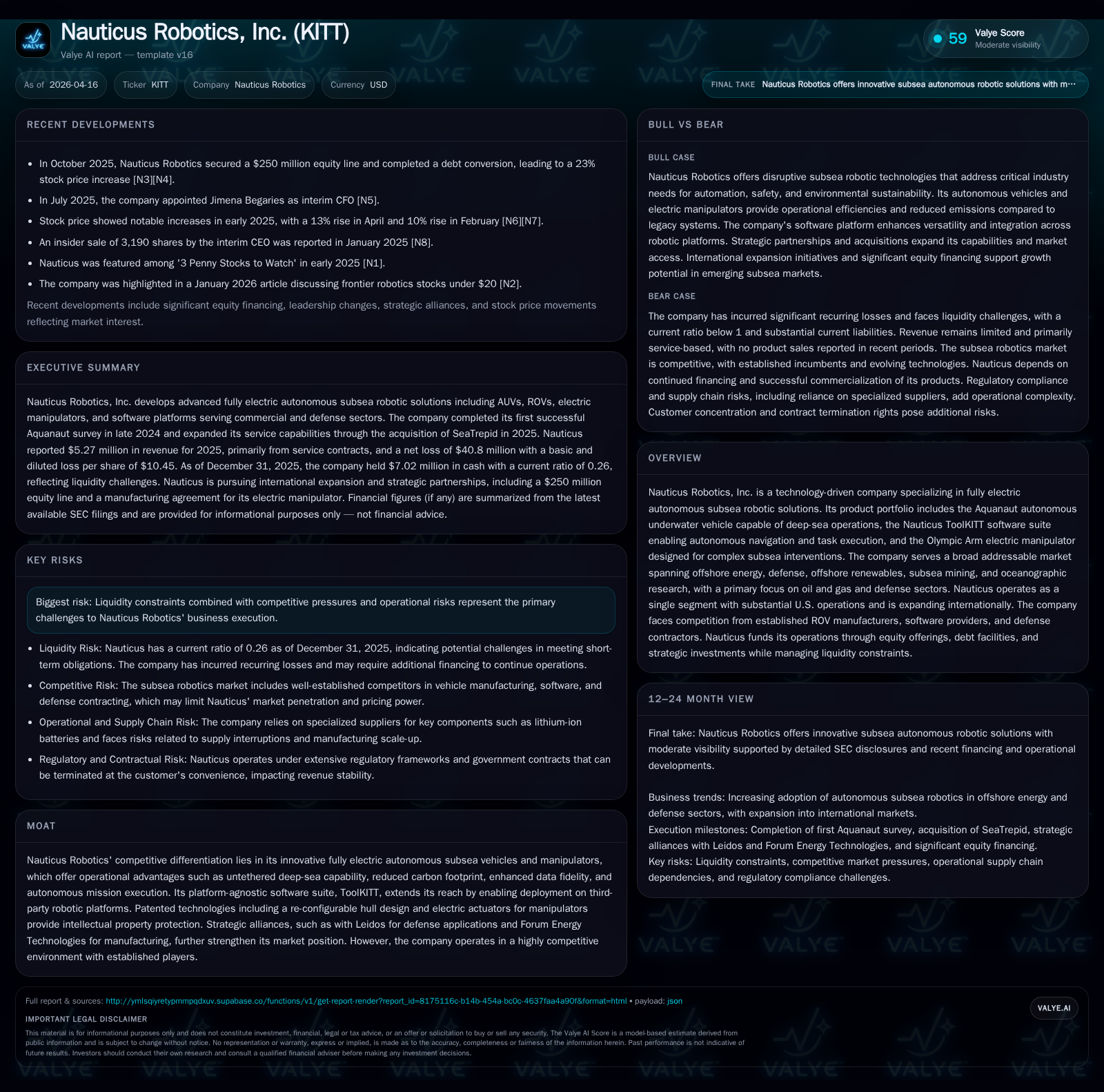

Nauticus Robotics Defines Autonomous Subsea Robotics’ Horizon With Strategic Innovation

Nauticus Robotics pursues commercialization of fully electric autonomous subsea vehicles amid capital constraints and competitive market dynamics.

Since its formation in 2022, Nauticus Robotics has advanced from concept to early commercialization by developing innovative untethered AUV technologies that challenge traditional tethered ROVs. The company’s flagship Aquanaut platform and proprietary software suite provide technical differentiation in deep-sea operations focused primarily on the offshore energy and defense sectors. Despite steady investments in R&D contributing to persistent operating losses, Nauticus faces significant liquidity risks due to its capital-intensive growth model and heavy reliance on debt and equity financing. Strategic partnerships with Leidos and Forum Energy Technologies bolster market adoption prospects; however, revenue concentration and execution risks warrant close monitoring as Nauticus aims to scale commercial deployments internationally.

Technology-Driven Growth: Nauticus’ Journey from Concept to Commercial Milestone

Founded through a business combination in September 2022, Nauticus Robotics has pursued replacing legacy tethered ROV technologies with fully electric untethered autonomous underwater vehicles (AUVs). Its flagship product, the Aquanaut AUV, achieved a crucial commercial milestone with its inaugural autonomous deep-sea survey in Q4 2024 ([S1],[S3]). This operational debut supports the company’s narrative as an innovator redefining subsea robotics — combining deep operational range without tether management with lowered carbon emissions due to smaller support vessels.

This technology evolution reflects persistent heavy R&D investment driving a transition from concept to initial revenue generation in industrial applications like offshore oil & gas infrastructure inspection and defense missions. Despite progress, the business remains early-stage, evidenced by continuing operating losses exceeding $23.7 million in FY2025, moderately improved from prior years (-2.6% YoY operating income) [F1]. Net income losses narrowed significantly by about 69.7% YoY to approximately -$40.8 million but remain indicative of substantial investment ahead of breakeven [F1].

Market Positioning and Competitive Differentiation

Nauticus’ competitive edge is anchored on technological innovation challenging entrenched ROV manufacturers reliant on tethered systems. Developing the Aquanaut AUV — a fully electric, untethered vehicle — mitigates operational limitations related to tether management logistics and vessel size. This translates into cost savings and supports a reduced environmental footprint important for regulatory compliance ([N1],[S1]).

Complementing this hardware is Nauticus’ platform-agnostic software suite ToolKITT which enables autonomous navigation and task execution on third-party subsea robotic platforms, expanding customer reach beyond proprietary hardware sales.

Patents covering re-configurable hull design and electric actuators underpin defensive technology moats. Strategic collaborations with Forum Energy Technologies for manufacturing scale-up and Leidos for defense systems development enhance production capabilities and credibility within target verticals ([N1],[S1]).

Competition includes dominant legacy players supplying hydraulic manipulators, conventional ROV systems, integrated subsea solutions, plus emerging software providers catering to subsea data processing demands ([S19]).

Financial Performance Overview: Growth Patterns and Profitability Challenges

The financial profile evidences a capital-intensive development lifecycle characteristic of frontier robotics innovation. Revenue was about $11.4 million at end-2022 [F1], with subsequent annual revenue figures undisclosed.

Operating income losses have remained material but narrowed from -$55 million in FY2023 to nearly -$23.7 million in FY2025 representing a ~57% reduction over three years yet underscoring unresolved profitability challenges [F1]. Net income follows this trend though net losses remain acute.

Operating cash flows are consistently negative; FY2025 saw nearly -$23 million outflows alongside significant capital expenditures supporting technology advancement (capex surged year-over-year) [F1]. This indicates no free cash flow generation and ongoing reliance on external funding.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -41 | -23 | -24 | +69.7% |

| 2024 | -135 | -24 | -23 | -166.2% |

| 2023 | -51 | -22 | -55 | -516.4% |

| 2022 | -8 | -37 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -581.7 |

| 2024 | 661.4 |

| 2023 | 121.3 |

| 2022 | -29559.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue disclosed only for FY2022; negative margins reflect ongoing R&D and commercialization costs [F1].

Liquidity and Capital Structure: Navigating Cash Constraints and Debt Levers

Liquidity metrics reveal financial constraints; as of December 31, 2025 the company held approximately $7 million cash against current liabilities near $35 million yielding a current ratio of about 0.26 ([F1],[S4]). These underpin going concern doubts given insufficient operating cash flow coverage combined with high cash burn rates ([S1],[S9]).

Capital structure involves multiple convertible debt instruments including November 2024 Debentures with original issue discounts convertible into equity at defined prices; senior secured term loans initially signed in September 2023 amended several times providing incremental tranches up to ~$20 million total principal ([S7]-[S17]). Key points include:

- Convertible Senior Secured Term Loan bears mid-teens interest rates annually with exit fees and original issue discounts amortized as interest expense.

- Conversion prices vary over time due to amendments incentivizing conversions during stock price dips.

- Several lenders converted portions of debt into Series Preferred Stock or Common Stock shares causing dilution risk.

Additional liabilities include SeaTrepid acquisition payables totaling about $3.3 million classified as current ([S11],[S26]).

The capex-intensive profile coupled with recurring negative cash flows necessitates periodic equity raises via At-The-Market offerings described in filings along with strategic investor commitments providing temporary liquidity relief but subject to market volatility affecting fundraising effectiveness ([S9],[S10]).

Strategic Collaborations Enhancing Product Adoption and Market Reach

Partnerships serve as pivotal growth enablers for Nauticus seeking wider adoption within subsea sectors.

The alliance with Leidos announced January 30, 2025 combines complementary expertise targeting next-generation autonomous underwater system applications for defense missions requiring advanced autonomy ([N1], [S1], [S19]). This may catalyze more government contracts despite termination-at-will contract structures.

Manufacturing scalability is projected through collaboration with Forum Energy Technologies providing established industrial capacity necessary for anticipated demand surges especially from oil & gas end-users deploying Aquanaut vehicles commercially ([N1],[S1]).

These alliances broaden footprint beyond invention toward operational reliability supported by recognized industry players enhancing client confidence.

Future Outlook: Opportunities Amid Customer Concentration Risks

Company disclosures omit explicit numeric guidance; qualitative commentary highlights ambitions for scaling commercial introductions beyond U.S.-centric pilots ([N1],[S1]). Growth drivers include:

- Transitioning pilot contracts into recurring revenue streams particularly within upstream oil & gas infrastructure inspection.

- Geographic diversification leveraging manufacturing partners for regional deployment efficiencies.

- Defense market penetration amplified by teaming arrangements enhancing bid competitiveness.

- Potential sector expansion exploring offshore renewables or subsea mining where autonomy offers advantages.

Customer concentration persists: In FY2025 roughly five clients represented nearly 70% of revenues including government entities subject to procurement variability ([S19],[S6]). Loss or delay of major contracts could heavily impact financial stability.

Monitoring contract backlog progression focusing on contract types (cost-plus versus fixed fee) is critical given margin implications alongside competitor responses from established incumbents.

Capital Allocation and Shareholder Returns: No Dividends or Buybacks Amid Reinvestment Needs

Given liquidity pressures driven by reinvestment into product lines alongside negative earnings trends there were no dividends paid nor share repurchase programs conducted recently ([S29]). This conservative stance aligns with prioritizing balance sheet repair ahead of shareholder returns.

Key Risks Amid Operational Execution and Funding Dependencies

Funding sufficiency amidst recurring losses combined with liquidity tension results in explicit going concern qualifiers communicated by management ([S1],[S9]).

Limited top-tier customer reliance imposes concentration risk heightened for governmental contracts often negotiated under termination-at-will clauses introducing revenue uncertainty ([S19],[N1]). Managing contractual cost controls is essential where fixed-price agreements may expose Nauticus to overruns given technical complexities inherent in subsea projects ([S20]).

Competition includes large integrated providers possessing matured relationships plus software-centric competitors advancing data analytics modules threatening differentiated value propositions ([N1],[S19]). Regulatory dynamics concerning defense exports or offshore operations may impose compliance costs or delays affecting project timelines.

This report synthesizes data exclusively from Nauticus Robotics’ publicly filed SEC documents through FY2025 supplemented by targeted news citations without offering investment guidance nor price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments