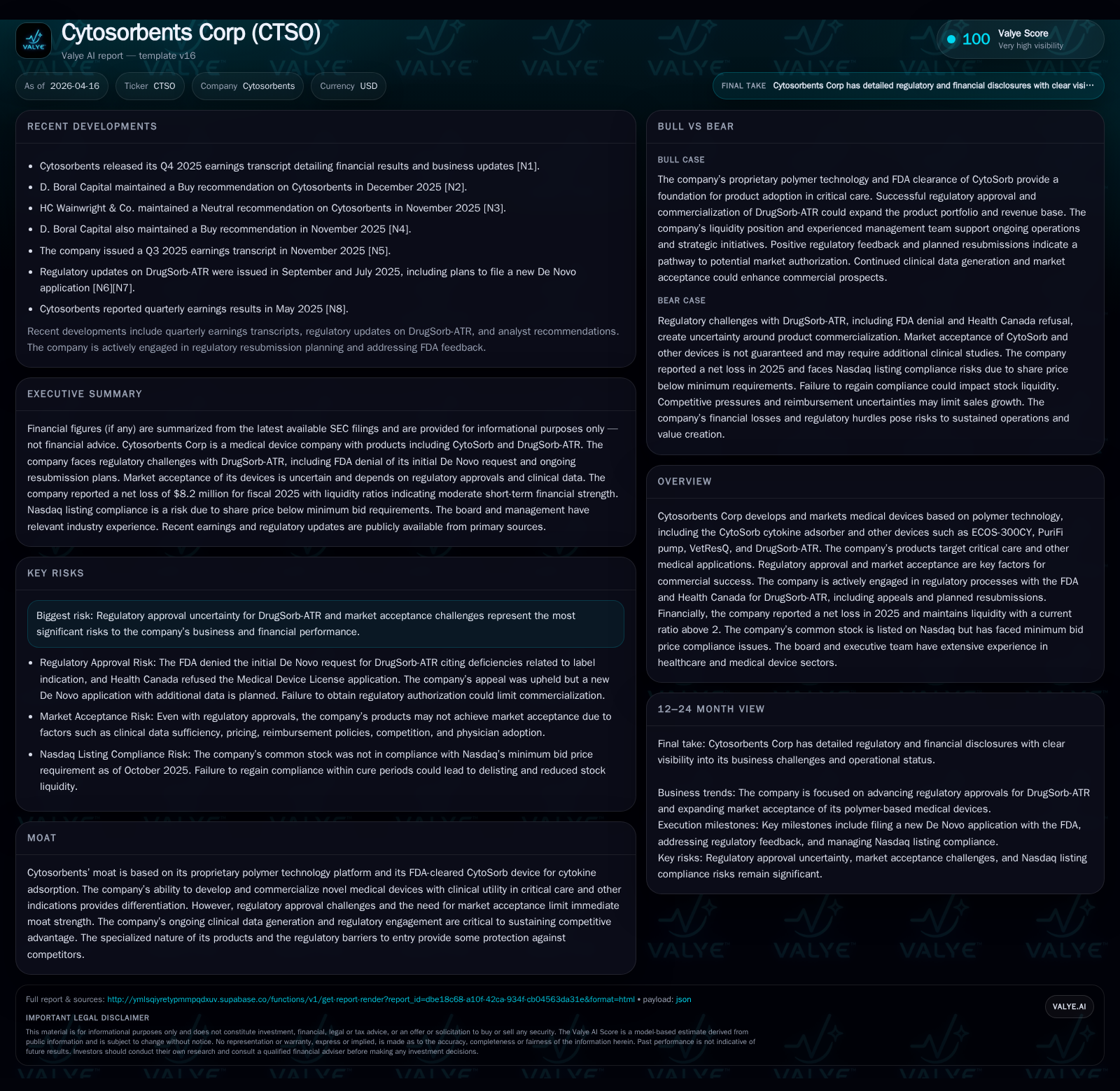

Cytosorbents Corp Confronts Regulatory Hurdles While Advancing Critical Care Innovations

Cytosorbents faces regulatory setbacks for DrugSorb-ATR amid strong technology-driven growth and maintains liquidity while pursuing FDA resubmission.

Cytosorbents Corp has demonstrated significant revenue growth over recent years fueled by its proprietary polymer technology, but persistent operating losses reflect ongoing R&D investment and regulatory challenges. The company’s DrugSorb-ATR device encountered an FDA De Novo application denial in April 2025, followed by an appeal process and plans for a resubmission with new real-world data expected mid-2026. Despite these regulatory hurdles and market acceptance risks, Cytosorbents retains a strong liquidity position with a current ratio above 2, though negative cash flows continue. Capital allocation remains conservative with no dividends or buybacks, focusing on funding clinical and regulatory milestones.

Strong Historical Growth Offset by Persistent Operating Losses

Cytosorbents Corp has exhibited a noteworthy growth trajectory in revenue since early commercialization stages. From generating just over $36,000 in revenue as far back as 2011, the company scaled sales up impressively to roughly $6.08 million by fiscal year-end 2018 [F1]. This exponential jump underscores successful penetration of the critical care market with its proprietary polymer technology platforms such as CytoSorb — an FDA-cleared cytokine adsorption device.

Yet operating results indicate sustained financial strain consistent with the typical medtech developmental lifecycle. Operating losses widened substantially from about -$6.36 million in FY2022 to -$14.75 million in FY2025 despite growing revenues [F1]. Net income remains negative at approximately -$8.2 million in FY2025, though this marks some improvement versus prior years which saw more severe net losses (nearly -$20.7 million in FY2024) [F1]. These losses reflect elevated R&D spending aimed at advancing product pipeline innovations and navigating regulatory pathways.

Operating cash flows also remain negative (around -$12.38 million in FY2025), signaling continuing cash burn from operating activities even after modest contraction compared to prior periods [F1]. Capital expenditures have considerably decreased from multi-million dollar levels seen a few years ago ($6.09 million capex in FY2022) down to only about $164,000 by end-2025, indicating a shift toward focusing resources on existing technologies rather than heavy fixed asset investments [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -8 | -12 | -15 | 0 | +60.4% |

| 2024 | -21 | -14 | -17 | 0 | +27.3% |

| 2023 | -29 | -22 | -9 | 1 | +13.1% |

| 2022 | -33 | -28 | -6 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -13 | -138.9 |

| 2024 | -15 | -186.5 |

| 2023 | -22 | -122.5 |

| 2022 | -34 | -92.8 |

Source: SEC companyfacts cache [F1].

Table captures key financial metrics illustrating strong revenue scale-up trajectory from minimal early sales countered by widening operating losses.

Regulatory Review of DrugSorb-ATR: Appeals and Planned Resubmissions

DrugSorb-ATR serves as Cytosorbents’ pivotal pipeline candidate targeting expanded clinical indications beyond its flagship CytoSorb device. However, it recently faced significant headwinds from regulatory authorities across major markets.

On April 25, 2025, the U.S. Food and Drug Administration (FDA) issued a denial letter for the Company’s De Novo classification request for DrugSorb-ATR citing outstanding deficiencies primarily related to insufficient evidence supporting the requested label indication rather than safety concerns [S2],[S4],[N1]. The company mounted an administrative appeal under FDA’s supervisory review process per CFR Title 21 Section 10.75 that included participation by senior FDA leadership and external surgical experts during July 2025.

The subsequent August appeal decision confirmed device safety but upheld the initial denial because additional clinical data was needed to substantiate efficacy claims and appropriate indications for use labeling [S4],[N1]. The FDA also tentatively proposed an expedited path forward contingent on provision of enhanced real-world evidence.

Encouraged by upper management feedback at FDA’s Center for Devices and Radiologic Health (CDRH), Cytosorbents opted against further appeal escalation and announced plans for a resubmission incorporating new comprehensive real-world data analyses expected early in calendar year 2026 [S4],[N1]. Ahead of this reapplication filing, the company submitted a pre-submission meeting request on November 7th aiming for formal feedback either late Q4 of 2025 or early Q1 of 2026 with a typical FDA review cycle of approximately 150 days thereafter [S2]. This revised approach underscores iterative engagement tactics within medical device regulation emphasizing post-market clinical follow-up data to support broader label claims.

Health Canada's parallel pathway similarly concluded with refusal of the initial medical device license application in June 2025 due to unresolved deficiencies [S4]. Following collaborative discussions including Canada's Medical Devices Directorate Bureau Director and regulatory counsel guidance linked to evolving clarity status for DrugSorb-ATR licensing prospects led Cytosorbents to withdraw their Request for Reconsideration while deferring re-submission until more definitive U.S. regulatory direction is received.

Market Acceptance Challenges for Polymer-based Critical Care Devices

While the CytoSorb polymer platform is proprietary with an established FDA-cleared cytokine adsorber commercial presence aiming at critical care applications such as mitigating cytokine storm syndromes among ICU patients [N1],[S7], achieving substantial market penetration hinges on multiple non-regulatory factors.

Clinical validation extending beyond initial clearance remains essential for securing physician buy-in and integration into standard care protocols. Real-world clinical utility demonstration supporting efficacy enhances treatment guideline inclusion probabilities.

Reimbursement landscapes governed by diverse payers including government programs and private insurers introduce pricing dynamics critical to hospital procurement decisions.

Competitive pressures loom from emerging novel devices potentially targeting similar inflammatory mediator control niches requiring continuous differentiation based on safety profile and ease of use.

Corporate partnerships with established medtech firms could accelerate commercial scale yet require alignment on strategic deployment and marketing investment.

Thus Cytosorbents confronts layered commercialization complexity beyond regulatory clearance whereby cumulative clinical evidence generation coupled with stakeholder engagement informs long-term adoption trajectories.[N1],[S7]

Financial Position: Liquidity Strong Despite Continued Losses

The latest financial disclosures underscore Cytosorbents maintains solid liquidity cushions despite persistent negative earnings trends.

At December 31st year-end 2025 balance sheet highlights show current assets totaling approximately $20.63 million against current liabilities near $9.71 million yielding a robust current ratio of circa 2.13x — indicating sufficient near-term solvency margins favorable for sustaining operations through ongoing clinical development phases [F1],[S9].

Cash and equivalents stood near $6.25 million providing immediate working capital availability [F1]. However operating cash flow continues negative at roughly -$12.38 million annually pressing the imperative for efficient cash management or supplementary financing avenues if extended timelines emerge [F1],[N1].

Debt instruments bear various maturities stretching out multiple years but do not appear presently impeding operational flexibility directly given investment grade-like spread profiles though detailed impact assessment merits further analysis outside current scope [S9,S10,S11,S12,S15,S16,S17,S18,S19].

Capital Allocation Strategy: No Dividends or Buybacks Amid Cash Burn

In light of financial resource constraints characterized by ongoing net losses and negative free cash flow (estimated approximately -$12.54 million combining CFO less capex), management has prudently refrained from deploying capital towards shareholder returns via dividends or share repurchase programs during fiscal year ended December 31st 2025 [F1],,.

Conservation of funds aligns strategically with intensive R&D focus required to advance product pipeline approvals particularly DrugSorb-ATR resubmission initiatives as well as commercialization infrastructure buildout.

Executive leadership complemented by board members possess extensive healthcare device sector expertise underpinning measured capital stewardship decisions aligned with long-term value creation objectives rather than immediate payout incentives that would stress liquidity further during phase-sensitive development environments.

Key Milestones Ahead: FDA Interactions and Clinical Data Expectations

Looking forward into mid-2026 calendar timeline frames milestone event anticipation around critical FDA engagements pertaining to new DrugSorb-ATR De Novo submission processes.

The scheduled pre-submission formal meeting late Q4/early Q1 window aims to clarify evidentiary thresholds requisite for market authorization potentially involving accelerated review mechanisms proposed earlier by FDA senior officials.[N1],[S2]

Successful navigation through these upcoming interactions combined with favorable regulatory outcomes represent key inflection points that could reframe valuation dynamics alongside enabling broadened commercial scale deployment opportunities leveraging improved label indications supported by novel real-world patient data analyses.[N1]

What Investors Should Watch: Regulatory Outcomes and Commercial Scalability

Cytosorbents’ stock liquidity presents short-term uncertainties tied to non-compliance risks related to Nasdaq minimum bid price rules after notification in October of sub-$1 average pricing triggers initiating cure periods expiring March-end 2026.[S6,S8]

Beyond market technicalities attention centers primarily on FDA authorization prospects—the ultimate success or failure herein will decisively influence company revenue realization curves amidst competing medtech innovation cycles.

Achieving reimbursement acceptance benchmarks alongside clinician endorsement within critical care units dictates adoption velocity essential for scaling recurrent product usage revenues amid evolving competitive landscapes.[N1],[S7]

Stakeholders must monitor pipeline developments encompassing additional pivotal trial results if pursued plus ongoing portfolio expansion efforts leveraging CytoSorb’s core polymer absorptive technology adaptable potential across therapeutic categories absent firm disclosures currently.[N1]

This analysis consolidates available financial data from official SEC filings alongside documented company disclosures about regulatory interactions without extrapolation beyond reported periods or forward-looking guidance absent explicit sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments