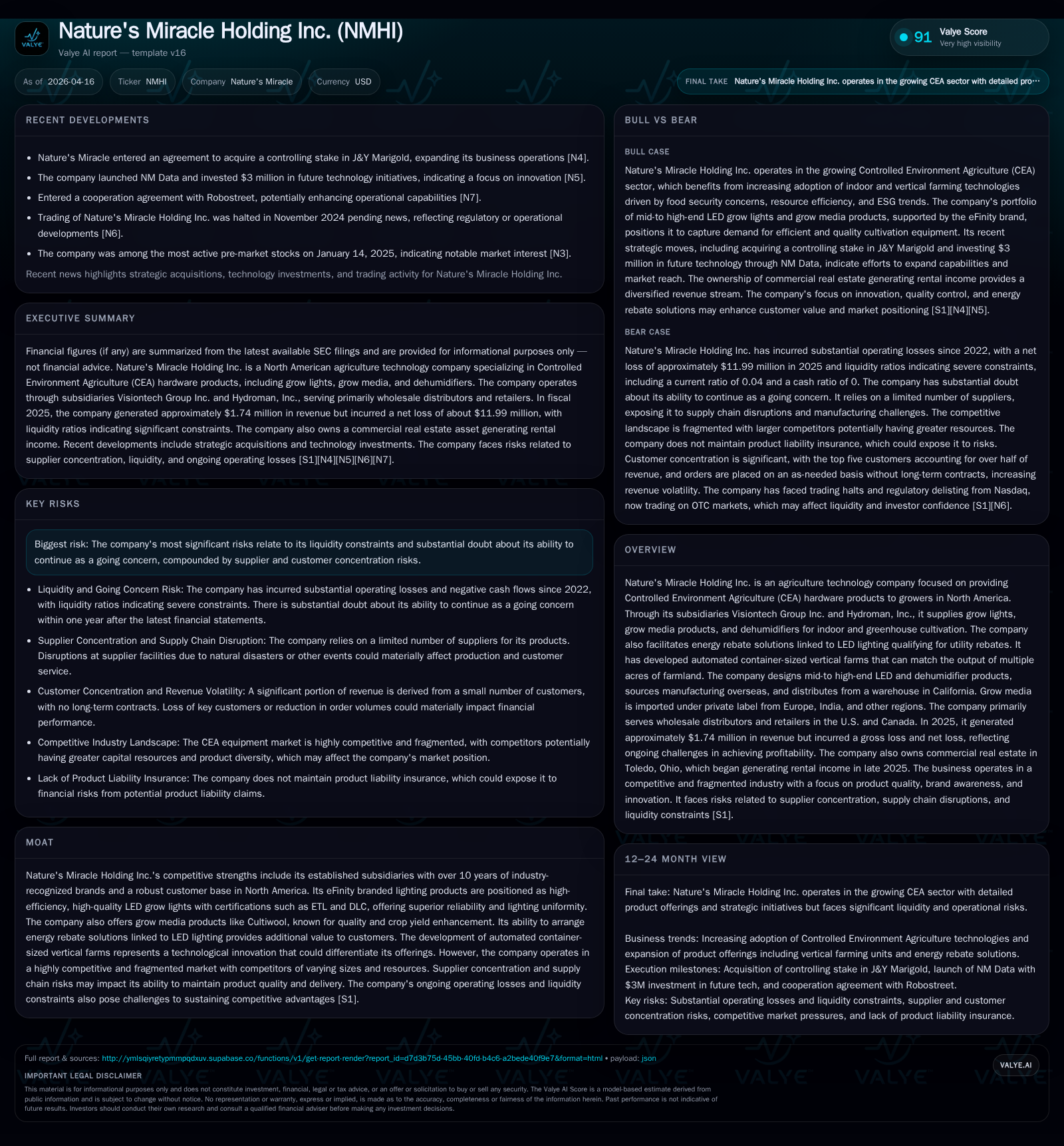

Nature's Miracle Holding: Charting the Impact of Declining Revenues Amid Operational Losses

Significant revenue contraction and continued operating losses at Nature’s Miracle Holding intensify liquidity risks amid a competitive Controlled Environment Agriculture market.

Nature's Miracle Holding Inc., a North American-focused CEA hardware supplier, has experienced a dramatic revenue decline exceeding 81% from 2024 to 2025, alongside persistent gross losses and negative operating income. Despite possessing differentiated product lines including high-efficiency eFinity LED grow lights and proprietary grow media, the company faces acute liquidity pressures highlighted by a dangerously low current ratio of 0.04 as of FY2025. Supplier concentration and ongoing operating cash flow deficits compound its financial fragility. Future growth hinges on successful commercialization of automated vertical farming units and energy rebate facilitation, yet is constrained by current financial distress and a fragmented competitive environment.

Historical Performance and Revenue Contraction Analysis

Nature's Miracle Holding Inc. has faced a stark reversal in revenue trajectory from fiscal year (FY) 2023 through FY2025 [F1]. In FY2023, revenues stood just under $8.9 million and climbed modestly to approximately $9.3 million in FY2024. However, FY2025 saw an unprecedented collapse to roughly $1.74 million—a decline exceeding 81% year-over-year. This revenue contraction has not been offset by cost containment as the company incurred gross losses both years: approximately $2.8 million in 2024 and persisting into 2025 (exact figure redacted) as disclosed in its annual report [S1].

The steep reduction in sales volume strained the company's ability to leverage scale against its administrative expenses — notably those increased by public company costs post-IPO transition cited in [S1]. Operating income remained deeply negative at -$7.15 million in FY2025 compared to -$10.35 million a year earlier, showing some albeit insufficient improvement [F1]. Net losses followed suit with $11.99 million reported for FY2025 versus $13.65 million the prior year.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -12 | -4 | -7 | -81.2% | +12.2% |

| 2024 | 9 | -14 | -6 | -10 | +3.7% | -86.1% |

| 2023 | 9 | -7 | -2 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 94.1 |

| 2024 | 95.2 |

| 2023 | 109.2 |

Source: SEC companyfacts cache [F1].

Revenue contraction outpaces any improvements in operating loss; CFO remains negative driven by operational cash burn.

Operational Losses and Liquidity Pressures: Unpacking the Going Concern Issue

Since 2022, Nature's Miracle Holding has accrued substantial recurring losses causing mounting liquidity pressures and triggering management’s disclosure of "substantial doubt" about its ability to continue as a going concern within one year after issuance of the FY2025 financial statements [S1][S10]. The company's cash position deteriorated sharply with only about $97K held as cash and equivalents at end-2025 against current liabilities totaling approximately $23.3 million as reported [F1]. This imbalance yields an alarmingly low current ratio of just 0.04.

Operating cash flows remain deeply negative at nearly -$4 million for FY2025 [F1], reflecting ongoing cash burning operations without meaningful offsetting inflows.

To bridge this liquidity gap, management indicates potential recourse to financial support from related parties or shareholders, debt financings with banks or other institutions, or additional equity financing in capital markets [S1][S14]. However, there are no assurances that such financings will be available at all or on commercially acceptable terms.

Failure to secure such funding could force operational cutbacks including reductions in research and development as well as sales and marketing staff—actions that could further impair growth prospects and market competitiveness [S1].

Portfolio of Products and Competitive Positioning in CEA Hardware

Nature's Miracle operates primarily through its subsidiaries Visiontech Group Inc. and Hydroman, Inc., supplying Controlled Environment Agriculture (CEA) hardware products: grow lights, grow media such as Cultiwool, and dehumidifiers tailored for indoor cultivation including greenhouses [S4][S20]. Its flagship lighting brand, eFinity, is marketed as a mid-to-high-end LED grow light line with recognized certifications—ETL and Design Lights Consortium (DLC)—indicating high efficiency, reliability, and superior lighting uniformity over competitors [S4][S20].

The company sources manufacturing overseas but maintains design control domestically; grow media products are imported mainly under private labels from Europe and India [S4]. Through these product lines it serves wholesale distributors and retailers throughout North America.

Innovatively, it developed automated container-sized vertical farms capable of producing equivalent output to multiple acres of traditional farmland—representing possible scalability advantages within CEA technology . This aligns with broader industry trends favoring year-round controlled-environment cultivation that optimizes resource use and yield predictability.

Despite strong product attributes, Nature's Miracle faces intense competition from both large national distributors/manufacturers with deep resources and localized players offering price-based alternatives [S20][S5]. Product quality, brand awareness—including trademarked eFinity—value perception, and comprehensive service are critical competitive factors that the company emphasizes but must balance against shrinking revenues.

Supplier Concentration and Supply Chain Risks Impacting Delivery and Costs

Supplier reliance represents a notable vulnerability within Nature’s Miracle’s operations: five largest suppliers accounted for virtually all purchasing volume — approximately 99.99% during FY2025 — indicating a critical concentration risk [S6]. These suppliers span regions facing geographic hazards: southern China is prone to earthquakes and floods; key U.S.-based suppliers face similar risks from wildfires or power interruptions [S6].

The company lacks product inventory insurance covering damages either during transit or storage at its California warehouse or direct shipments to customers—exposing it further to potential shipment loss [S5][S6]. Disruptions could cascade into delivery delays impacting customer service levels adversely while squeezing already narrow margins under falling revenues.

Efforts to diversify the supplier base appear nascent; expanding relationships for economic viability remains essential given supply chain fragility accompanying natural disasters or geopolitical uncertainties pervasive across international sourcing [S6][S29].

Future Growth Drivers, Market Demand, and Innovation Potential

Strategically invested areas highlight Nature’s Miracle’s automated container-sized vertical farm units designed to condense farmland-equivalent yields into modular indoor spaces—targeted innovation that could materially enhance per-unit output efficiencies if successfully commercialized . Coupled with expansion into energy rebate facilitation linked to its LED grow light products—potentially unlocking utility-driven cost savings for growers—the business aims to deepen market penetration across North America’s growing CEA sector.

Sector context supports growth drivers such as urbanization trends increasing demand for locally produced crops grown indoors under optimized conditions that improve yield consistency while reducing resource usage . However, given the company’s severe financial constraints detailed earlier ([S1],[S10],[F1]) scalability may be limited until profitability benchmarks can be achieved through stabilized revenue streams.

Absent explicit public forecasts or milestones within recent filings or news sources, monitoring commercial uptake of container farm units alongside recovery or stabilization of sales volumes will provide critical signals on growth viability (analysis).

Capital Structure, Financing Activities, and Shareholder Returns

Nature's Miracle’s capital structure reveals pressing concerns: shareholders’ equity turned deeply negative at approximately -$12.7 million at fiscal year-end 2025 reflecting accumulated losses since early-stage operations [F1][S16]. No dividend payments or share repurchase programs have been authorized amid ongoing operating red ink [F1][S23].

Capital injections have been raised through convertible debts alongside issuance of convertible preferred equity during 2024-25 periods intended primarily to address debt repayments arising from its business combination merger transaction costs plus working capital needs tied to public company expense structures [S1][S16]. Despite leveraging these instruments, continuous financing needs persist due to insufficient positive operational cash generation.

Return on Equity metrics appear artificially inflated (~94%) due largely to negative book value distortions rather than sustainable profit generation dynamics—a scenario cautioning interpretation [F1]. Continued reliance on external funding sources signifies elevated dilution risks absent fundamental operational turnarounds.

Outlook: Critical Milestones and Financial Metrics to Monitor

Absent explicit forward guidance from management or updated analyst coverage (none available), key performance indicators warrant close attention:

- Revenue trajectory reversing steep declines toward stabilization or growth,

- Gross margin improvements signaling improved production/sourcing efficiency,

- Positive turnaround in operating cash flows indicating operational viability,

- Rebalancing supplier diversification mitigating concentrated supply chain risks,

- Market acceptance rates for automated vertical farm modules demonstrating scalable differentiation benefits,

- Progress toward securing sustainable financing arrangements reducing going concern uncertainties.

Such metrics will collectively illuminate whether Nature’s Miracle Holding can shift from current distressed status toward sustainable growth within a highly competitive CEA hardware ecosystem (analysis).

This analysis is based solely on publicly available regulatory disclosures dated up to April 15, 2026 ([F1],[S#]) without any forward-looking projections beyond stated facts or speculation about future events. Investment decisions should consider independent assessments beyond this report.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments