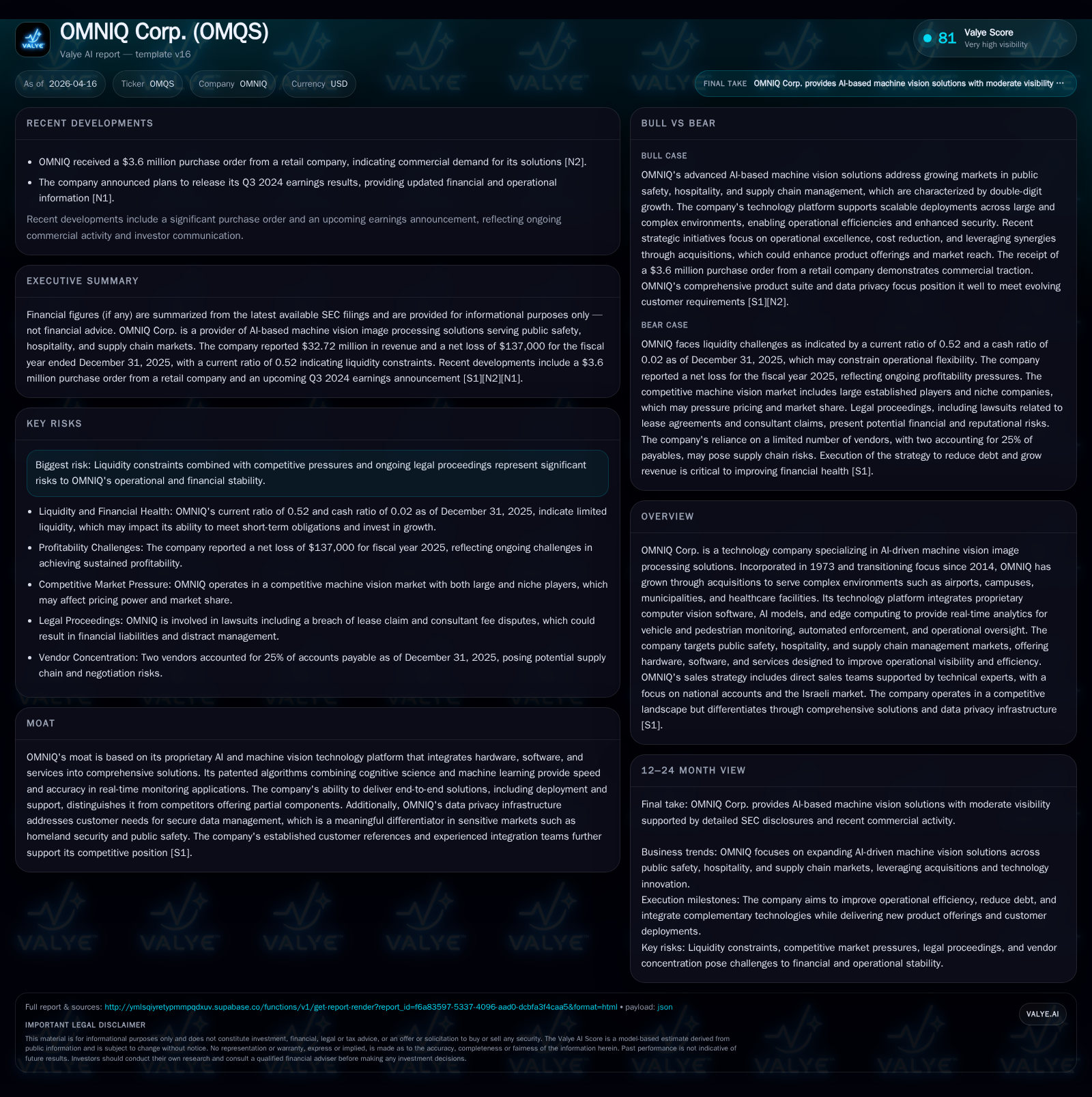

OMNIQ Corp. Focuses on AI Vision Solutions Amid Operational Challenges

OMNIQ evolves from energy roots into a technology integrator, enhancing operational cash flow despite steep revenue declines and balance sheet pressures.

Founded in 1973 with origins in oil and gas development, OMNIQ Corp. strategically transitioned in 2014 to specialize in AI-driven machine vision image processing. The company's proprietary technology platform serves complex environments such as airports, municipalities, and healthcare facilities with integrated hardware and software solutions. Despite a sharp revenue drop of 55.2% from FY2024 to FY2025, operating cash flow surged by over 200%, reflecting improved operational efficiency amid ongoing losses narrowing close to breakeven. Financial strain remains due to negative equity and liquidity constraints, compounded by active legal proceedings. Management focuses on operational excellence, strategic acquisitions, and leveraging synergies to sustain growth within public safety, hospitality, and supply chain sectors.

From Energy Roots to Tech Innovator: The Journey of OMNIQ Corp.

OMNIQ Corp., originally incorporated in 1973, maintained an oil and gas focus through the first decade of the new millennium. From 2008 to 2013, OMNIQ’s business concentrated on developing oil and gas reserves. However, the company decisively shifted its strategic direction starting January 2014 to focus on operating companies with proven positive cash flows and larger revenue bases [S1]. This shift led to acquisitions commencing with Quest Solutions (Jan 2014), Bar Code Specialties (Nov 2014), HTS Image Processing (Oct 2018), EyepaxIT Consulting (Feb 2020), and Dangot Computers Ltd. (July 2021), which collectively transformed OMNIQ into a specialized provider of computerized machine vision image-processing solutions.

Today, OMNIQ integrates proprietary AI-driven machine vision technologies tailored for complex environments—ranging from airports to municipalities and healthcare facilities—demonstrating a targeted approach across multiple industries [S1][S6]. This evolution represents not just a business pivot but also a foundational overhaul of core competencies aligned towards AI-enabled operational visibility and security.

Financial Trajectory: Revenue Decline Meets Improving Operational Cash Flow

The financial performance from FY2016 through FY2025 depicts significant volatility linked to the company’s transition phase and market challenges. Most notably, fiscal year 2025 saw revenue plunge by approximately 55.2% from $73 million in FY2024 down to $32.7 million [F1]. Operating income losses have narrowed impressively—from nearly $26 million negative as recently as FY2023 to just over $3.8 million negative in FY2025 [F1]. Similarly, net income swung closer to break-even with a -$137 thousand loss reported at FY2025 end compared to deep losses exceeding $29 million two years prior.

Despite top-line declines, operating cash flow surged by over 216% year-over-year between FY2024 ($2.37M) and FY2025 ($7.5M), emphasizing better working capital management or operational efficiency improvements [F1]. Capital expenditures declined sharply by circa 91%, supporting positive free cash flow generation estimated at roughly $7.46 million for the latest fiscal year.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 33 | 0 | 8 | -4 | -55.2% | |

| 2024 | 73 | 2 | -7 | |||

| 2023 | -29 | 0 | -26 | -115.1% | ||

| 2022 | -14 | 1 | -10 | -2.4% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1.1 | ||

| 2024 | 2 | ||

| 2023 | 1448000 | 0 | 84.0 |

| 2022 | 1448000 | 1 | 130.0 |

Source: SEC companyfacts cache [F1].

Balance sheet dynamics reveal substantial debt-related pressure with current liabilities exceeding current assets resulting in a current ratio near half at 0.52 as of FY2025 year-end [F1]. Moreover, shareholder equity remained deeply negative at -$12.7 million, reflecting accumulated losses and leverage challenges.

Proprietary AI and Machine Vision: Core Growth Drivers and Market Position

OMNIQ's technological edge lies in its patented AI platform that merges cognitive science principles with advanced machine learning algorithms within a multi-layered decision arbitration framework [S9]. This architecture supports rapid pattern recognition via computer vision models deployed on edge computing devices interconnected through centralized management systems.

The company offers a full-stack solution bundle including hardware components (networked cameras/sensors), proprietary software suites for vehicle recognition, license plate identification, pedestrian analytics, behavioral event detection, zone-based compliance monitoring, as well as network communications and automated enforcement mechanisms [S6][S14]. Such integration distinguishes OMNIQ amid competitors that typically provide partial solutions.

A key differentiator is OMNIQ's emphasis on data privacy infrastructure—critical when servicing sensitive applications like homeland security projects—which builds customer trust through responsible data management protocols controlling image/video data access securely [S7]. The experienced consulting teams further enhance client adoption by guiding end-to-end technology selection through deployment phases.

Market Footprint: Public Safety, Hospitality, and Supply Chain Dynamics

Targeting three primary segments—public safety including homeland security enforcement; hospitality venues requiring crowd monitoring; and supply chain management focused on legacy system replacement—the company participates in several billion-dollar markets exhibiting double-digit growth rates [S1][S4][S6].

Public safety deployments involve airports, border crossings, municipality surveillance programs utilizing vehicle recognition for automated enforcement or incident escalations [S15]. The Safe City initiative prominently features road safety monitoring technologies paired with real-time alerts for law enforcement agencies.

In hospitality contexts such as event campuses or sports venues, OMNIQ applies people-counting systems that track foot traffic flows crossing virtual thresholds ensuring safety compliance or operational efficiency [S5][S14].

Supply chain clients benefit from upgraded logistics monitoring replacing outmoded infrastructures using integrated AI systems feeding actionable data for inventory oversight or gate access control [S6][S9]. The modularity allows integration into existing enterprise workflows enhancing ROI via productivity gains.

Capital Structure and Liquidity: Addressing Balance Sheet Vulnerabilities

While operational cash generation improved significantly last fiscal year ($7.5M CFO), liquidity remains strained with liabilities far outweighing current assets ($27.7M liabilities vs $14.46M assets) yielding a suboptimal current ratio of only about 0.52 [F1][S13]. Negative shareholders’ equity (-$12.7M) highlights persistent leverage pressure possibly reflecting accumulated operating deficits as well as financing costs.

Recent securities offerings raised approximately $950K primarily through unregistered share sales alongside pre-funded warrants subscribed partly by CEO Shai Lustgarten—demonstrating insider commitment while supplementing working capital needs [S16][S22]. However, ongoing financing requirements appear critical.

Management explicitly stresses prioritizing cost reductions along with extracting synergies across acquired entities to deleverage the balance sheet over time [S1][S13]. Yet these actions must be balanced against sustaining necessary R&D investments demanded by fast-evolving AI/machine vision landscapes.

Legal Challenges and Risk Management in Multi-Jurisdiction Operations

OMNIQ faces material litigation risks notably from an alleged breach of lease contract filed in Israeli courts involving Dangot Computers Ltd., part of its acquisition portfolio; this claim totals approximately US$5.6 million equivalent [S10]. The matter is currently in mediation stage with the company maintaining it has vigorous defenses pending full exposure quantification.

Additional disputes include consultant fee claims around $389K for alleged unpaid commissions contested vigorously by OMNIQ invoking cross claims [S10][S12]. These legal burdens complicate financial planning scenarios adding uncertainty to near-term balance sheet outcomes.

Leadership Strategy: Management’s Plan for Operational Excellence and Synergies

OMNIQ’s leadership articulates a clear strategic focus on operational excellence emphasizing cost controls alongside technological leadership cemented through intellectual property protection [S1][S4]. The objective includes identifying internal synergies accelerating product bundling capabilities that enrich customer offerings while rationalizing overheads.

Sales efforts are vertically organized by sector expertise—public safety versus supply chain—and geographically focused particularly on the Israeli market where structured technical service support enhances solution uptake confidence [S7]. The integration teams bring cross-disciplinary talents enabling smoother enterprise-wide deployments fostering referenceable success stories which are critical competitive validation points.

Outlook: Acquisition Potential, Technological Leadership, and What to Watch

Analysis suggests that OMNIQ aims to augment its technological base further through selective acquisitions targeting companies specializing in data collection platforms, mobile computing architectures, or integration services enabling broader end-to-end solutions [S1]. This can mitigate revenue contraction trends if successfully executed while leveraging existing client relationships.

Upcoming quarterly earnings announcements scheduled per recent Nasdaq notice will serve as important milestones indicating whether operating cash flow momentum sustains amidst legal/risk offsets [N1]. Efficacy of ongoing cost reductions coupled with any resolution or escalation of current litigations will critically influence financial stability trajectories.

Monitoring product innovation pace relative to competitive advances especially among larger incumbents offering component-based machine-vision versus OMNIQ’s full-stack propositions remains crucial given fast-moving AI technology cycles.

Disclaimer: This analysis is based exclusively on available company filings (SEC Form 10-K/10-Q/8-K) dated up to April 16th, 2026 plus recent press releases without forming any investment opinion or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments