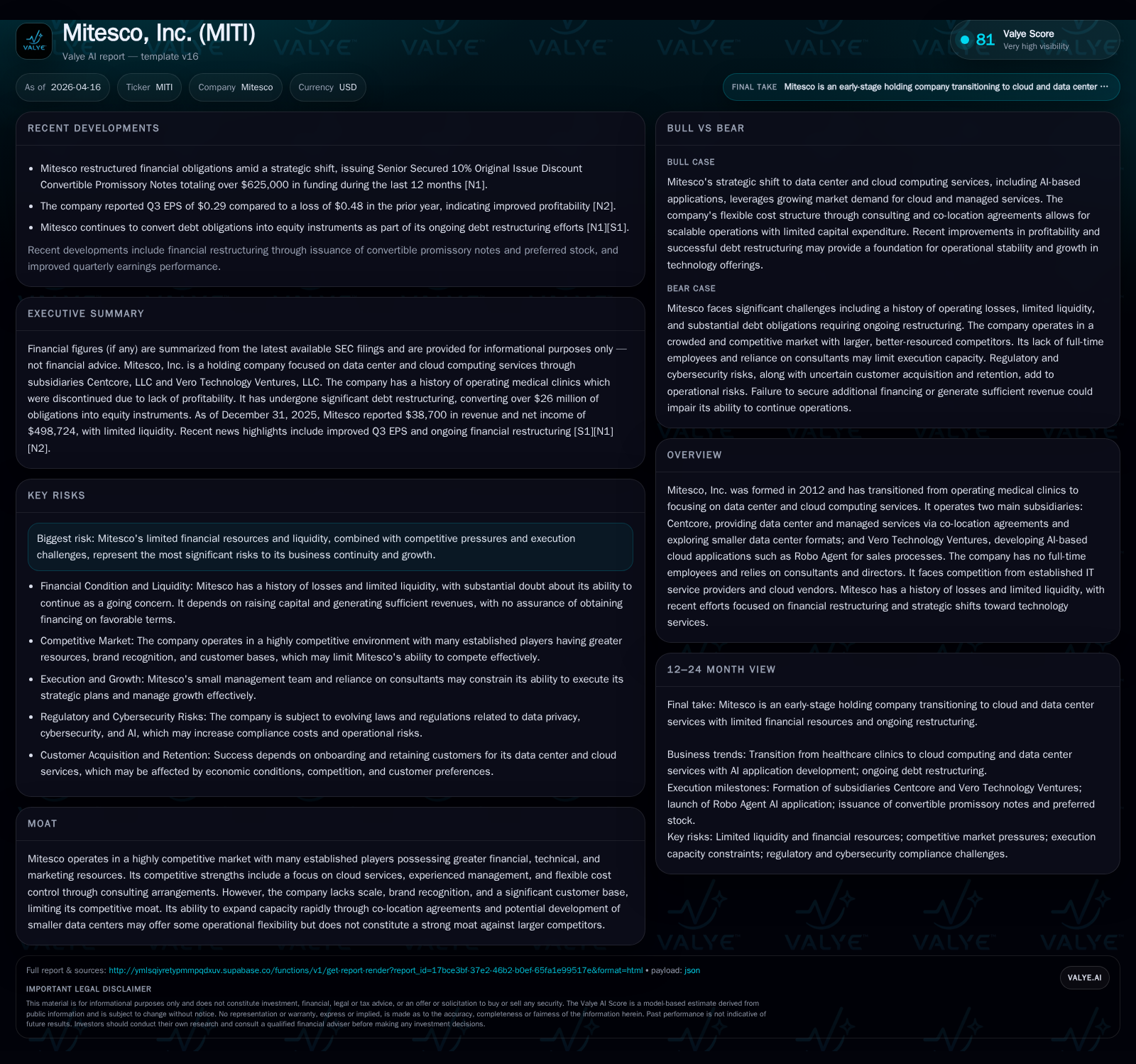

Mitesco, Inc. Navigates Strategic Pivot Amidst Financial Headwinds and Market Challenges

Transitioning from healthcare clinics to cloud and data center services, Mitesco confronts significant liquidity constraints and competitive pressures.

Mitesco, Inc. ceased its unprofitable clinic operations in late 2022 and reoriented its business towards technology services through subsidiaries Centcore LLC and Vero Technology Ventures LLC, focusing on data center co-location and AI-enabled cloud applications. Despite this strategic pivot, the company continues to face severe financial challenges including minimal revenues, substantial operating losses, and a highly leveraged balance sheet. Debt restructuring initiatives have converted large portions of legacy liabilities into equity instruments, easing immediate cash demands but diluting shareholders. The firm operates in a fiercely competitive IT services market where success depends on effective customer acquisition, product rollout, and managing regulatory and legacy legal risks.

Company Overview and Historical Performance

Founded in 2012, Mitesco initially operated medical clinics under The Good Clinic brand until closing all such operations by late 2022 due to persistent losses [S1], [S16]. Following this exit, the company pivoted toward technology services through two subsidiaries formed in June 2024: Centcore LLC offering data center co-location services including partnerships with existing facilities like one in Melbourne, Florida; and Vero Technology Ventures LLC developing AI-powered cloud applications such as the "Robo Agent" for sales process automation [S1], [S16].

Financially, Mitesco’s transition is reflected in its revenue trajectory peaking at $690K in 2022 before sharp declines post-clinic shutdown [F1]. FY2023 showed zero revenue during shutdown transition. Revenues modestly resumed but fell from $43.7K in FY2024 to $38.7K in FY2025 (-11.4%) [F1]. Operating losses remain significant but improved from -$18.2 million (2022) to -$1.9 million (2025) [F1]. Notably, net income swung positive to $498K in 2025 primarily due to non-operating or accounting-related gains linked to debt restructuring activities [F1]. Operating cash flow stayed negative at approximately -$702K, with free cash flow also negative given minimal capital expenditures [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 38700 | 0 | -1 | -2 | -11.4% | +119.9% |

| 2024 | 43700 | -3 | -1 | -1 | +81.2% | |

| 2023 | 0 | -13 | -1 | -3 | -100.0% | +42.6% |

| 2022 | 690534 | -23 | -5 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -2.1 |

| 2024 | 9.5 |

| 2023 | 94.3 |

| 2022 | 121.4 |

Source: SEC companyfacts cache [F1].

Note: Net income recovery reflects non-cash adjustments related to debt restructuring.

Liquidity Position and Capital Structure

Mitesco faces severe liquidity challenges with current liabilities exceeding $19 million versus current assets of approximately $132K as of December 31, 2025 — yielding an extremely low current ratio (~0.01) [F1]. This imbalance primarily arises from legacy obligations tied to shuttered clinic operations including lease settlements and default judgments totaling roughly $3.4 million plus other vendor claims documented in court rulings [S7], [S14].

To mitigate these cash demands amid limited operational revenues and capital access, the company has undertaken extensive debt restructuring since FY2024 converting over $26 million of prior obligations into Series A Amortizing Preferred Stock shares and restricted common stock at negotiated valuations [S13], [S27]. These exchanges reduce immediate cash outflows but substantially dilute existing shareholders.

Further financing includes multiple bridge notes issued since late 2025 as Senior Secured Convertible Promissory Notes bearing original issue discounts near 10%, interest only payable upon default; these notes are secured by subsidiary assets [S8], [S9], [S12], [S18], [N1]. Such financing supports ongoing development efforts but provides limited runway.

Equity remains deeply negative (-$23.5 million), reflecting accumulated deficits exceeding invested capital despite recent accounting gains masking underlying operational losses [F1]. Operating cash flows remain negative primarily due to continued development costs without sufficient subscription revenue scale.

Business Model Transition & Competitive Landscape

Mitesco's pivot places it within a highly competitive IT sector featuring dominant cloud providers like AWS/Microsoft/Google; colocation specialists such as Equinix; and global systems integrators including Accenture and IBM offering broader consulting services [S4], [S24].

The company's competitive strengths include a flexible cost model relying heavily on consultants rather than full-time employees alongside initiatives targeting niche cloud applications powered by AI via Vero Technology Ventures.

However, disadvantages include limited scale or brand recognition restricting pricing power or ability to secure long-term contracts typical of enterprise clients who require extensive global infrastructure footprints. Many incumbents maintain entrenched client relationships via legacy contracts or integrated service offerings making customer acquisition challenging for a smaller entrant [S4], [S24].

Centcore’s model leverages partnerships with existing data centers worldwide enabling rapid capacity expansion at low capital expense while providing managed services for hybrid cloud migrations—a strategy reflecting broader industry trends favoring edge data centers close to end-users though Mitesco’s footprint remains small currently [S16].

Vero's AI-enabled "Robo Agent" targets vertical SaaS opportunities by automating residential real estate sales processes leveraging cloud infrastructure. Initial rollout is planned for Q3 FY2026 but execution risks persist given resource constraints typical of early-stage ventures [S16].

Growth Prospects & Risks

Growth depends on expanding subscription customers for Centcore’s hosting/managed services alongside uptake of Vero’s AI products. Customer renewal rates post-contract are critical but subject to economic conditions influencing contract length or downsizing decisions by clients [S15], adding volatility risk.

Regulatory compliance presents ongoing challenges amid evolving data privacy laws such as CCPA/CPRA plus cybersecurity threats heightened by geopolitical tensions—including nation-state actors—which require continuous investment impacting cost structures or market availability [S6], [S10], [S17], [S20].

Legacy legal exposures remain material risks due to unresolved lease-related litigations from clinic operations that may consume future cash flows if settlements are unfavorable [S7], complicating financial planning.

Acquisition ambitions flagged as growth drivers carry integration risks given Mitesco’s lean management composed mainly of consultants without full-time staff—posing operational and cultural absorption challenges while managing scarce internal resources effectively [S22].

Returns & Capital Allocation Review

Operating returns remain negative with operating losses vastly exceeding revenues; approximate return on equity stands near negative 2.1% based on net income relative to negative equity base—signaling continued shareholder value erosion ([F1]). Capital allocation prioritizes survival via bridge financing; there have been no dividends or share repurchases recently given cash preservation imperatives ([S27], [S28]). Investments focus on low-capex approaches such as consultancy engagements replacing permanent hires alongside selective software development projects ([S16], [S19]).

Summary Commentary

Mitesco represents a high-risk technology startup grappling with legacy financial burdens during an ambitious transformation toward cloud infrastructure services complemented by early-stage AI application efforts. The low fixed-cost operating model using consultants mitigates burn rate relative to traditional firms requiring full-time technical staff or heavy physical asset ownership.

Nevertheless, the weak balance sheet combined with very modest revenues underscores fragility. Success hinges on rapidly onboarding paying customers for data center services while achieving meaningful revenue from products like Robo Agent slated for mid-FY2026 launch.

Competitive pressures from established global IT players with deeper pockets and broader footprints remain formidable. Concurrently evolving regulatory frameworks around data privacy heighten compliance costs potentially limiting market reach without adequate investment.

Recent capital injections through convertible note financings have sustained R&D but future funding availability remains uncertain amid dilution concerns affecting common shareholders.

In essence: Mitesco must demonstrate swift operational execution paired with rigorous cost control while navigating entrenched competitors plus complex regulatory environments or risk further erosion necessitating recapitalization or potential cessation.

This report is for informational purposes only and does not constitute investment advice or recommendations. Investors should perform their own analysis before making investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments