QVC Inc’s Strategic Crossroads: Financial Strain and Growth Imperatives

QVC faces acute liquidity challenges and operational setbacks as it balances a legacy multi-channel model against urgent refinancing and growth demands.

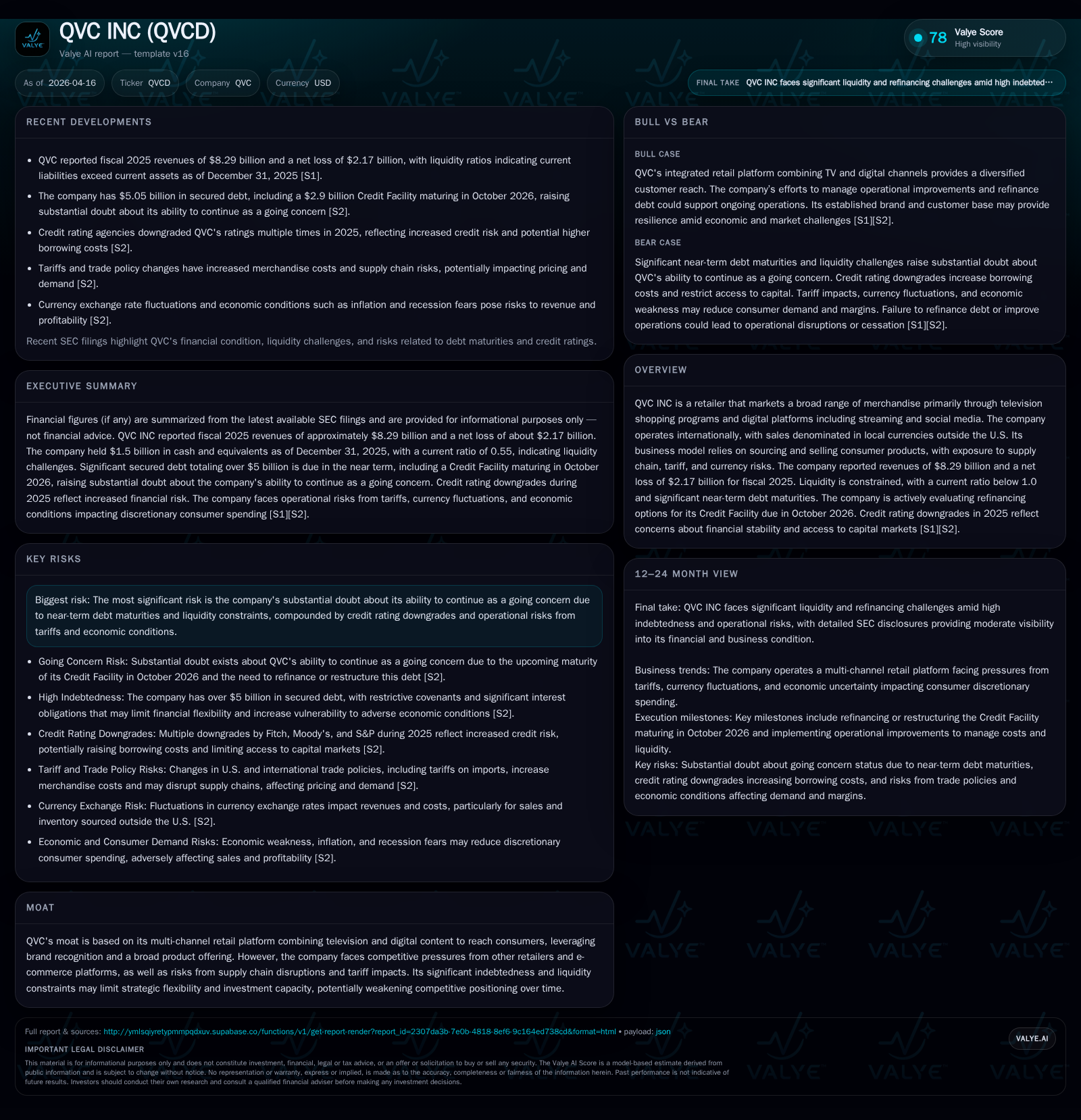

QVC Inc shows a marked deterioration in financial health through fiscal 2025, with revenues declining nearly 8% year-over-year and operating losses deepening past $2 billion. The company's multichannel retail platform combining televised shopping and digital extensions remains a core strength but is pressured by tariffs, currency volatility, and e-commerce competition. Imminent debt maturities in October 2026 raise significant concerns about going concern status, prompting a Chapter 11 bankruptcy filing to facilitate restructuring. Operational improvements and digital growth initiatives are underway amidst lender negotiations, but risks remain heightened by regulatory matters and rating downgrades.

Historical Financial Performance and Erosion of Profitability

Over the four-year span from 2022 to 2025, QVC underwent a pronounced decline in key financial metrics reflecting deteriorating operational conditions. Revenue decreased from $9.89 billion in 2022 to $8.29 billion in 2025 — a cumulative contraction of approximately 16%. The annual rate of revenue decline accelerated notably between FY2024 and FY2025 (-7.8% YoY) consistent with intensifying headwinds in consumer demand and supply challenges [F1].

Most striking is the operating income trajectory which swung from a positive $645 million profit in FY2023 into steep losses exceeding $2 billion by FY2025 — a deterioration of over 300% year-over-year indicating worsening margin pressures that outpaced top-line contraction. Net income followed suit with amplified losses reaching -$2.17 billion in FY2025 after more modest deficits previously [F1].

Despite negative earnings, operating cash flow remained positive at $419 million for FY2025, though down nearly 22% from the prior year. Capital expenditures scaled back significantly (down ~24% to $132 million), reflecting management's cautious posture amid tightening liquidity. The compressed cash flow generation relative to capital intensity highlights constrained free cash flow dynamics critical for servicing debt obligations going forward.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($mm) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8.3 | -2.2 | 419 | -2.0 | -7.8% | -102.8% |

| 2024 | 9.0 | -1.1 | 535 | -0.8 | -4.8% | -772.3% |

| 2023 | 9.4 | 0.2 | 1094 | 0.6 | -4.4% | +108.5% |

| 2022 | 9.9 | -1.9 | 409 | -1.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 287 | -181.4 |

| 2024 | 362 | -32.5 |

| 2023 | 912 | 3.7 |

| 2022 | 193 | -41.7 |

Source: SEC companyfacts cache [F1].

The critical liquidity metric current ratio has plummeted to approximately 0.55 as of year-end 2025, with current liabilities nearly double current assets—a signaling of balance sheet stress placing QVC firmly under short-term funding pressure [F1].

Drivers Behind Revenue Decline and Operating Loss Worsening

Several intertwined operational challenges catalyzed QVC’s top-line compression and margin deterioration through FY2025:

Tariff Increases: Following new U.S trade policies announced in April 2025 imposing baseline tariffs of ~10% on imports alongside specific punitive tariffs targeting China-origin goods, QVC faced escalated procurement costs for merchandise primarily sourced overseas. These elevated costs eroded gross margins despite selective pricing adjustments that slowed demand [S14][S17][S21].

Supply Chain Disruptions: The need to source alternative suppliers due to tariff impacts triggered costlier procurement cycles and periodic inventory timing shifts affecting product availability and promotional roll-outs [S14][S16].

Currency Volatility: With significant international operations spanning Europe, Japan, and the UK where revenue is realized locally but reported in USD, unfavorable foreign exchange movements substantially impacted translated sales figures as well as inflating inventory procurement costs denominated in foreign currencies such as the Chinese RMB [S15][S16].

Consumer Spend Contraction: Macro headwinds including inflationary pressures and global economic uncertainty curtailed discretionary spending on non-essential items sold via QVC’s various channels reducing volume sales at historically important price points [S15].

Competitive Environment: Increasing penetration of pure-play e-commerce players focusing on direct-to-consumer engagement across super-app ecosystems poses an ongoing challenge to QVC’s hybrid video commerce format requiring expedited investment into digital platform enhancements to sustain consumer reach [S1].

These converging factors collectively strained QVC’s multichannel retail ecosystem underpinning its revenue declines and accelerating operating losses.

Complexities of QVC’s Liquidity Constraints and Debt Maturities

A core issue confronting QVC is its substantial secured indebtedness totaling over $5 billion, primarily segmented between approximately $2.9 billion under its Credit Facility maturing October 27, 2026, paired with senior secured notes amounting to roughly $2.15 billion due mostly starting in calendar year 2027 onward [S3][S7]. The company’s financial covenants under these arrangements impose leverage limits mandating refinancing or deleveraging actions to avoid accelerated maturities.

In recognition of these pressures alongside deteriorating creditworthiness reflected by multiple rating downgrades (e.g., Fitch from B to CCC+, Moody’s from B2 to Caa3), QVC has publicly disclosed significant doubt regarding its ability to continue as a going concern without successfully refinancing this near-term Credit Facility obligation or completing its planned Chapter 11 restructuring process [S1][S2][S10][S12].

The planned Chapter 11 filing triggers an automatic stay preventing immediate creditor enforcement while accelerating all debt obligations legally but offering restructuring protections; operationalized through "first day" motions enabling ongoing business functions within bankruptcy court supervision during negotiation phases [S1]. This complex interplay between insolvency law protections, lender covenant restrictions, variable-rate interest exposure on the Credit Facility borrowings, plus ongoing creditor outreach quantifies the precarious capital structure environment facing management.

Debt agreement covenants also restrict asset sales without consent as well as acquisitions or dividend payments further limiting strategic flexibility during this critical period [S3][S11]. Moreover, increased interest rates on floating rate debt due to macroeconomic policy shifts magnify refinancing costs threatening liquidity if unmitigated.

Multi-Channel Retail Platform: Strengths Amid Competitive Pressures

Despite financial strains, QVC maintains a differentiated multi-channel retail platform blending traditional televised shopping networks (QVC U.S., HSN channels), digital streaming on multiple OTT services (Roku, Apple TV), mobile apps, plus robust social media integration incorporating TikTok live selling formats that capitalize on storytelling combined with immediate purchase capabilities—a setup often referred to as video commerce or streaming commerce within the sector jargon [S1].

Internationally, localized product sourcing teams tailor assortments adapting to regional preferences across Japan (operating via Mitsui JV), Germany (multiple channel variants), UK (segmented channels like QVC Beauty), and Italy; supporting distinct customer engagement strategies leveraging live broadcast studio production know-how juxtaposed with e-commerce fulfillment efficiency [S1].

This blended platform theoretically offers resilience against purely digital competitors by delivering brand familiarity combined with curated experiences not easily replicated without significant investments into content creation infrastructure.

However, competitive pressures persist from nimble online marketplaces optimized for fast shipping logistics while simultaneously digital marketing trends shift customer acquisition costs upward causing margin compression even on higher sales volumes.

Operational scalebacks driven by liquidity constraints notwithstanding, the brand equity associated with QVC-HSN remains an asset if effectively leveraged post-restructuring.

Forward-Looking Assessments: Chapter 11 Reorganization Impact and Business Viability

QVC’s upcoming Chapter 11 cases represent pivotal moments designed to restructure their balance sheet severely burdened by high leverage while preserving business continuity under court protection status [S1][S2]. Key strategic objectives include:

- Achieving deleveraging sufficient for sustainable capital structure standards.

- Refinancing or replacing near-term high-cost debts including the October ’26 Credit Facility maturity.

- Potentially monetizing non-core assets subject to court approval.

- Advancing WIN strategic initiatives focused on digital transformation alignment.

Reorganization risks encompass execution uncertainty surrounding plan confirmation timelines potentially lengthening operational disruption risk; dilution risks posed by negotiated creditor terms; diminishment of tax attributes impairing future cash tax outlays; as well as residual litigation uncertainties particularly linked to compliance mandates — all impacting going concern viability beyond emergence scenarios.

Investors and stakeholders should monitor:

- Bankruptcy court filings detailing proposed plan structures.

- Progress updates on creditor consents or financing commitments.

- Quarterly performance indicators reflecting stabilization or improvement trajectories post-initial restructuring steps.

- Outcomes of legal investigations affecting contingent liabilities.

Without successful execution of these clearly defined milestones, long-term survival beyond bankruptcy protection could be jeopardized with attendant loss realizations for equity holders likely.

Capital Structure, Cash Flow Dynamics, and Shareholder Returns Outlook

Analytically juxtaposing net income losses (-$2.17 billion) against shareholder equity tallying just over $1.19 billion at fiscal end yields a staggering negative return on equity approximation near -181%, symptomatic of capital base erosion accentuated by heavy retained losses over recent years [F1].

Nonetheless positive operating cash flows around $419 million underline underlying operational cash conversion capacity absent large non-cash items or working capital swings — albeit constricted relative to prior years by almost one-fifth reflecting volume & margin compression combined with tighter expense management [F1].

Capital expenditure prudence manifests through incremental reductions down to $132 million reflecting prioritization given financial constraints focused predominantly on essential maintenance capex over growth investments currently suspended or delayed during restructuring uncertainty phases.

Dividend distributions have been suspended since FY2019 when last recorded payments totaled close to $879 million—reflecting typical deleveraging priorities where free cash flow generation guides resumption prospects only post balance sheet normalization absent formal guidance from management given ongoing restructuring processes [F1].

Collectively these metrics portray an enterprise grappling simultaneously with operating recovery imperatives alongside urgent refinancing needs that absorb available cash resources restricting shareholder returns prospectively.

Operational Initiatives and Refinancing Strategies Underway

The company has articulated deployment of its WIN strategy targeted at refocusing operations towards profitable verticals within video commerce space synergized with emerging streaming platforms bolstered through social commerce integrations [S2]. However such initiatives are contingent not only upon internal execution capabilities but also access to capital resources elevated by lender collaboration efforts underway evaluating modifications or extensions of credit facilities contingent upon structural improvements agreed within Chapter 11 framework.

Management acknowledges lack of guaranteed success given macroeconomic uncertainties compounded by industry-specific disruptions yet presents these programs as foundational pillars for long-term competitiveness restoration post-restructuring transition periods intended for operational stabilization while protecting core brand franchises underpinned by differentiated content-driven retail formats accessible native both on TV screens and digital devices alike.

Risks Associated with Ongoing Litigation and Regulatory Compliance

Regulatory exposures focus notably around HSN subsidiary's settlement involving a $16 million fine paid pursuant to CPSC allegations stemming from delayed reporting requirements related to recalled Joy Mangano branded handheld steamers sold prior years—a matter extending into active criminal investigation phase initiated via grand jury subpoena received January ‘24 highlighting unresolved legal risk tailing compliance shortfalls capable of inflicting further penalties or injunctive relief potentially constraining revenue streams if recurring deficiencies manifest .

Moreover evolving regulations governing e-commerce conduct including privacy standards coupled with emerging compliance mandates concerning "conflict minerals" sourcing transparency exert continuous cost burdens which may increase compliance expenditures required ultimately absorbed into product pricing models risking marginal demand contraction if misaligned.[S5][S9][S17]

Concurrently constraints imposed by restrictive covenants coupled with restrictive debtor-in-possession financing terms during Chapter proceedings curtail operational levers limiting scope for proactive remedial measures outside bankruptcy plan scope further elevating risk profiles beyond routine retail sector hazards.[S26]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments