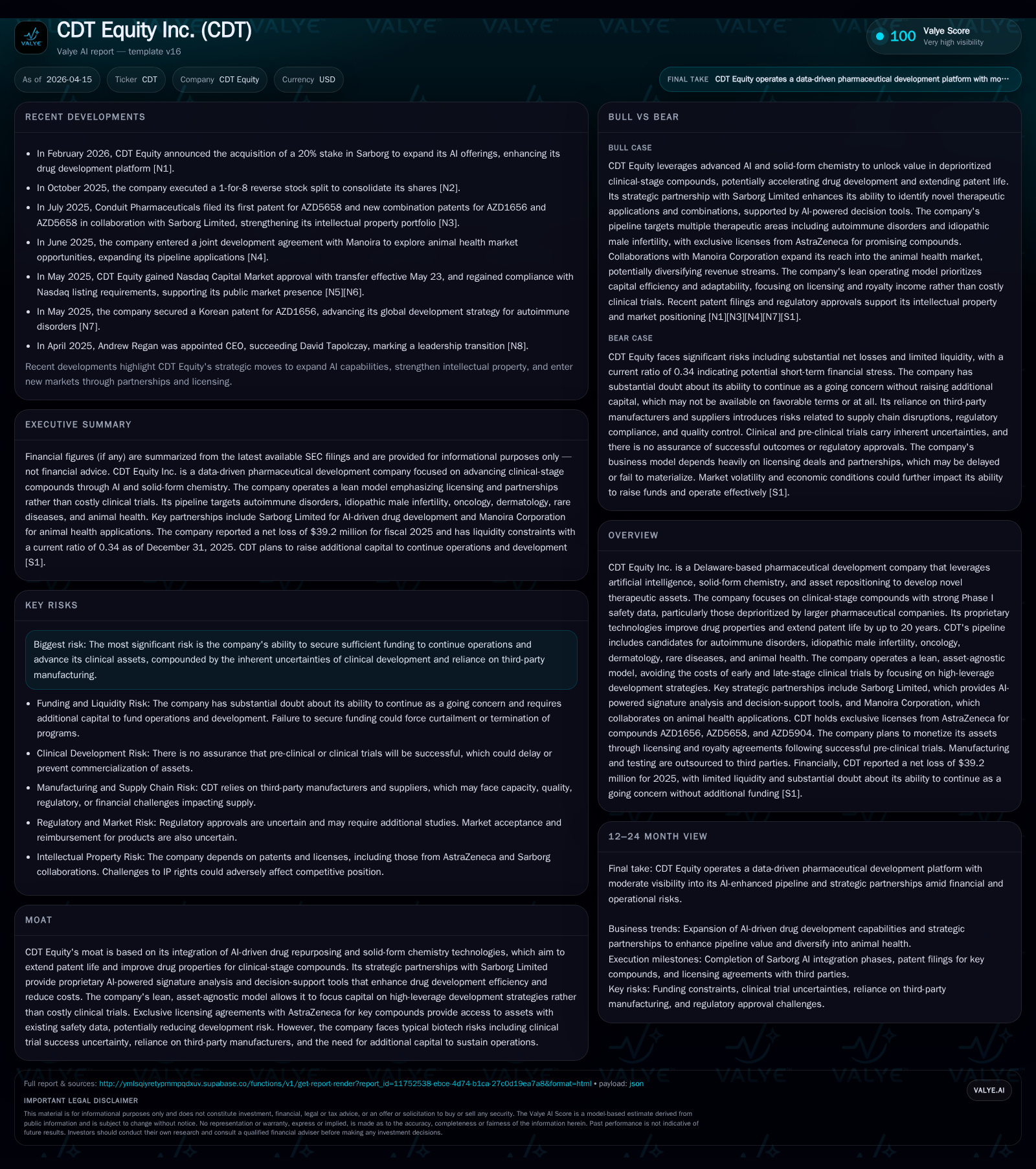

CDT Equity Inc. Faces Intensified Losses and Liquidity Constraints While Leveraging AI-Enhanced Drug Repositioning

CDT Equity Inc. pursues AI-driven pharmaceutical asset development but confronts mounting financial losses and significant liquidity pressures.

CDT Equity Inc. operates a novel pharmaceutical development platform integrating artificial intelligence, solid-form chemistry, and asset repositioning focused on clinical-stage compounds underexploited by larger pharma companies. The company has incurred growing net losses, with operating income deteriorating sharply from -$15.4 million in 2024 to -$36.8 million in 2025, driven by increased R&D and operational expenditures [F1]. Its capital base is constrained, evidenced by a current ratio of just 0.34 and limited cash reserves as of end-2025 [F1]. CDT’s growth depends heavily on advancing key clinical assets through preclinical and early-phase trials and forming licensing partnerships. The firm’s lean, asset-agnostic model prioritizes capital efficiency but will require significant funding to sustain progress [S1][S22]. Risks include clinical trial uncertainties, intellectual property disputes, regulatory challenges, and continued reliance on third-party contractors [S1][S19][S20]. Monitoring upcoming clinical milestones and capital raising activities will be critical for evaluating CDT’s trajectory in a competitive biotech environment.

Company Overview

CDT Equity Inc., a Delaware corporation, specializes in pharmaceutical development that integrates artificial intelligence (AI), solid-form chemistry innovations, and strategic repositioning of clinical-stage compounds deprioritized by larger pharmaceutical companies. The company's proprietary technologies aim to improve drug properties such as bioavailability and stability while potentially extending patent protection by up to 20 years via co-crystallization methods developed at its Cambridge facilities. Additionally, CDT collaborates with Sarborg Limited to apply AI-driven signature analysis for identifying new therapeutic applications and optimizing candidate selection.

Operating an asset-light business model focused on early- to mid-stage compounds with favorable Phase I safety data but often neglected by originators, CDT seeks high-leverage returns while minimizing capital-intensive late-stage trial expenditures by pursuing third-party licensing deals following early clinical validation [S1][S22].

Historical Financial Performance

CDT Equity has sustained escalating operating losses over the past four years as shown below:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -39 | -16 | -37 | -120.3% |

| 2024 | -18 | -10 | -15 | -3227.5% |

| 2023 | -1 | -8 | -5 | -234.2% |

| 2022 | 0 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 547.1 |

| 2024 | 262.1 |

| 2023 | 117.1 |

| 2022 | -9.3 |

Source: SEC companyfacts cache [F1].

The steepening losses reflect increased investment in research & development alongside operational expenses without revenue generation—no significant revenues are expected until successful clinical validation of core assets occurs [F1][S1]. Operating cash flows remain negative annually due to these expenditures.

Liquidity is constrained; as of December 31, 2025 the company held approximately $1.5 million in cash against $12.8 million in current liabilities yielding a current ratio of about 0.34. This indicates acute near-term funding requirements to maintain operations beyond initial trial stages absent substantial financing or equity dilution [F1][S22]. The accumulated deficit totaled $68.3 million at year-end 2025.

Pipeline and Growth Prospects

Key developmental assets include:

- AZD1656: A glucokinase activator targeting autoimmune disorders with indications refined via AI insights.

- AZD5904: An irreversible inhibitor of human myeloperoxidase under investigation for idiopathic male infertility.

Additional candidates address oncology indications (e.g., AZD5658), dermatology conditions, rare diseases, and veterinary health through collaborations such as with Manoira Corporation. These assets primarily originate from AstraZeneca-derived compounds possessing Phase I safety data advantages [S1][S22].

The company's strategy emphasizes out-licensing or strategic partnerships post Phase II proof-of-concept milestones to transfer commercialization risk externally rather than conducting costly late-stage trials internally [S15].

However,

- CDT depends on successful capital raises amid volatile funding environments.

- Clinical trial progress relies heavily on third-party CROs whose performance impacts timelines.

- Regulatory acceptance of endpoints and demonstration of safety/efficacy remain uncertain.

- Intellectual property disputes—including a patent challenge by St George Street Capital over the AZD1656 co-crystal formulation—pose material risks [S14][S19].

Risk Factors Summary

Risks outlined include:

- Funding Risks: Sustained negative cash flows necessitate ongoing financing without near-term commercial revenues [S1][S22].

- Clinical Trial Execution: Reliance on third-party contractors introduces risks related to compliance with Good Clinical Practice standards; failure may cause delays or require repeat studies [S9][S20].

- Intellectual Property Litigation: Patent ownership disputes threaten exclusivity essential for market protection; ongoing litigations carry multi-million dollar liabilities impacting financial stability [S14][S19].

- Regulatory Challenges: FDA review complexities combined with healthcare pricing reforms such as the Inflation Reduction Act add uncertainty even post approval [S6][S10][S16].

- Manufacturing Dependencies: Outsourced production requires adherence to cGMP standards; disruptions may delay product availability or trigger recalls [S25].

- Liquidity Concerns: Negative equity position coupled with low current ratio highlight urgent fundraising needs critical for sustaining operations [F1][S22].

Capital Allocation and Returns

As a pre-commercial entity focused on development:

- No dividends or share repurchases have been declared or executed.

- Return metrics such as ROE are distorted due to negative equity; an approximate calculation yields an anomalous figure (~547%) resulting from the negative denominator rather than sustainable profitability [F1].

- Free cash flow remains negative consistent with investment-heavy operations; FY2025 operating cash flow was approximately -$15.6 million indicating no internal capacity for shareholder returns without external financing support.

Capital deployment priorities will likely continue emphasizing pipeline advancement while managing operational expenses within constrained liquidity parameters.

Outlook Analysis

While CDT does not provide explicit financial guidance:

- Near-term catalysts include progression through preclinical validations informed by AI analytics and completion of Phase II trials for lead candidates AZD1656 and AZD5904.

- Successful out-licensing or partnership agreements post-clinical data readouts remain central to converting pipeline assets into revenue streams sustaining further development efforts without excessive dilution.

- Resolution of intellectual property disputes will be pivotal for securing exclusivity benefits crucial to market positioning.

- The availability of capital from public or private markets amidst biotech funding volatility is critical given current liquidity shortfalls.

Conclusion

CDT Equity Inc.'s integration of AI technologies with pharmaceutical formulation science positions it uniquely within the drug development sector focused on unlocking value from deprioritized assets. However, the company's financial profile reflects typical pre-commercial biotech challenges marked by escalating losses, deteriorating liquidity, and execution risks tied to regulatory approvals, litigation, and partner dependencies. Its lean asset-light approach mitigates some costs but does not eliminate the fundamental need for sustained external financing aligned with pipeline progress milestones. Stakeholders should closely monitor clinical milestone achievements, fundraising initiatives, and resolution of material litigation as key indicators shaping CDT's path toward potential value creation.

This analysis is based solely on publicly available SEC filings including recent Form 10-K reports; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments