.gif)

WOODSIDE ENERGY GROUP LTD

WDS

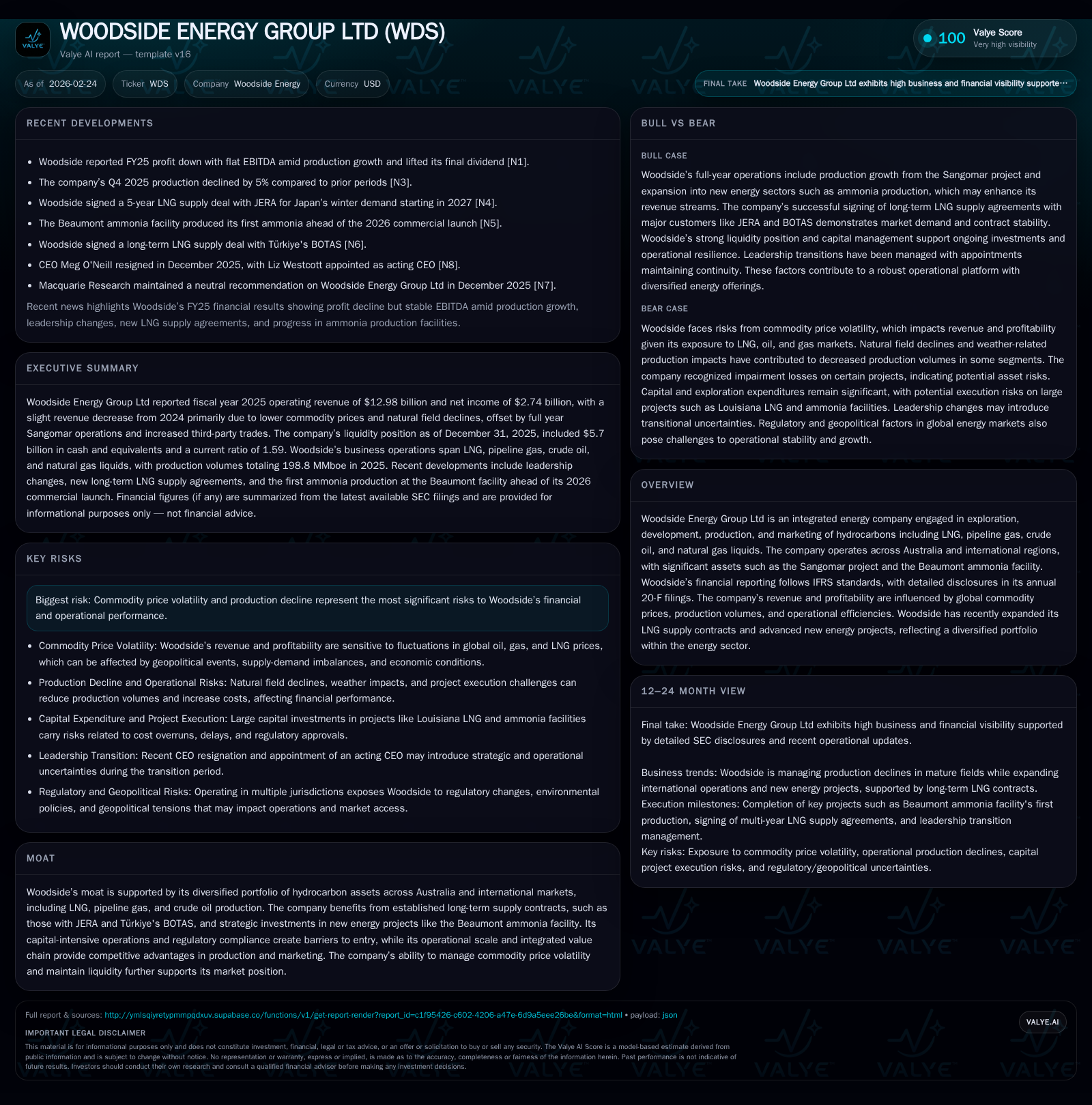

Woodside Energy Group navigated a complex 2025 with modest revenue contraction of 1.5% against increased production, weighed down by lower commodity prices and aging assets in Australia. The company advanced key projects like Sangomar and the Beaumont ammonia facility while strategically managing capital expenditure, which declined by 13% year-over-year. Free cash flow dynamics show robust liquidity supported by joint venture sell-downs and capital contributions, underpinning Woodside’s decision to raise dividends despite a nearly 25% drop in net income. Future growth hinges on successful ramp-up of new energy assets and long-term LNG contracts, balanced against commodity price volatility and natural field declines.

Valye Articles (auto)

WOODSIDE ENERGY GROUP LTD (WDS)