMB227.9 million (USD $32.6 million), nearly flat compared with RMB231.1 million in 2024 amid disciplined expense reduction across all operating categories:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2020 | -43 | -3 | -41 | 335000 | -1050.5% |

| 2019 | -4 | -23 | -3 | 666000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2020 | 1800000 | -3 | -73.4 |

| 2019 | 335000 | -23 | -4.1 |

Source: SEC companyfacts cache [F1]. (Amounts approximate; sourced from [S1], [F1])

Cost controls reduced sales/marketing expenses by nearly 20% year-over-year while administrative costs halved largely due to reductions in personnel-related expenses including credit loss allowances ([S14],[S22]). Capital expenditures remained minimal at RMB0.1 million reflecting the asset-light software platform model ([S19]).

Liquidity was sustained by cash holdings exceeding RMB104 million (~US$15 million), mostly held within PRC subsidiaries compliant with operating currency regulations enabling working capital stability — crucial given accounts receivable terms extending over several months ([S4],[S18],[F1]). The company forecasts sufficient cash runway beyond twelve months without requiring immediate external financing barring acquisitions or unexpected operational demands.

Despite improvements though not yet highly profitable on scale metrics gross profit margins rose to approximately RMB131 million reflecting favorable cost-to-revenue dynamics.[F1]

Conclusion

36Kr stands as a specialized provider embedded deeply within China's fast-evolving New Economy ecosystem leveraging content leadership combined with diverse service verticals tailored for startups advancing through technological maturation stages as well as legacy enterprises initiating digital transformation journeys. The recent quarterly confirmation of ongoing operations under its VIE structure anchors near-term stability amid an uncertain regulatory backdrop that requires vigilance.

Evidenced progress toward consistent profitability supported by stringent cost discipline marks an encouraging inflection poised for further monetization diversification leveraging AI-fueled insights combined with organic community network effects created across entrepreneurial ventures, institutional investors and government entities alike.

Future monitoring should prioritize regulatory regime shifts impacting VIE enforcement or capital flows alongside execution milestones expanding subscription uptake and event scale—the twin engines powering revenue growth curves beyond underlying seasonality constraints inherent to China's marketing cycles.

This analysis reflects publicly available SEC filings as of April 23rd, 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments