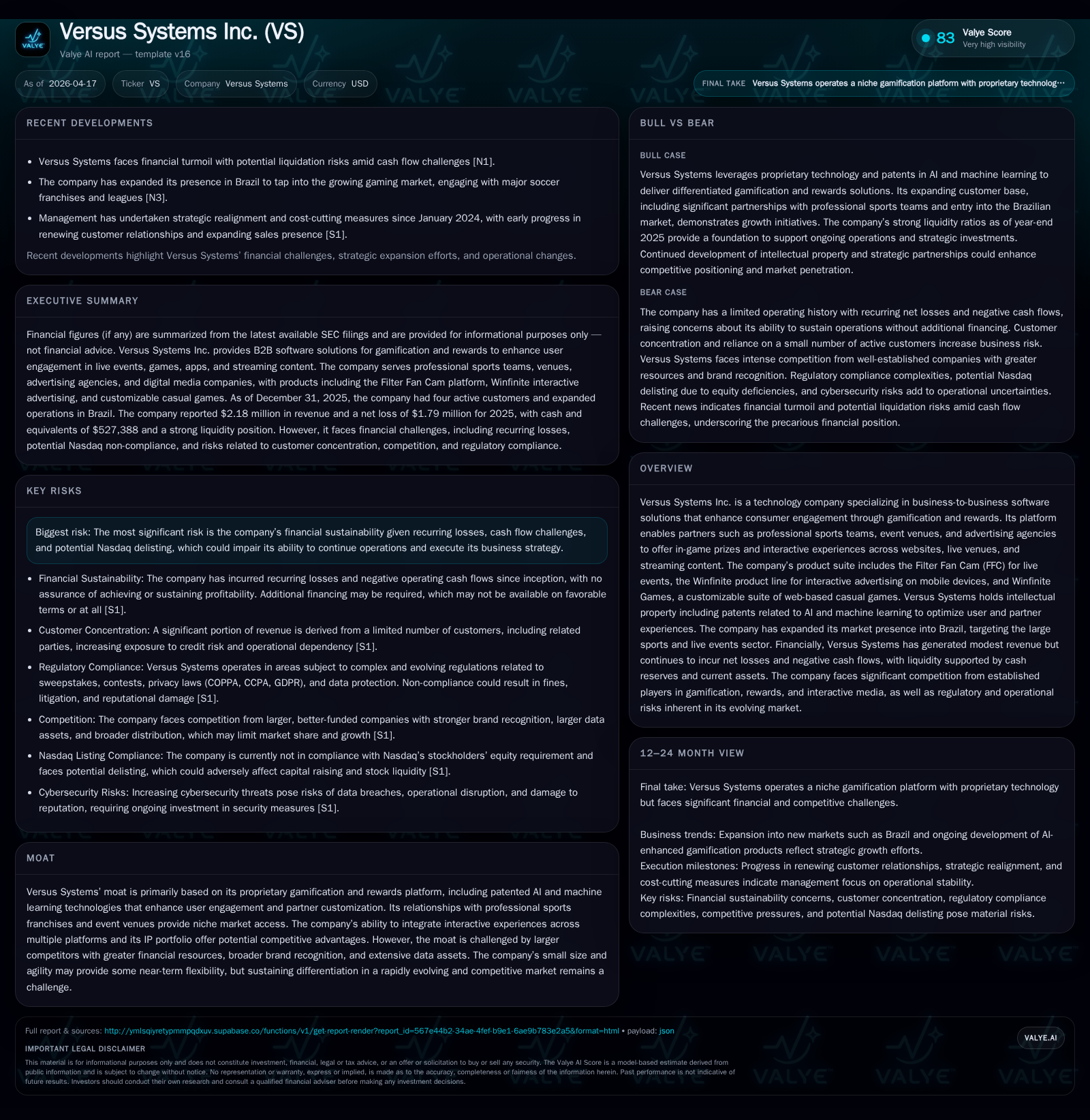

Versus Systems Inc. Struggles to Sustain Momentum Amid Financial Distress and Industry Competition

Versus Systems delivers patented gamification solutions but faces persistent losses and liquidity pressures in a competitive market.

Versus Systems Inc. leverages a proprietary platform anchored in AI-driven gamification and rewards targeting professional sports and live events sectors. The company achieved a remarkable revenue growth surge of over 3700% in fiscal 2025, driven by expansion from two to four active customers and new geographic efforts in Brazil. Despite this top-line improvement, operating losses remain substantial though reduced by about half from prior levels, underscoring ongoing cash burn challenges. Customer concentration risks, intense competition from larger players with integrated data assets, and lack of credit facilities pose significant threats to financial sustainability. Partnerships such as the ASPIS Cyber licensing agreement provide revenue visibility yet underline dependency on few key relationships. Monitoring execution on expansion, additional financing, and Nasdaq listing compliance will be critical going forward.

Revenue Growth Surge: Analyzing FY2025 Breakthrough Against Prior Years

Versus Systems registered a dramatic increase in revenue for fiscal year 2025, reaching $2.18 million compared to just $57,288 in 2024 and $271,169 in 2023 according to [F1]. This translates into a staggering 3711.3% year-over-year revenue growth from FY2024 to FY2025. The operating loss for FY2025 narrowed significantly by approximately 52%, improving from -$4.54 million in FY2024 to -$2.16 million despite still being sizeable relative to scale [F1]. Net income losses similarly shrank by over half but remained negative at -$1.79 million for the most recent fiscal period.

The uptick reflects an increase in active customers from two at the end of 2024 to four by end-2025 [S6], highlighting nascent traction within its targeted verticals such as professional sports teams and event venues. However, the widening top line has yet to translate into profitability or positive operating cash flow—a continuing theme challenging Versus's path toward financial stability.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -2 | -2 | -2 | +3711.3% | +55.7% |

| 2024 | 0 | -4 | -5 | -5 | -78.9% | +61.5% |

| 2023 | 0 | -11 | -6 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -17.6 |

| 2024 | -35.4 |

| 2023 | -88.0 |

Source: SEC companyfacts cache [F1].

Market Niches and Customer Concentration: The Double-Edged Sword

Versus' revenues depend heavily on a limited roster of clients concentrated within specialized segments such as professional sports franchises (e.g., Texas Rangers) and cybersecurity firms like ASPIS Cyber Technologies which became the largest customer in FY2025 [S20]. While this focused client base enables deep customization of Versus' prizing platform tailored for live events and streaming content engagement [S6], it also exposes the company to material risk if these relationships deteriorate or revenues slow.

Management has acknowledged the significance of customer concentration risks impacting cash flows and operational results [S4]. Efforts to diversify through expanding the active customer base have made some early progress—doubling customers within a year—but remain at an embryonic stage given only four active clients reported at year-end 2025 [S6]. The company also seeks growth via geographic diversification with contractor-driven sales teams recently initiated in Brazil—a strategic move aiming at one of the world's largest sports markets [S20].

Still, dependency on few large accounts subject to contract renewals places Versus’ revenue stability under pressure given limited scale or diversified sources [S4]. The collectability of receivables tied to key customers also presents credit risk that management is monitoring carefully.

Gaming Patents and AI Innovation As Competitive Moat

Central to Versus Systems' differentiation strategy is its portfolio of intellectual property that includes patents surrounding artificial intelligence (AI) and machine learning (ML) technologies designed to optimize both user engagement outcomes and partner customization capabilities within its gamification platform [S1][S20][S6]. The core product suite features Filter Fan Cam (FFC), an augmented reality engagement tool employed during live events; Winfinite—a flexible interactive advertising prizing platform usable across mobile devices; and Winfinite Games offering customizable casual gaming experiences tailored for brand integration [S6][S17].

These patented AI/ML claims position Versus favorably against low-tier software developers by creating technology barriers intended to enhance retention of consented first-party data from users while delivering personalized rewards-based interactions for sponsors and media partners [S6]. Nonetheless, these IP advantages are challenged by formidable industry incumbents who deploy significantly greater financial resources toward their own proprietary technologies as well as massive datasets for behavioral insights that far exceed what Versus can harness currently [S15].

The Competitive Arena: Facing Established Giants and Emerging Players

Versus competes against a broad field that ranges from direct prizing platform specialists such as TapJoy and Honey to more generalized pay-to-play rivals like Skillz or DraftKings which monetize primarily from user wagers rather than brand sponsorships [S5]. Beyond this niche competition lies formidable tech giants including Apple, Alphabet (Google), Amazon, Meta (Facebook), Microsoft and Netflix who are steadily expanding interactive content offerings—many integrating AI-powered personalized advertising—that could subsume parts of Versus's market opportunity if they incorporate prizing features leveraging their extensive ecosystems [S5].

This crowded environment elevates challenges for Versus where its relatively small size restricts marketing reach, data resources for training AI models at scale, economies of scope across multiple product lines, and ability to absorb upfront R&D investments required for continuous innovation [S15]. Furthermore, open smartphone app stores enable numerous small competitors or independent developers with minimal overhead capable of launching competing games swiftly creating constant threat from below [S5][S15].

Fiscal Health: Loss Trends, Cash Flow, and Funding Imperatives

Financial discipline trends show signs of incremental improvement as demonstrated by roughly halving operating losses from more than $4.5 million in FY2024 down to $2.16 million in FY2025 while net loss narrowed comparably by nearly 56% year-over-year [F1]. Yet operating cash flow remains deeply negative at around -$2.05 million indicating continued cash consumption exceeding operating income losses given ongoing working capital outlays or investment activities absent explicit capex figures disclosed [F1].

The company's balance sheet exhibits a strong current ratio (~10x), reflecting sound short-term liquidity relative to liabilities; however cash & equivalents stand modestly at less than $530k as of December 31st 2025 risking operational continuity without immediate fresh inflows [F1][N1]. There is no available credit facility providing financing buffer increasing dependence on equity issuances or partnership deals for liquidity support [S12][N1][S23]. Recent entry into a Stock Purchase Agreement with ASPIS Cyber Technologies supplying upfront cash injection around $1.7 million illustrates tactical capital raise efforts linked directly with licensing agreements critical for near-term runway extension [N1][S3].

Persistent recurring losses alongside equity erosion caution that further rounds of dilution may be necessary unless profitable scale is achieved shortly. The SEC filings highlight actual doubt regarding going concern status exacerbated by potential Nasdaq listing non-compliance if stock price or market cap thresholds are breached creating existential pressure for management’s turnaround success [N1][S9][S23].

Strategic Moves in Brazil and Beyond: Expansion Efforts Underway

To reduce geographic concentration risk inherent in limited U.S.-based clients while tapping resilient live-event ecosystems globally, management launched contractor-led sales activities focusing on Brazil starting January 2024 [S4][S6]. Brazil represents a massive untapped market with passionate sports fan bases spanning soccer leagues as well as music festivals that align naturally with Versus' augmented reality filtering tools (FFC) and interactive prizing products tailored for venues or digital campaigns.

Though early results reportedly show promise in establishing new relationships with major soccer franchises and event promoters there remains uncertainty due to workforce downsizing impacting development capacity at headquarters post-cost-cutting measures implemented previously [S4][N1]. Continuity hinges on rebuilding resources efficiently while converting pipeline wins into signed contracts generating meaningful contribution margin.

Within the domestic U.S. market existing client partnerships particularly renewal deals with Texas Rangers alongside growing focus on licensing models (e.g., ASPIS Cyber agreement) help stabilize revenue streams while management pursues technological upgrades through internal R&D projects enhancing platform features supported by IP extensions filed recently around AI/ML uses [S20][S6][S22].

Capital Structure, Allocation, and Shareholder Return Profile

The company's return metrics indicate an approximate negative return on equity near -17.6% measured by net income divided by average equity held predominantly within shareholder funds reflecting ongoing operational deficits but preserved capital base above $10 million as of end-2025 [F1][S24]. There are no declared dividends nor share repurchase programs evidencing liquidity prioritization devoted solely towards operational continuity rather than distributions.

Capital allocation strategy centers on reinvestment into proprietary software improvements alongside cautious geographic expansion attempts balanced against stringent cost control struggles aimed at stemming cash burn rate until break-even scaling is plausible [S24][F1]. Future fundraising paths contemplate equity dilution through private/public offerings or convertible debt issuances under possibly onerous covenant terms constraining corporate flexibility common among early-commercial stage technology firms lacking stable profits or sizable asset collateralization options [S12][N1][S24].

What Comes Next? Key Milestones and Risks Investors Should Monitor

There is no explicit quantitative guidance provided beyond disclosed contractual milestones such as mandatory monthly license fees totaling approximately $165k from ASPIS Cyber commencing April 30th 2025 contracted for twelve months minimum underpinning predictable near-term income portion albeit tied exclusively to one partner's performance [S6][N1][S3]. Key operational benchmarks include:

- Expanding beyond four active customers into further diversified sectors or geographies,

- Renewal success rates on existing contracts particularly with marquee sports franchises,

- Progression against intellectual property development timelines supporting defensibility,

- Securing additional liquidity via equity raises or strategic alliances avoiding undesired dilution,

- Maintaining Nasdaq listing compliance amidst financial distress pressures,

- Adapting rapidly to intensifying competition from large tech incumbents supercharging interactive engagement offerings,

- Navigating evolving regulatory milieus including sweepstakes laws governing prize distribution mechanics affecting product viability internationally.

The principal risk centers squarely on financial sustainability: recurrent operating losses paired with constrained cash flows evoke material uncertainty over continued operations without prompt capital infusion or drastic operational scale improvements highlighted extensively both publicly via news coverage concerning potential liquidation scenarios and internally within annual reports addressing going concern conditions explicitly stated by auditors and management alike ([N1], S9]). Competitive threats compound execution risks as increasingly deep-pocketed adversaries expand overlapping product suites integrating data-driven personalization techniques beyond the scope presently managed internally at Versus ([S5],[S15]). Any failure on multiple fronts simultaneously could force restructuring or cessation inflicting significant capital impairment upon shareholders.

This analysis synthesizes reported financial data ranging FY2023-FY2025 alongside detailed disclosures embedded within SEC filings dated April 15–16th 2026 incorporating recent news coverage published April 17th stressing liquidity constraints confronting Versus Systems Inc.. All presented figures are derived exclusively from cited sources referenced throughout the narrative without extrapolation beyond official statements issued by the company or regulatory submissions.

Readers should note this memorandum aims solely to explore business dynamics comprehensively without inclusion of investment advice or securities recommendations consistent with regulatory standards governing financial research publications.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments