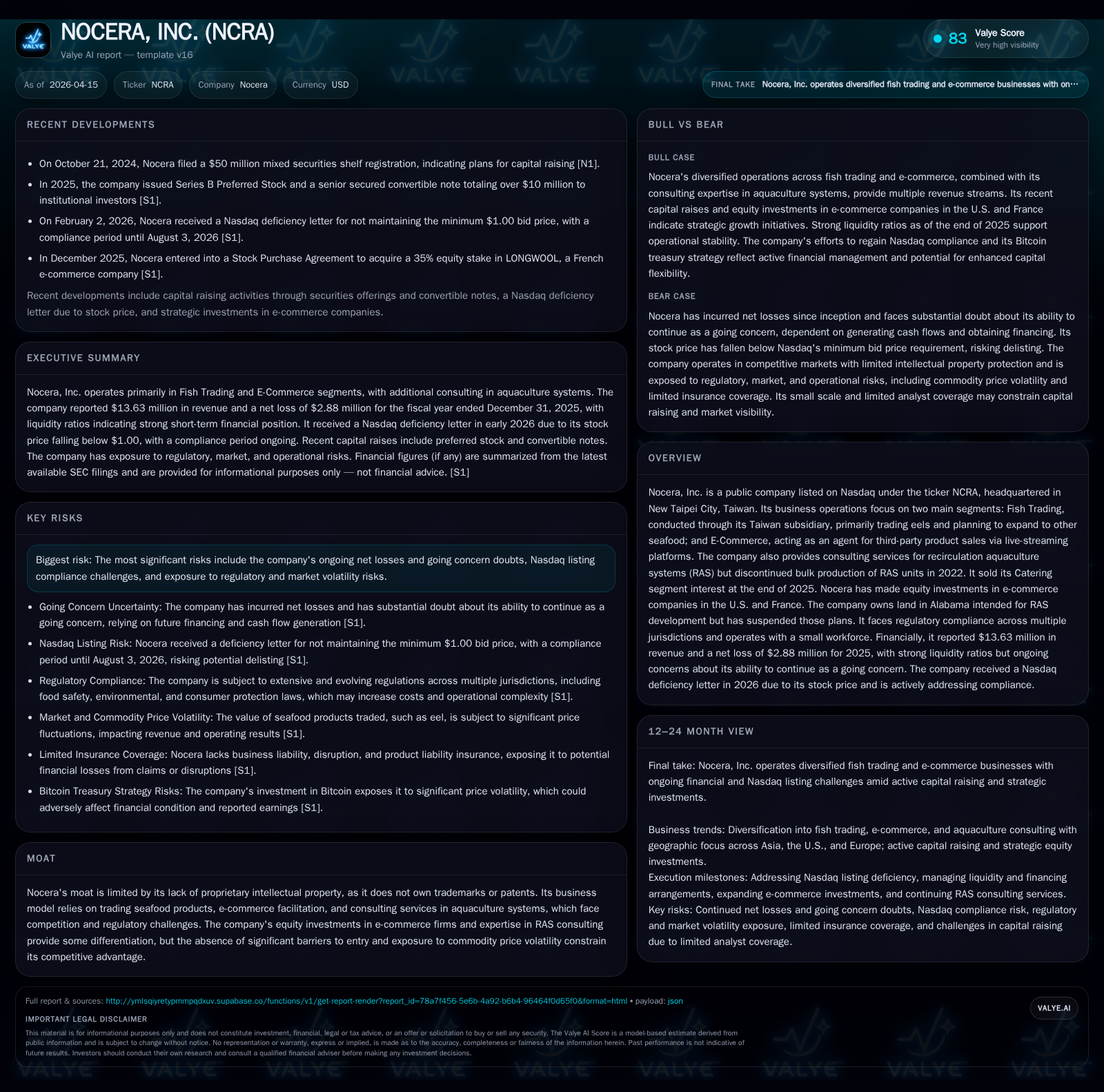

Nocera’s Diversified Operations Face Critical Profitability and Capital Allocation Questions

Nocera's business diversification contrasts with its ongoing losses and complex capital management challenges.

Nocera, Inc. has rapidly expanded revenues primarily through its Fish Trading and E-Commerce segments but continues to report significant operating losses and negative cash flows. The company has shifted strategically by discontinuing bulk RAS production and exiting catering while investing in equity stakes in e-commerce ventures in the US and France. Despite a strong liquidity position supported by a substantial current ratio and a $2 million Bitcoin treasury purchase, the firm faces persistent regulatory pressures, Nasdaq listing compliance risks, and questions around sustainable profitability. Ongoing operational restructuring and capital allocation decisions will be critical indicators to watch as Nocera attempts to stabilize and grow.

Evolution of Nocera’s Revenue Streams

Nocera’s top-line growth trajectory demonstrates a striking increase from a modest revenue base under $5 million in FY2018 to approximately $13.63 million in FY2025 [F1]. This expansion largely reflects ramped-up trading activities within its Fish Trading segment—predominantly eel sales conducted via its Taiwan subsidiary—as well as growing commission revenues derived from its E-Commerce live-streaming agent model administered through the Xinca division [S1][S5][S18]. The company noted targeted geographic markets for these segments extend across Taiwan, Japan for fish trading, and the United States and France for e-commerce facilitation [S5][S14]. Despite this impressive revenue scaling—over a 27,000% increase year-over-year when comparing FY2019/FY2020 figures to FY2025—the top-line growth has failed to translate into profitability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | -3 | -22.3% | ||

| 2024 | -2 | -2 | -301071 | 956 | +45.1% |

| 2023 | -4 | -1 | 857870 | +10.9% | |

| 2022 | -5 | -2 | 0 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 653.5 | |

| 2024 | -1575665 | -56.3 |

| 2023 | -1919721 | -134.9 |

| 2022 | -1771551 | -79.7 |

Source: SEC companyfacts cache [F1].

Table: Selected historical financial metrics extracted from [F1]. Note capex scaled down sharply post-2023.

Segment Performance and Shifts in Business Focus

Nocera’s main operational thrusts consist of two distinct segments: Fish Trading and E-Commerce. The Fish Trading segment is routed through Nocera Inc. Taiwan Branch (NTB), focusing primarily on eel procurement and sales [S1][S18]. Handling includes order intake followed by coordination for harvesting and inspection before delivery. NTB is also planning to expand into other seafood varieties such as tilapia and milkfish [S1]. This segment caters mainly to customers in Taiwan and Japan [S5][S14]. On the other hand, the E-Commerce segment operates on an agency basis without inventory control; it generates commission-based revenue through third-party product sales on live-streaming platforms predominantly targeting US and French markets [S1][S14]. Equity investments into e-commerce companies based in these countries during FY2025 underscore management's intent to grow this business line via partnerships rather than direct product control.

Additional legacy operations included recirculation aquaculture systems (RAS), where Nocera engaged in design consultation but ceased bulk manufacturing/sales as of late 2022 while continuing consulting services [S1][S18]. RAS represents advanced land-based fish farming facilities emphasizing controlled water reuse for environmentally friendly high-density cultivation — a technical niche that leverages Nocera’s expertise but involves significant regulatory compliance hurdles [S6]. Furthermore, the Catering segment was divested at year-end 2025 to streamline operations further [S1][S14]. This strategic pruning underscores a corporate pivot toward core competencies amid structural losses.

Financial Results: Operating Dynamics and Profitability Trends

Despite Nocera's revenue growth surge up to nearly $13.6M by FY2025 ([F1]), profitability remains elusive. Operating income data reveals persistent losses: the latest reported operating income stands at approximately negative $301k for Q3-2024 with continuing net losses amounting to $2.88 million for the full year ending December 31, 2025 [F1][S1]. The net income trend shows deterioration from fiscal years prior—though improving slightly relative to deeper losses like the roughly $4.81M deficit recorded in FY2022—indicating ongoing margin compression possibly related to commodity price volatility typical of seafood trading markets [S21] and operating costs related to multi-jurisdictional regulation.

Cash flow analysis confirms this pressure: operating cash flow has worsened considerably by more than 60% year-over-year by end-2025 reaching negative $2.58 million with capital expenditures nearly halted compared to prior years [F1]. This liquidity drain highlights sustainability challenges absent operational breakeven or fresh capital infusions.

Capital Allocation: Treasury Crypto Investment and Liquidity Management

In a notable departure from conventional treasury strategies common among small-cap public firms facing cash burn issues, Nocera allocated $2 million toward purchasing Bitcoin across two tranches completed in January 2026 ([12 BTC at around $83k average price]) representing approximately one-seventh of their reported cash reserves ($7.95 million as of December 31, 2025) [F1][S12]. This move suggests an experimental approach seeking asset diversification amid operating losses rather than immediate business reinvestment.

The firm's liquidity remains comparatively healthy on a balance-sheet basis with a current ratio exceeding twelve times—driven by current assets of about $8.27 million against current liabilities near $0.69 million as of end-FY25 [F1][S19]. However, there is no record of dividends or share buyback programs given ongoing capital constraints ([S10]). Recent financings include issuance of preferred equity carrying dividend obligations (~9% annually starting October 2025) alongside senior secured convertible debt totaling $8 million issued late-2025 with interest payable monthly until maturity in late-2027; these raise questions about future leverage and capital structure impacts on shareholder value [S27].

Regulatory Complexity and Operational Constraints

Operating across multiple jurisdictions including Taiwan, China, the US, France alongside emerging markets such as South Africa exposes Nocera to an array of regulatory frameworks affecting privacy laws; trade compliance; aquaculture environmental regulations; product safety; licensing for fish farms; labor laws; marketing conduct governed by entities like the U.S. Federal Trade Commission; plus securities exchange regulations under Nasdaq scrutiny [S4][S6][S11][S29].

Environmental standards pertinent to RAS operations impose rigorous water quality requirements along with local government approvals for land usage and operating permits—increasing operational overheads and risk exposure particularly relevant as the company balances consultancy-led RAS business while having exited unit manufacturing [S6]. Moreover, ongoing Nasdaq listing compliance is threatened due to failure maintaining minimum closing bid prices (<$1/share over consecutive periods), though management has obtained an initial relief window until August 3rd, 2026 to remedy via stock price improvement or reverse split actions [S3][S10].

These combined regulatory demands add layers of complexity that may constrain Nocera’s operational agility as well as inflate compliance costs.

Future Outlook: Opportunities, Risks, and What to Monitor

While explicit forward guidance is absent given the company's emergent nature ([N/A]), several future growth avenues present themselves cautiously. The planned expansion of seafood offerings beyond eel could broaden trading revenue streams if market acceptance proves adequate [S18]. Continued development of RAS consulting may offer steady services income leveraging niche technical expertise despite bulk production termination.

Investors should closely monitor:

- Nasdaq compliance progress including share price trends or corporate actions addressing listing deficiencies;

- Ability of the e-commerce segment’s equity ventures in foreign markets to generate meaningful returns or synergies;

- Operational break-even achievement including narrowing negative operating margins;

- Potential currency fluctuations impacting Taiwan-based revenues due to reporting currency disparities (USD reporting vs NT dollar functional operations);

- Regulatory changes affecting aquaculture facility approvals or import/export restrictions impacting supply chains.

Persistent risks from commodity price swings inherent in seafood trading alongside macro uncertainty regarding geopolitical tensions involving Taiwan necessitate prudent surveillance moving forward [S24][S25].

Investor Returns and Balance Sheet Health

An analysis based on available data reveals significant challenges dampening investor returns. Though reported ROE appears anomalously strong at approximately +653% for FY2025 when comparing net loss against negative equity valued near -$441k at year-end—a distorted figure due to accounting anomalies—the broader picture shows sustained accumulated deficits exceeding $26 million implying deep-rooted historical shareholder capital erosion [F1][S19]. Negative free cash flow exceeding $2.58M after minimal capital expenditure further underscores operational funding requirements outpacing internal generation capacity.

Liquidity strength provides short-term buffer but continued reliance on external financing evidenced by preferred stock issuance with associated dividend commitments alongside expensive convertible debt may pressure long-term solvency without operational turnaround improvements or accretive investment successes [S19][S27].

Summary: Strategic Resilience Amid Structural Challenges

Nocera’s journey illustrates a stark juxtaposition: robust revenue scaling borne from diversified operations met head-on with persistent profitability deficits compounded by operational complexity spanning fragmented international regulations and evolving corporate strategy pivots away from longstanding verticals like RAS unit manufacturing toward advisory roles complemented by live-streaming e-commerce commissions.

The sizable cryptocurrency acquisition signals experimental treasury management amid constrained conventional capital deployment options—an unorthodox step implying management’s search for alternative store-of-value mechanisms amidst loss generations.

Supportive liquidity ratios mask underlying negative cash burn trends emphasizing the imperative need for successful execution on growth initiatives coupled with stringent cost management if viability is to improve before refinancing constraints narrow further.

Ongoing surveillance is warranted around Nasdaq compliance milestones alongside developments within core fish trading expansions plus ROI visibility from international e-commerce partnerships to properly gauge whether diversification efforts will translate into sustained financial health or merely complicate an already delicate capital framework.

This analysis relies solely on facts extracted from publicly available SEC filings dated April 15th, 2026 ([F1], [S#]) without speculative forecasts or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments