.gif)

SMITH & WESSON BRANDS, INC.

SWBI

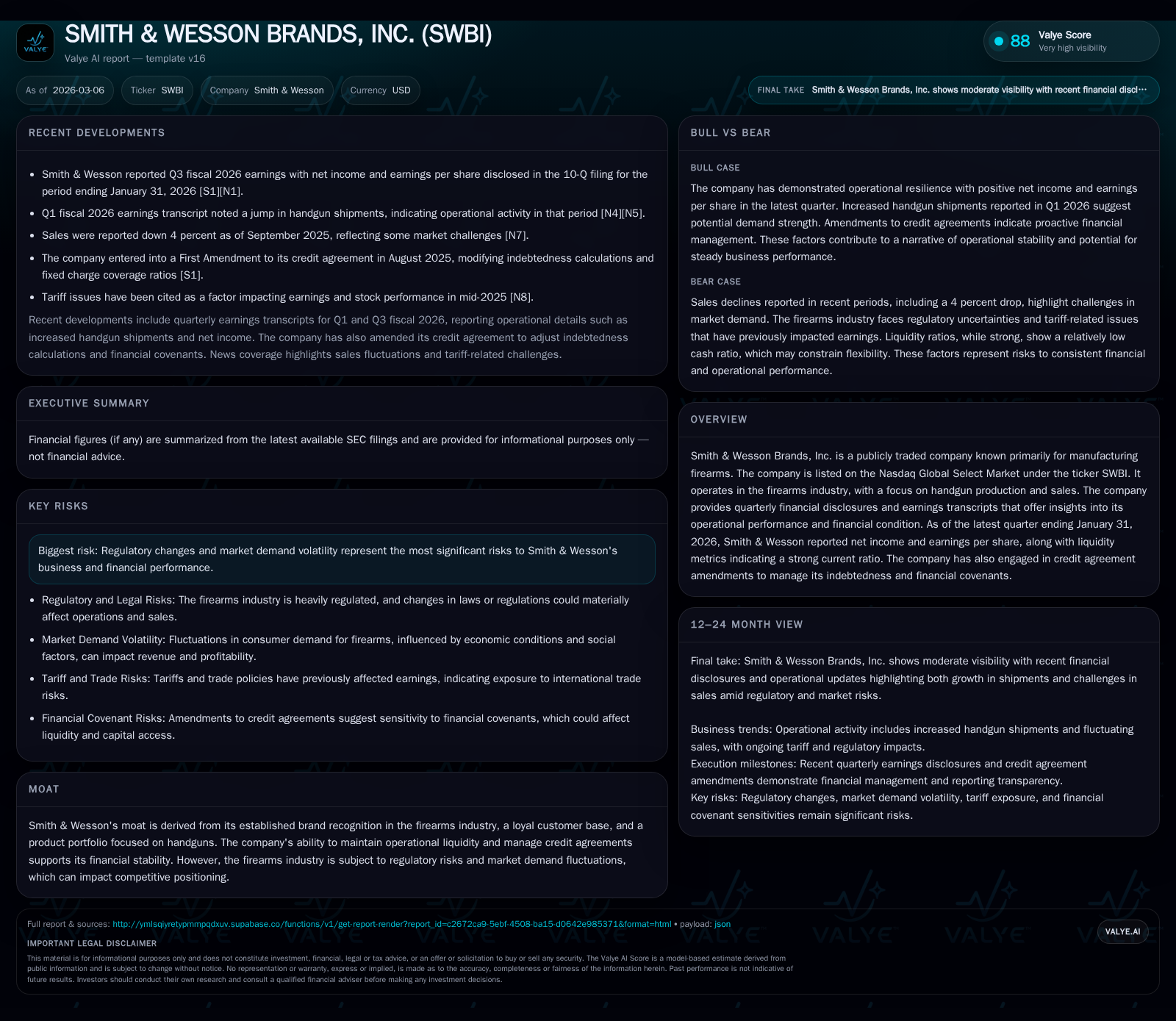

Smith & Wesson Brands, Inc. reported a notable revenue decline of nearly 25% from FY24 to FY25, accompanied by a 47% drop in operating income and a steep net income fall reflecting margin compression and handgun segment volume pressures [F1]. Operating cash flow turned negative in FY25 after years of stability, coinciding with significant capex cuts as management conserves cash amid market uncertainties. The company maintains a robust current ratio of approximately 4.5x as of January 2026, providing a liquidity buffer against regulatory challenges flagged consistently across recent SEC filings [S2-S6]. Capital allocation reflects steady dividend payments and fluctuating buyback activity influenced by credit agreement amendments aiming to preserve financial flexibility [S7-S11]. Key near-term performance indicators remain closely watched in the absence of explicit guidance [N1][N2]. Despite these pressures, Smith & Wesson’s returns on equity stayed low at around 3.6%, reinforcing the capital efficiency headwinds within the current firearm industry cycle [F1].

Valye Articles (auto)

SMITH & WESSON BRANDS, INC. (SWBI)