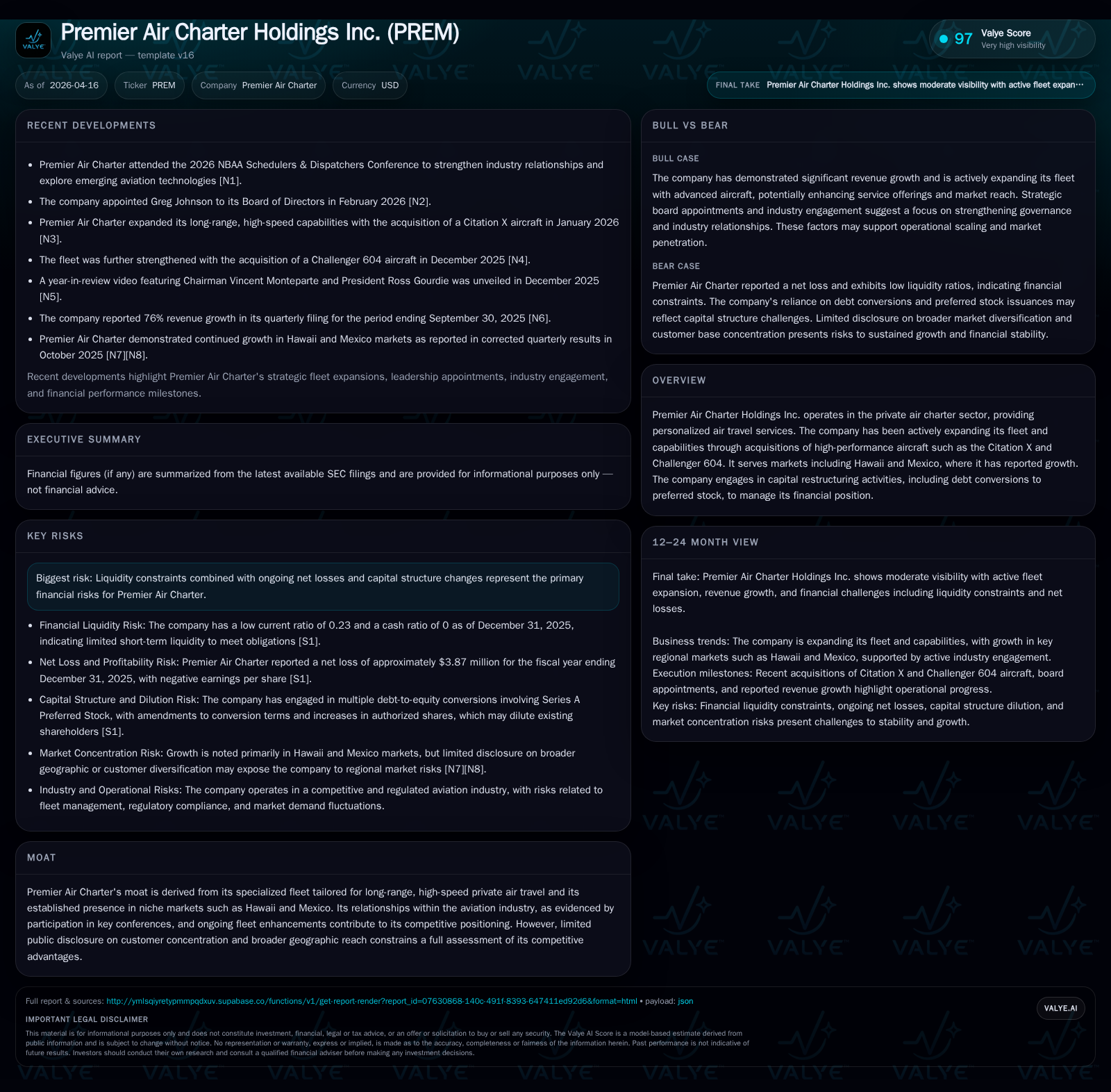

Premier Air Charter Navigates Growth Amid Liquidity and Profitability Challenges

Premier Air Charter Holdings Inc. reports robust revenue growth driven by fleet expansion and niche market focus, but continues to face significant liquidity constraints and operating losses.

Premier Air Charter Holdings Inc. achieved a 53.6% increase in revenue for fiscal year 2025, reaching approximately $31.9 million, supported by strategic additions of long-range aircraft and expansion into specialized markets such as Hawaii and Mexico. Despite this growth, the company’s operating and net losses widened, with an operating loss of $2.7 million and net loss of $3.9 million in 2025. Liquidity remains under pressure, with a current ratio of 0.23 at year-end 2025. The company has actively restructured debt through issuance of Series A Preferred Stock to alleviate financial stress, though capital expenditures have outpaced operating cash flow, resulting in negative free cash flow for the year.

Executive Summary

Premier Air Charter Holdings Inc., specializing in personalized private air travel services, reported substantial revenue growth for fiscal year 2025 with total revenues reaching approximately $31.9 million — a 53.6% increase over the prior year’s $20.8 million figure [F1]. This growth was driven by strategic fleet expansion that included acquiring high-performance long-range aircraft such as the Citation X and Challenger 604 jets, enhancing capacity to serve specialized markets like Hawaii and Mexico where private charter demand remains steady due to limited commercial alternatives [N1][S1][S5]. Despite these advances in top-line performance, the company continues to face challenges related to profitability and liquidity.

Historical Performance Overview

Premier Air Charter's financial results over recent years reveal strong revenue gains accompanied by widening losses:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 32 | -4 | 1 | -3 | +53.6% | -76.4% |

| 2024 | 21 | -2 | 3 | -1 | -25.2% | |

| 2023 | -2 | 0 | 0 | +29.2% | ||

| 2022 | -2 | 0 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -1398819 | -97.4 |

| 2024 | 1595351 | 140.5 |

| 2023 | 1197.3 | |

| 2022 | -15989.3 |

Source: SEC companyfacts cache [F1].

The company’s operating losses increased alongside revenue growth reflecting higher costs related to fleet additions and scaling operations [F1]. Operating cash flow returned positive in FY2025 after prior fluctuations but was insufficient to cover capital investments into fleet expansion that rose over 70% compared with the previous year [F1]. Equity improved from negative levels in prior years to positive territory by end-2025 primarily due to debt conversions into preferred stock [F1], though an approximate return on equity remains deeply negative near -97%, underscoring continued unprofitability.

Growth Drivers and Market Positioning

Premier Air Charter focuses on expanding its specialized fleet capable of long-range missions with jets like Citation X known for speed and Challenger 604 for cabin comfort [N1][S1]. These additions enable service differentiation on niche routes less served by competitors.

Geographic emphasis on Hawaii and Mexico leverages steady private charter demand driven by tourism and limited commercial options [S5]. This targeted approach aims at providing tailored luxury services rather than competing broadly with regional or fractional providers.

Participation at industry events such as the NBAA Schedulers & Dispatchers Conference supports relationship building while exploration of emerging aviation technologies signals efforts toward operational modernization [N1].

Furthermore, the February 2026 appointment of Gregory Johnson to the board introduces seasoned expertise in aviation fintech and technology platforms potentially enhancing pricing strategies and payment infrastructure aligned with evolving customer preferences [S24][S25].

Financial Position & Capital Structure Adjustments

Liquidity remains a critical concern: as of December 31, 2025 Premier Air Charter's current assets totaled roughly $3.7 million against current liabilities exceeding $16 million yielding a current ratio near 0.23 — indicative of significant short-term financial pressure [F1][S9][S12][S14].

To address indebtedness and improve balance sheet flexibility, the company engaged in multiple debt-to-preferred-stock conversion transactions during mid to late 2025:

- In August 2025 agreements converted approximately $6.42 million principal plus accrued interest into Series A Preferred Stock under terms designed to reduce dilution risk.

- November transactions settled nearly $2.93 million more debt via additional preferred share issuances following authorization increases.

These actions substantially reduced outstanding debt obligations but introduced preferred stock convertible into common shares subject to ownership limits [S11][S15][S21].

Cash equivalents were minimal as of prior period-end ($76), while capital expenditures remained elevated reflecting ongoing investment requirements for fleet maintenance and growth [F1]. Despite positive operating cash flow generation ($1.15 million), free cash flow was negative due to capex exceeding operating inflows by approximately $1.4 million underscoring capital intensity inherent in the business model.

Risks & Limitations

Risk factors outlined in recent SEC filings highlight ongoing challenges including:

- Significant liquidity constraints requiring vigilant working capital management given large current liabilities relative to assets [S4][S6].

- Continued net losses limiting internal reinvestment capacity necessitating reliance on external financing or equity solutions.

- Concentration in specific geographic markets exposes business performance to localized demand fluctuations without broader diversification benefits.

- Competitive pressures within private aviation may affect pricing power or asset utilization rates.

- Limited public disclosure on customer diversification prevents detailed analysis of client concentration risks.

The addition of a director with extensive aviation fintech experience may help mitigate some operational inefficiencies through technology adoption; however execution risk remains.

Outlook Considerations

No explicit forward guidance has been provided through filings or news releases up to April 2026; thus investors should monitor:

- Quarterly revenue trends for signs of sustained growth momentum beyond current niche geographies.

- Cash flow dynamics relative to continuing capex commitments indicating sustainability of fleet investments.

- Debt maturity profiles post-conversion activity assessing refinancing needs or potential liquidity events.

- Any strategic shifts toward geographic or service diversification that might reduce concentration risks.

- Outcomes from new board appointments signaling potential technology-driven efficiencies or business model evolution.

Overall Premier Air Charter stands at a pivotal juncture balancing rapid revenue growth enabled by fleet expansion against persistent structural cost burdens characteristic of specialized private air travel operations.

This report is based exclusively on provided SEC filings and verified public disclosures without extrapolation or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments