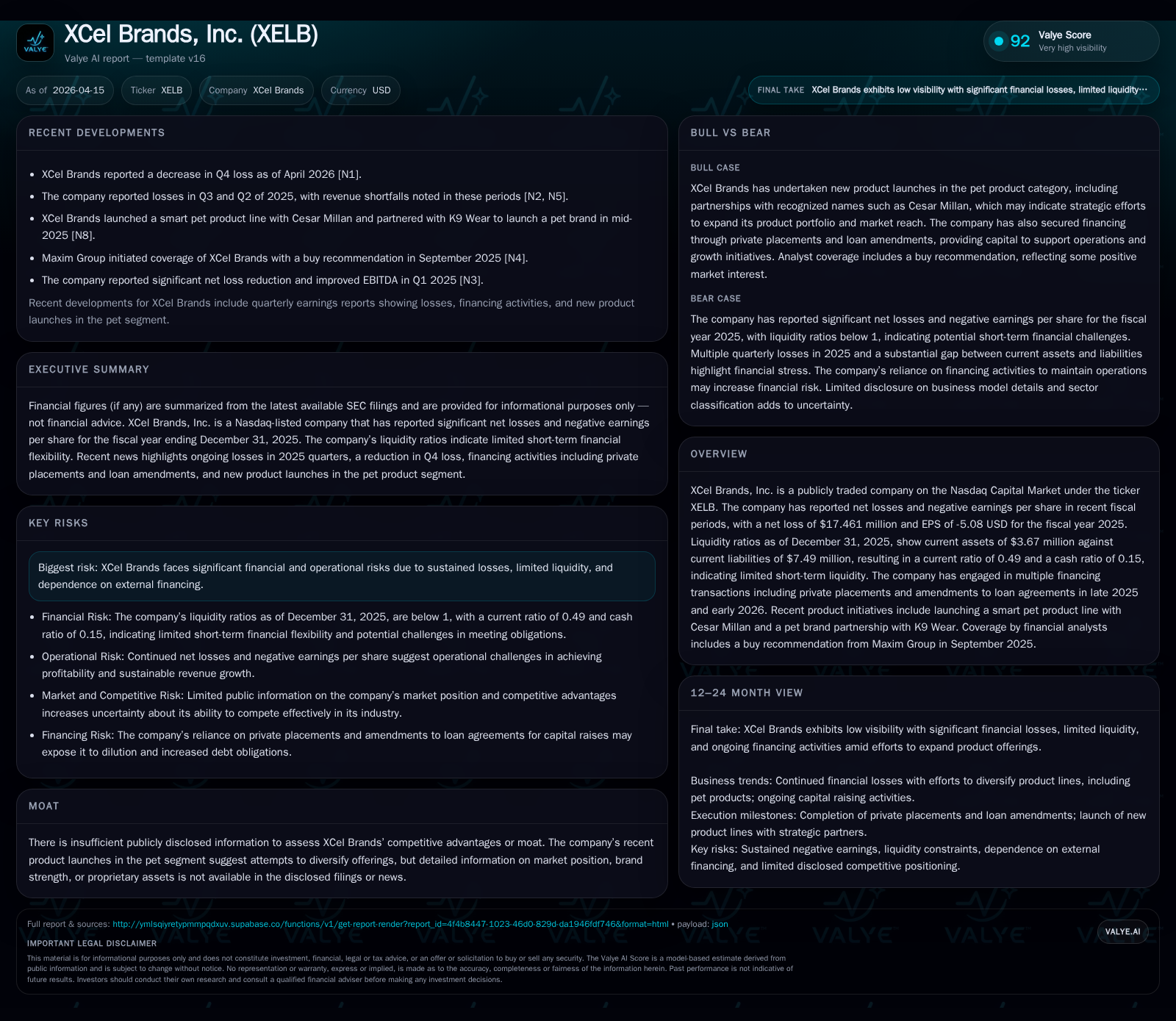

XCel Brands Faces Liquidity Constraints and Mounting Losses Despite New Product Launches

Sustained net losses and limited liquidity hamper XCel Brands’ operational flexibility amid fresh strategic initiatives.

XCel Brands, Inc. reported a net loss of $17.461 million in fiscal 2025, continuing a multi-year trend of substantial operating deficits as the company invests in diversifying with new pet product lines. Its liquidity remains fragile with a current ratio of 0.49 as of year-end 2025, raising concerns about short-term obligations given its reliance on capital raises and loan amendments to sustain operations. The company executed a $15 million equity purchase agreement and successfully closed a $2 million private placement in late 2025 to bolster working capital. While these moves signal an attempt to stabilize finances, absent clear operational milestones or profitability forecasts, the near-term outlook centers heavily on external financing and successful execution of new offerings.

Historical Financial Overview

XCel Brands has endured sizable financial setbacks through recent years, underscored by sustained net losses that have not yet abated. In fiscal year (FY) 2025, the company posted a net loss of $17.461 million [F1], an improvement on the severity seen in prior years but still indicative of deep structural challenges. Operating income remained sharply negative at -$13.231 million, which nevertheless marks some recovery from the preceding two years where operating losses exceeded $20 million annually.

The revenue data available is limited but signals modest growth compared to earlier periods, though absolute scale remains small relative to fixed cost commitments common in brand licensing and product development sectors.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -17 | -7 | -13 | 10000 | +22.0% |

| 2024 | -22 | -5 | -21 | 112000 | -6.4% |

| 2023 | -21 | -7 | -21 | 100000 | -423.9% |

| 2022 | -4 | -14 | -2 | 265000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 204000 | -7 | -97.2 |

| 2024 | 107000 | -5 | -73.6 |

| 2023 | 442000 | -7 | -42.1 |

| 2022 | 442000 | -14 | -5.7 |

Source: SEC companyfacts cache [F1].

Note: Cash flow (CFO), Capex, Equity and Buybacks reflect fiscal-year ending values; buyback data excludes partial historical years.

The operating cash flow trend mirrors ongoing losses with all four years reported showing negative cash from operations (CFO). Capital expenditure is minimal relative to overall expenses — consistent with an asset-light model possibly focused on licensing or branding rather than manufacturing-heavy operations.

Liquidity and Capital Structure

As of December 31, 2025, XCel Brands showed acute liquidity pressures with current assets totaling roughly $3.67 million versus current liabilities nearly double that at $7.49 million [F1]. The resulting current ratio of about 0.49 signals potential short-term funding stress if timely inflows do not materialize or costs are not curtailed.

Cash reserves were particularly lean at approximately $1.15 million year-end [F1], an amount that provides limited buffer against operational volatility or unexpected expenses.

The company secured several amendments to its loan agreements during late 2025 through early 2026 [S8][S9][S17], illustrating ongoing negotiations with creditors aimed at easing liquidity covenants — such as lowering liquid asset requirements from $1 million down to as low as $500,000 linked to collateral allocations — and scheduling prepayments to manage outstanding debt tranches.

Additionally, XCel closed a private placement deal that raised gross proceeds around $2.05 million in December 2025 [S14], netting approximately $1.75 million for working capital after fees and expenses [S20]. This private placement was part of a broader financing strategy including an equity purchase agreement inked in January 2026 with White Lion Capital LLC potentially providing up to $15 million over two years via share purchases under controlled volumes [S19][S12]. Terms restrict total issuance under these agreements so as not to exceed nearly 20% ownership dilution without shareholder approval.

Business Developments and Growth Prospects

Operationally, XCel Brands is attempting diversification beyond core apparel or licensing operations through recent product launches in the pet care segment — an area showing consumer growth trends globally . The company launched a smart pet product line featuring Cesar Millan's branding and established a partnership with K9 Wear for pet accessories [N1]. These moves suggest an attempt to capture emerging niche consumer segments by leveraging celebrity-endorsed products integrated with technology solutions.

However, public disclosures do not include granular performance metrics for these new initiatives nor specific revenue targets or milestones tied to commercialization success [S1]. Without established scale or demonstrable unit economics publicly available, growth prospects remain contingent upon market acceptance and successful execution against entrenched competitors within the broader consumer pet products industry.

Forecasts and Milestones to Watch

XCel Brands has not provided explicit financial guidance or milestone timelines associated with its recent ventures or overall corporate turn-around efforts within the available filings [S1]. Investors and analysts will likely monitor quarterly results for signs of revenue stabilization or improvement from new product lines, along with updates on operational cost management given persistent negative operating margins.

Close attention should also be paid to changes in liquidity status given the high dependence on external capital demonstrated by multiple equity raises and loan covenant adjustments already pursued within a short timeframe.

Returns and Capital Allocation

The company’s return profile remains poor due to sustained losses even amid slight margin improvements: approximated return on equity (ROE) for FY2025 stands near -97%, defined by dividing net income ($-17.46M) by shareholders’ equity ($17.96M) [F1]. This figure highlights negative shareholder value generation over recent periods.

Free cash flow (FCF), inferred as operating cash flow minus capex, was roughly negative $7 million for FY2025 — consistent with continuing high operational burn rates despite cost-cutting attempts [F1].

Capital allocation activities include modest share repurchases totaling around $204,000 during FY2025 compared with prior years’ activity below $500,000 [F1]. These buybacks represent a minimal use of available capital given pressing liquidity needs and ongoing financing requirements.

No dividends have been declared or paid over the reviewed period reflecting constrained cash availability.

Risk Factors Summary

XCel Brands faces profound risks principally stemming from financial instability characterized by repeated large net losses and weak liquidity ratios limiting operational flexibility without further capital infusions [S4]. The dependence on frequent financing rounds subjects the company to dilution risk while regulatory restrictions within purchase agreements constrain financing options.

Commercial execution risk surrounds its nascent expansion into smart pet product lines where competitive dynamics are intense, requiring effective brand leverage and innovation to gain traction absent clear protective moats disclosed publicly.

Legal contingency risk is noted without prominent active litigation disclosures but remains an intrinsic consideration for companies managing intellectual property-based brands in fast-moving consumer sectors [S4][S6].

Conclusion

XCel Brands remains challenged by sizeable cumulative losses and strained liquidity despite efforts to strengthen its balance sheet through variable debt repricing and fresh equity financing completed over late 2025 into early 2026. The company's modest revenue base paired with continued operating deficits underscores the uphill path toward profitability.

Recent strategic shifts into technology-enhanced pet products provide some directional growth avenues but lack disclosed commercial validation or near-term forecasts necessary for a comprehensive re-rating from current financial distress levels.

Close monitoring of quarterly performance updates will be essential to assess whether operational discipline combined with fresh capital deployment can translate into sustainable improvement.

This analysis is based solely on publicly available filings and news sources as of April 15, 2026, without any recommendations or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments