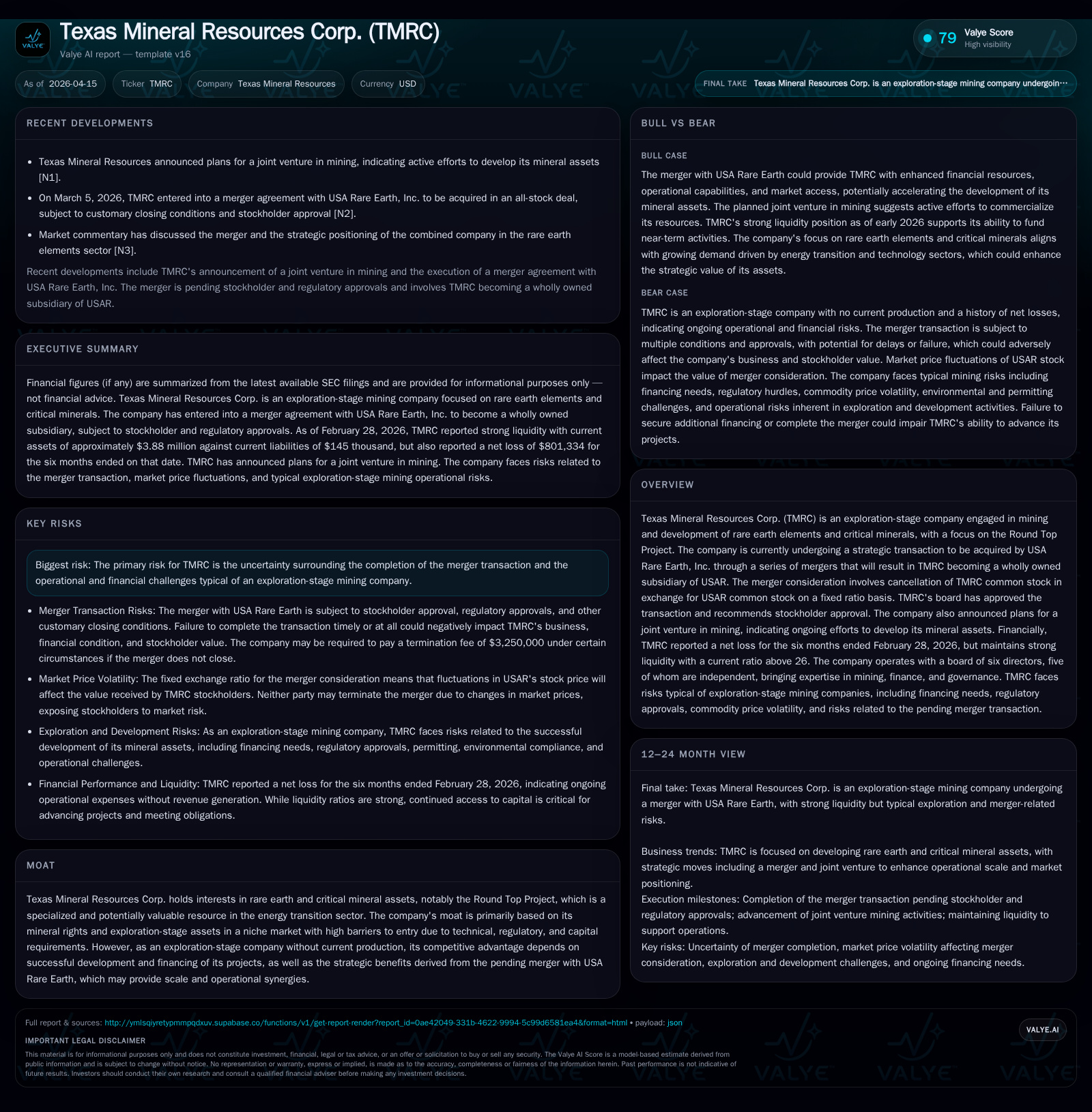

Texas Mineral Resources’ Merger with USA Rare Earth Hinges on Strategic Synergies and Project Development Risks

TMRC’s exploration-stage focus and strong liquidity contrast with operational losses and merger completion uncertainties.

Texas Mineral Resources Corp. has consistently operated at a loss while maintaining a robust liquidity position, reflecting its exploration-stage status centered on the Round Top Project. The pending acquisition by USA Rare Earth, Inc. represents a major strategic shift aimed at scaling operations and potentially unlocking value through combined resources and expertise. Key risks remain from the uncertain closing of the merger and the challenges inherent to advancing an undeveloped rare earth mining project.

Historical Performance

Texas Mineral Resources Corp. (TMRC) operates primarily as an exploration-stage mining company focused on rare earth elements critical for energy transition technologies. Over recent fiscal years, TMRC's financial performance has been characterized by consistent operating losses reflective of its early-stage development profile. For instance, operating income was negative $1.21 million in FY2025, marking a deterioration compared with negative $954 thousand in FY2024 [F1]. Net losses followed a similar trend with nearly $1.93 million reported in FY2025 versus $833 thousand in FY2024.

Operating cash flow also remained negative throughout this period (-$897 thousand in FY2025), underscoring continued cash consumption largely attributed to exploration and preliminary development activities at their flagship Round Top Project [F1]. Capital expenditures are modest but increased significantly relative to earlier years indicating incremental investments into project-related assets. TMRC's equity base contracted due to cumulative losses but still stood above $1 million as of FY2025 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -2 | -1 | -1 | -132.1% |

| 2024 | -1 | -1 | -1 | +67.9% |

| 2023 | -3 | -1 | -3 | +10.7% |

| 2022 | -3 | -3 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -186.6 |

| 2024 | -96.4 |

| 2023 | -179.9 |

| 2022 | -95.4 |

Source: SEC companyfacts cache [F1].

Note: Capex data is available sporadically and is omitted here where not comparable.

TMRC's liquidity remains exceptionally strong on a current basis with a current ratio exceeding 26 as of February 28, 2026—an unusually high figure denoting considerable liquid assets relative to short-term liabilities [F1]. The company held roughly $789 thousand in cash and equivalents alongside nearly $3.9 million in total current assets against liabilities approximating $145 thousand [F1]. This liquidity buffer reflects both cash inflows from financing activities and conservative working capital management amid ongoing exploration expenditures.

Future Growth Prospects

The Round Top Project is TMRC's core asset and serves as the foundation for its growth prospects. Located in Texas, this asset contains rare earth elements alongside other critical minerals essential for green technology applications [N2][S13]. However, the project has yet to proceed beyond exploration stages into commercial production. Profitability depends heavily on successful development milestones including securing adequate financing and navigating complex environmental and regulatory approvals.

Strategically pivotal is the announced merger with USA Rare Earth (USAR), an entity aiming to consolidate complementary rare earth mining operations [N1][S3]. Upon closing—the timing of which is subject to standard deal conditions such as stockholder approval and Nasdaq listing clearance—TMRC would become a wholly owned subsidiary within USAR’s organizational structure [S12]. This integration may offer operational synergies through resource pooling and enhanced technical expertise.

However, growth remains capped by several factors: uncertainties around merger completion could delay integration benefits; critical mineral markets are volatile; developmental risks abound such as title issues regarding surface rights; and competition for capital persists given the sector's capital-intensive nature [S13][S14]. Since the merger consideration involves fixed share conversion ratios without market price adjustments before closing [S2], shareholder value realization could be affected by external equity market fluctuations.

Further underpinning future growth will be TMRC's plans for joint ventures targeting mining operations advancement [N2]. These collaborations may serve dual purposes: sharing financial burdens for project execution and leveraging partner expertise.

Forecasts and Expectations

Explicit forward guidance from TMRC is limited due to its exploration-stage status and ongoing corporate transaction [S8]. Stakeholders should monitor proxy filings related to the merger process for milestone updates such as special meeting outcomes and regulatory notices [S11]. Key deal conditions that affect timeline include effectiveness of USAR’s registration statement on Form S-4 for issuance of consideration shares alongside customary due diligence findings [S12][S18].

Absent standalone operational forecasts from TMRC post-merger reporting will consolidate under USAR’s disclosures implying a transition phase where separate financial detail for TMRC diminishes. Market participants will thus need to track both USAR’s operational progress post-acquisition as well as overall rare earth demand dynamics.

Returns and Capital Allocation

In line with many junior mining companies focused on resource definition rather than production or dividends TMRC has not issued dividends or repurchased shares recently [F1][S22][S26]. Capital allocation has prioritized funding exploration programs primarily via convertible debt issuances evidenced by previous unsecured notes conversions totaling roughly $1.1 million during 2025 [S9][S10][S27]. Management compensation remains modest reflecting lean headcount focused on project advancement rather than broader operational infrastructure [S23][S24].

Free cash flow remains negative consistent with industry norms at this development stage—FY2025 showed negative free cash flow approximating $932 thousand after factoring operating cash outflows less capital expenditure [F1]. Return on equity is deeply negative (~-187%), attributed to net losses exceeding book equity values indicative of ongoing investment cycles predating revenue generation [F1].

Risk Profile

Significant risks center around typical junior mining challenges compounded by transactional uncertainties. The fixed conversion ratio merger exposes shareholders to equity market volatility risk while awaiting deal closure [S8][S14]. Operationally potential delays or cost overruns linked to the Round Top Project’s development including permitting challenges or title disputes may impact feasibility [S13][S6]. Financing needs persist especially if joint ventures do not materialize promptly or at expected scales.

Additional litigation risks arise from enforcement proceedings possibly associated with merger non-completion or competing bids given restrictions imposed on alternative transactions under the merger agreement [S4][S20]. Resource market dynamics fueled by geopolitical tensions impacting supply chains also represent external unpredictabilities influencing critical mineral sector outlooks [S7][N3].

Conclusion

Texas Mineral Resources Corp.’s trajectory illustrates the classic profile of an ambitious rare earth junior miner advancing a strategically significant mineral asset toward commercial viability amid broader industry consolidation. Elevated liquidity provides some runway security; however persistent operating losses underscore dependence on successful financing events including completion of the complex merger with USA Rare Earth to scale development efforts effectively.

Investors and stakeholders aligned with TMRC’s prospects should prioritize monitoring regulatory approvals related to the merger transaction alongside milestones tied to joint venture progress and Round Top Project permitting developments. Additionally understanding impacts from macroeconomic factors governing rare earth element markets is essential given their outsized influence on future valuation potential.

This report synthesizes available public disclosures without providing investment advice or specific recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments