Global Gas Corp Eyes Localized Hydrogen and CO2 Solutions to Disrupt Industrial Gas Market

Global Gas pursues modular hydrogen and carbon recovery projects using renewable waste feedstocks, targeting localized industrial gas demand in major Western markets.

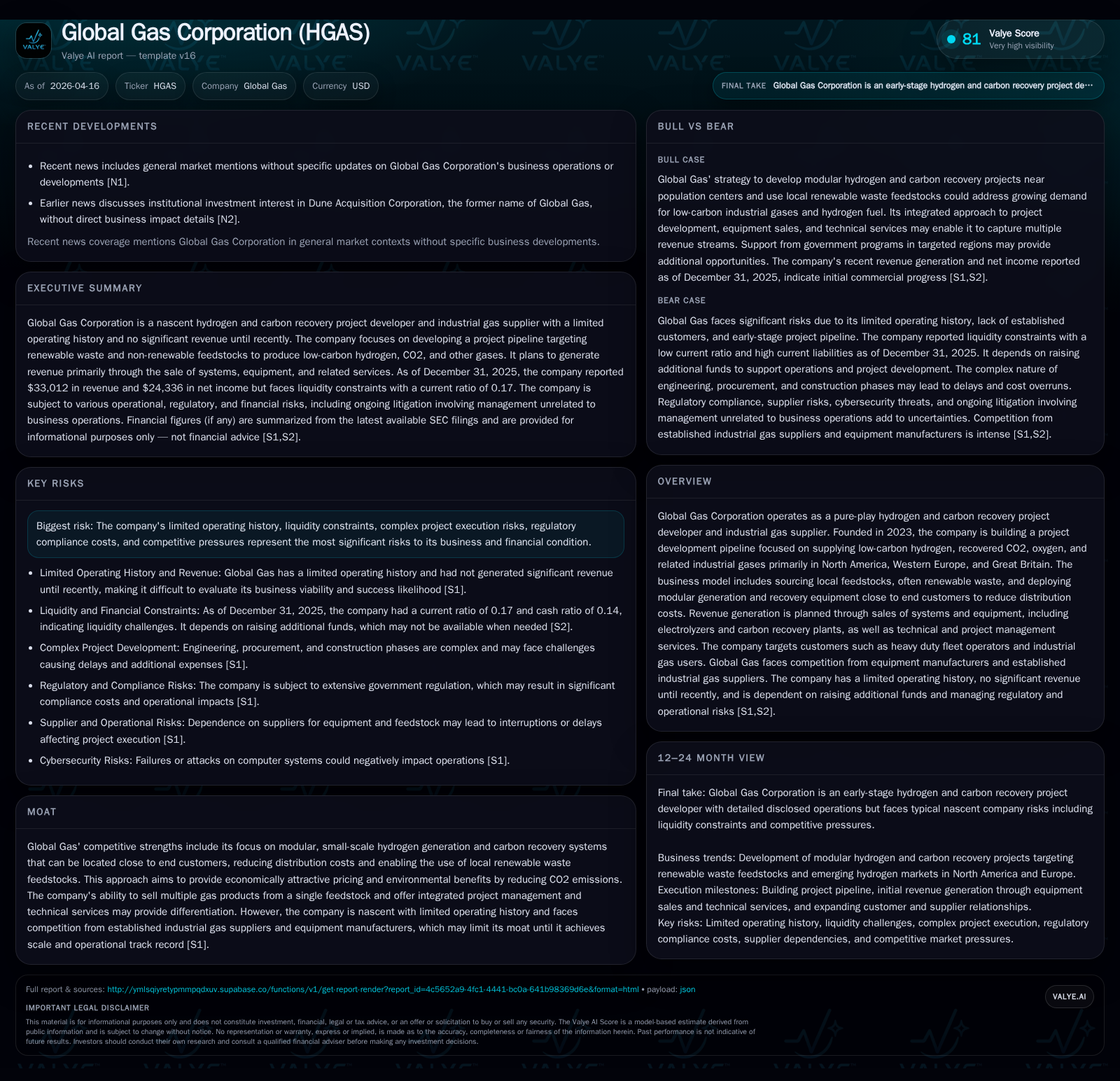

Founded in 2023, Global Gas Corporation develops modular, small-scale hydrogen production and carbon recovery projects near end users primarily in North America, Western Europe, and Great Britain. The company’s unique business model leverages local renewable waste feedstocks to deliver low-carbon hydrogen, CO2, and oxygen to sectors including heavy-duty fleets. While early financials show improving profitability trends, liquidity constraints and a limited operating history underscore significant operational risks. Market expansion hinges on project execution success and capital raises amid intense competition from established industrial gas suppliers.

From Startup to Scale: Tracing Global Gas’s Recent Financial Trajectory

Global Gas Corporation’s financial history spans only three full fiscal years since inception in 2023. The company demonstrates an evolving performance pattern indicative of its transition from a pre-revenue startup into early commercial operations. Annual revenues remain modest at $33,012 recorded by FY2025 [F1]. Despite this modest top-line figure, net income swung to positive territory at $24,336 in 2025 compared with significant net losses exceeding $130 million in 2024 and $300 million in 2023 [F1]. Operating income remains negative but improving sharply—operating losses narrowed by nearly 70% year-over-year from -$551.9 million in 2024 to -$166.2 million in 2025 [F1].

These results reflect initial revenue generation primarily linked to sales of specialized hydrogen generation systems and technical services rather than industrial gas resale volumes [S1],[S5]. Operating cash flows improved substantially but stayed negative at -$63.2 million for FY2025 versus over -$1.3 billion prior year [F1], underscoring ongoing investment phases associated with project development cycles.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 0 | -63226 | -166249 | +118.6% |

| 2024 | 0 | -1344037 | -551983 | +56.5% |

| 2023 | 0 | -160162 | -409027 | -104.6% |

| 2022 | 7 | -302262 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -8.2 |

| 2024 | 29.3 |

| 2023 | 40.9 |

| 2022 | -328.4 |

Source: SEC companyfacts cache [F1].

Improving operating loss margins and emergence into net profitability signal progress despite a nascent operating base.

Modular Hydrogen Generation and Carbon Recovery: The Core Business Model

Fundamental to Global Gas’ competitive positioning is its focus on modular "Gen/Fill" systems — compact hydrogen electrolyzers and carbon recovery units designed for installation close to or even onsite with customers [S5],[S16],[S21]. Unlike traditional industrial gas suppliers centered on large centralized plants distant from end users, Global Gas aims to capitalize on proximity advantages that dramatically reduce costly distribution logistics inherent in gaseous fuel supply chains.

The company employs flexible engineering to tailor projects to customer requirements including gas type (primarily hydrogen or CO2), volume demanded, location constraints, redundancy needs and budget considerations [S5]. Integration capabilities enable extraction of multiple gases such as oxygen alongside hydrogen and recovered CO2 from a shared feedstock input stream leveraging equipment like compressors and dispensers sourced from global industrial suppliers such as Emerson or PDC Machines [S16],[S28].

This modular approach enables opportunity for rapid deployment scalability while maintaining manageable capex intensity compared to large-scale facilities. It also aligns well with fuel cell heavy-duty vehicle applications requiring localized fueling infrastructure [S5].

Harnessing Local Renewable Waste: Market Differentiation and Technical Merits

A distinctive feature of Global Gas’ offering lies in sourcing low-cost renewable feedstocks often derived from waste streams such as anaerobic digesters or landfills [S1],[S5]. Utilizing anthropogenic waste not only lowers raw material costs but produces hydrogen with notably low lifecycle carbon intensity — some projects even targeting neutral or negative emissions profiles [S16].

This environmental benefit meets increasing regulatory mandates for decarbonization while enabling cost competitiveness against diesel in commercial fuel cell transportation sectors. Co-location strategies enhance feasibility by placing generation/recovery plants near anthropogenic CO2 emitters enhancing circular carbon reuse opportunities [S21].

Economically this vertical integration across multiple clean gases consolidates revenue streams while mitigating exposure to spot market price swings through diversified product output planning aimed at >70% long-term contracted sales book coverage prior to project approval [S16].[S20]

Current Financial Profile: Liquidity Constraints and Capital Structure Challenges

Despite operational progress, Global Gas faces acute liquidity stress highlighted by a working capital deficit exceeding $280 million at end-2025 driven by current liabilities ($335.5 million) exceeding current assets ($55.4 million), translating into a severely negative current ratio around 0.17 [F1]. Cash reserves remain critically low with under $50 million available as of Q3 2025 [F1].

The company’s primary sources of funds have been equity raises supplemented by related party advances; however, additional financings will be essential given ongoing substantial cash burn rates which reflect continued capex on project development and overhead costs [S3],[S4],[S6],[S10],[S14].

Legal proceedings involving management unrelated directly to core operations present reputational risk that can affect investor confidence indirectly but are not material business risks per filings [N2],[S10]. Regulatory compliance costs across multiple jurisdictions further add operational cost complexity in early stages [S14],[S15].

Growth Horizons: Expansion Plans Within North America and Europe

Global Gas concentrates its geographic focus on industrialized regions: North America (notably US), Western Europe including Great Britain where fuel cell adoption for transportation is accelerating supported by government incentives like the Inflation Reduction Act’s hydrogen tax credits [S1],[S5],[S16]. Markets targeted include heavy-duty fleet operators, industrial gas consumers traditionally reliant on centralized supplies and producers of renewable natural gas among others.

Though detailed recent news coverage is absent currently, structural demand drivers from decarbonization mandates coupled with modular scalability suggest potential pipeline expansion if development can be executed within capital limits . The capability to customize system sizes provides flexibility deploying into varied urban or segregated markets otherwise underserved by incumbent providers.

Operational Risks and Competitive Headwinds Ahead

Operating as a nascent developer with limited track record exposes Global Gas to significant risks: technical complexities during engineering procurement & construction phases could delay project completion or increase costs beyond estimates; availability of consistent feedstock supply may vary regionally causing operational interruptions; regulatory environments are fluid adding compliance burden; competition includes established global industrial gas suppliers leveraging scale advantages—this amplifies pressure on pricing strategy and customer acquisition [S1],[S10],[S14],[S15].

Industry jargon such as capex intensity metrics matter here given tight funding constraints while project-level technical risks remain elevated until scale benchmarks are met. Feedstock sourcing unpredictability also weighs on reliability perception critical in industrial gas contracting.

Capital Allocation Strategy and Return Metrics: A Nascent Track Record

Global Gas has yet to establish mature return metrics; approximate return on equity is negative approximately –8.2%, calculated using most recent annual net income ($24K) against an equity deficit nearing $296M at end-FY25 reflecting accumulated losses since inception [F1]. There are no dividends declared nor any share repurchase programs noted indicating all available capital is prioritized towards operational ramp-up.

Cash flows remain strained showing persistent negative operating cash flow despite improvement signaling continued rosiest focus on growth investments over near-term shareholder returns [F1,S25]. The company remains dependent on external equity issuance compatibility with maintaining credit access more than debt leverage at this stage [S3,S4,S6,S10].

Milestones to Monitor in 2026 and Beyond

Looking forward beyond explicit milestone guidance absent explicit forecasts or scheduled deliveries found in available evidence ([N#] lacking), key milestones warrant watch:

- Successful contracting of >70% output via letters of intent or binding agreements prior to new plant approvals which de-risks revenue streams per company project pipeline discipline outlined [S16]

- Commissioning success of modular Gen/Fill electrolyzer systems demonstrating operability under practical conditions validating technical approach [S5,S16]

- Acquisition of necessary permits plus demonstration of compliance adherence supporting expanded plant rollouts amidst tightening regulations

- Achieving incremental capital raises mitigating ongoing working capital deficits sustaining development cadence without compromising balance sheet integrity

- Building operational scale enabling margin improvement needed to transition cash flow toward breakeven status before meaningful returns manifestation. Monitoring SEC reports for developments on these fronts will reveal the viability pathway while failure flags may signal increased execution challenges.

This report is prepared solely for informational purposes based on publicly filed data as of April 16, 2026. It contains no investment advice or recommendations. Readers should note that Global Gas Corporation remains an early-stage entity with significant operational uncertainties amidst evolving market dynamics inherent in emerging clean energy infrastructure sectors.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments