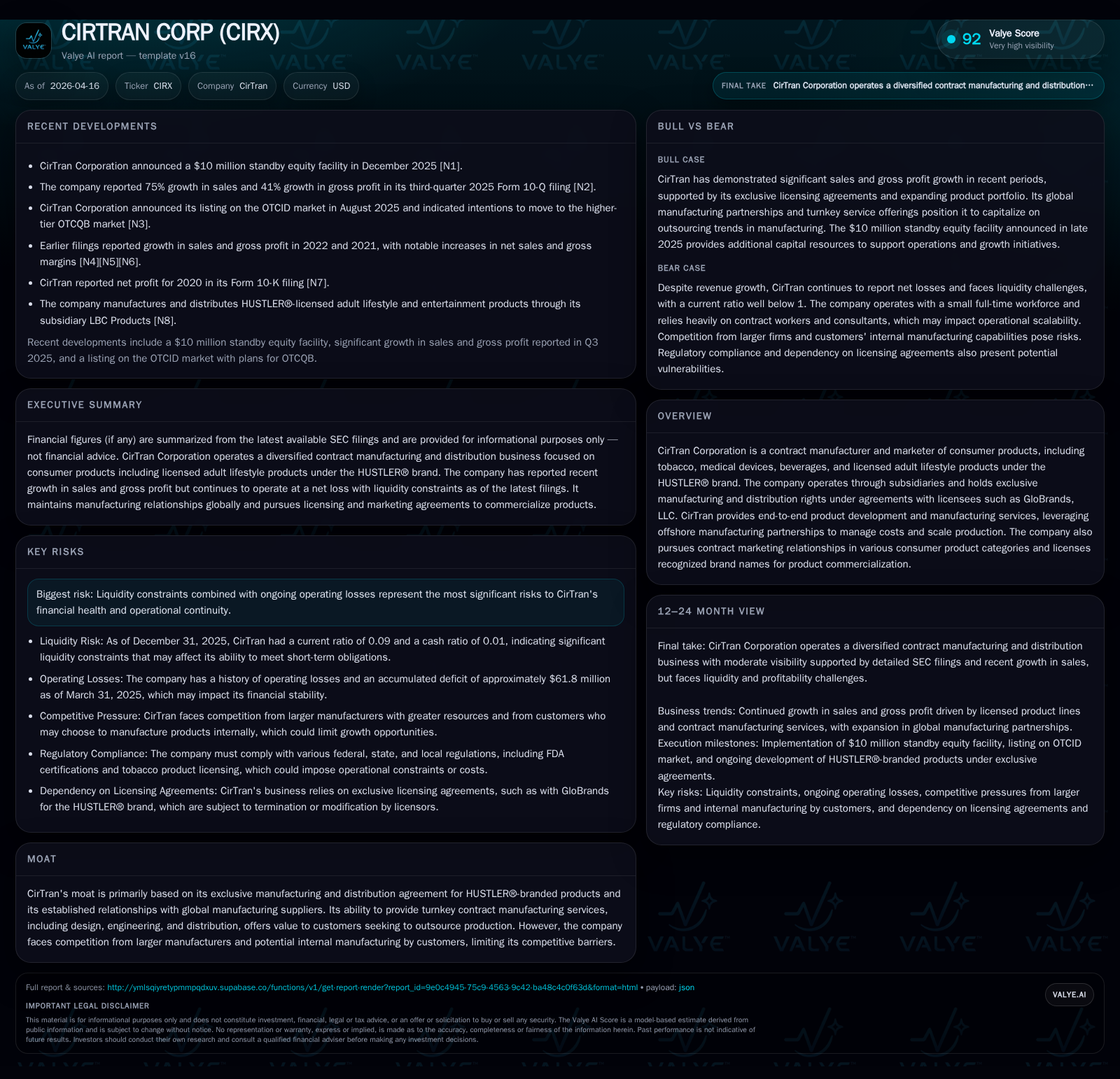

CirTran Corp Battles Operating Losses and Severe Liquidity Constraints Despite Diverse Consumer Product Portfolio

CirTran operates contract manufacturing and marketing across several consumer categories but faces cash flow stress and negative equity.

CirTran Corporation leverages exclusive licensing agreements, such as for HUSTLER®-branded products, combined with offshore manufacturing partnerships to serve global consumer markets. Despite diversified product lines spanning tobacco, medical devices, and beverages, the company has consistently recorded operating losses over recent years, accompanied by a mounting working capital deficit and negative shareholders’ equity. Liquidity remains strained due to high current liabilities relative to assets, with operating cash flows deteriorating sharply in 2025. The business model focuses on turnkey contract manufacturing solutions supported by licensing and marketing relationships, yet ongoing losses and debt servicing obligations pose significant continuity risks.

Business Overview

CirTran Corporation (CIRX) operates as a contract manufacturer and marketer of diverse consumer products including tobacco-related items, medical devices such as condoms, beverages, and lifestyle goods licensed under brands like HUSTLER®. It executes its activities primarily through three subsidiaries: LBC Products, Inc., CirTran Products Corp., and CirTran - Asia, Inc. Their footprint spans over 50 international markets supported by established global manufacturing partnerships to optimize costs and scale production capacity [S1][S3][S4].

The company’s manufacturing strategy is anchored in offering "Concept to Consumer" end-to-end solutions—covering design, engineering, procurement, manufacturing, packaging, branding, distribution, and order fulfillment—with an emphasis on turnkey contracts that relieve clients from heavy capital investment and inventory management burdens [S3][S5]. Offshore production facilities in Asia help CirTran maintain cost competitiveness.

Since 2020, CirTran has focused on developing HUSTLER®-branded products under an exclusive contract with GloBrands LLC for manufacturing and distribution rights—a partnership granting access to a globally recognized adult lifestyle brand ecosystem comprising retail outlets and clubs worldwide [S1]. This niche licensing confers some competitive advantage but does not constitute a wide moat given aggressive industry competition.

Historical Financial Performance

Financial trends reveal persistent operating losses despite generating revenue through product deliveries (notably from HUSTLER® lines) and product development service contracts recognized upon milestone achievements. The company follows ASC 606 for revenue recognition reflecting control transfer upon contractual acceptance [S6][S12][S18].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -1338174 | -129723 | +73.3% | |

| 2024 | -3 | -46354 | -550739 | 8414 | -112.9% |

| 2023 | 20 | -72607 | -14917 | 8414 | +1450.7% |

| 2022 | -2 | 159304 | -522283 | 3798 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 2.8 | |

| 2024 | -54768 | 10.8 |

| 2023 | -81021 | -93.2 |

| 2022 | 155506 | 3.6 |

Source: SEC companyfacts cache [F1].

Operating income improved in 2025 compared to prior years but remained negative at approximately $-130K [F1].

Net income followed a similar pattern with a reduced loss of $-701.6K in FY25 compared to a much larger loss in FY24 ($-2.6M), albeit still substantially negative [F1].

Operating cash flow deteriorated dramatically to $-1.34M in FY25 from near-breakeven levels previously suggesting worsening working capital or operational inefficiencies [F1].

Shareholder equity remains deeply negative (> $25M deficit), indicating accumulated losses have eroded book value significantly over time.

The company's current ratio is extremely low (approx. 0.09), highlighting severe liquidity pressure as current liabilities overwhelmingly exceed current assets at year-end 2025 [F1].

Revenue Drivers and Margin Pressure

CirTran earns revenue mainly through sales of manufactured products delivered under contractually binding agreements plus fees from product development services recognized at predetermined milestones such as design completion or prototype acceptance [S6][S25].

Revenues have been relatively stable but not growing materially—product delivery revenue totaled approximately $1 million for the nine months ended September 30, 2025 [S18]. The modest scale reflects niche markets rather than mass volume.

Margins are pressured by royalties paid quarterly based on sales to licensors (e.g., for licensed brands), regulatory compliance costs particularly for tobacco imports and FDA certifications related to medical devices like condoms [S1][S15], plus expenses related to managing international supply chains.

Future Growth Prospects

Growth opportunities hinge largely on expanding the reach of licensed brand products like HUSTLER®, leveraging turnkey offshore manufacturing capabilities to attract more OEMs seeking cost-effective outsourcing solutions across various consumer categories including health & beauty aids, fitness equipment, kitchenware, and tobacco alternatives .

Strategic partnerships with retailers could open new distribution channels as CirTran simultaneously offers itself as the preferred manufacturer for partner-produced goods—a reciprocal priority arrangement aiming to mutually boost sales growth [S3].

However growth risks include intense competition from large-scale contract manufacturers capable of providing more extensive resources or internalization of manufacturing functions by customers seeking cost savings or proprietary control. Regulatory complexities—for tobacco excise tax compliance or FDA approvals—could delay or limit new product introductions [S15].

Capital Structure and Liquidity Analysis

CirTran's capital structure is heavily leveraged with notes payable totaling roughly $733K alongside convertible debentures amounting near $2.67 million secured by company assets due mostly by April 2027; accrued interest significantly adds burden (over $400K accrued interest on notes plus millions associated with convertibles) [S8][S11].[F1]

The company's monthly operating cost was estimated around $35K excluding an additional $50K monthly interest expense; cash equivalents were negligible at reporting dates with no liquidity cushions noted [S8][S12].[F1]

Negative working capital exceeding $22 million due to accumulated payables and related party advances puts stress on day-to-day cash needs against limited liquid resources as of late-2025 year-end accounts.[F1]

Operating cash flow turned strongly negative in FY25 reflecting continuing operational cash burn despite attempts at streamlining operations [F1].[S13]

There are no reported material legal litigations currently active; management continues focusing on raising liquidity likely through external funding sources though success cannot be assured given past credit profiles and ongoing losses [S15][S24].[F1]

Returns and Capital Allocation Considerations

The approximate return on equity based on last fiscal net loss against deeply negative equity results in a positive ROE figure due solely to losses shrinking the base denominator; this should not be interpreted as signaling profitability improvement but rather accounting effect from deficits.[F1]

Capital expenditures remain minimal (approx. $8K annually), consistent with the outsourcing business model relying on third-party manufacturers rather than heavy owned asset investments.[F1]

No dividends or buybacks have been reported given the persistent deficits.

Sector Context Analysis (non-company-specific)

Within contract manufacturing targeting consumer goods sectors—especially those involving regulated products like tobacco or medical devices—the trend toward outsourced turnkey services continues driven by OEMs' desire for flexibility amidst supply chain volatility and rising regulation complexity. However small players like CIRX face uphill battles scaling margins amid competition from large incumbents with integrated supply chains or vertically controlled competitors.

Successful firms often combine technological innovation in production processes with solid branding/licensing deals that provide stable revenue streams beyond commodity manufacturing fees.

Watchpoints for Investors & Stakeholders (Analysis)

- Follow quarterly updates on cash flow trends closely given liquidity constraints.

- Monitor progress toward securing additional capital or refinancing convertible debt maturing in coming years.

- Assess developments expanding HUSTLER® product portfolio or other licensing arrangements impacting top-line growth potential.

- Gauge competitive positioning improvements versus internal manufacturer threats or larger contract manufacturing players.

- Observe regulatory changes affecting import licenses or FDA certification hurdles raising operational risk profiles.

- Track any restructuring efforts targeting cost reduction especially accruing payroll/interest expenses.

Conclusion

CirTran Corporation presents an intriguing case featuring diversified product involvement combined with niche licensing strengths balanced against persistent financial distress manifested through continuous operating losses and acute liquidity challenges. The firm’s future hinges on its ability to stabilize cash flows while expanding its licensed brand offerings via efficient turnkey manufacturing amid tough industry dynamics. Maintaining operational continuity will likely require material external financing or strategic shifts.

Disclaimer: This report is for informational purposes only and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments