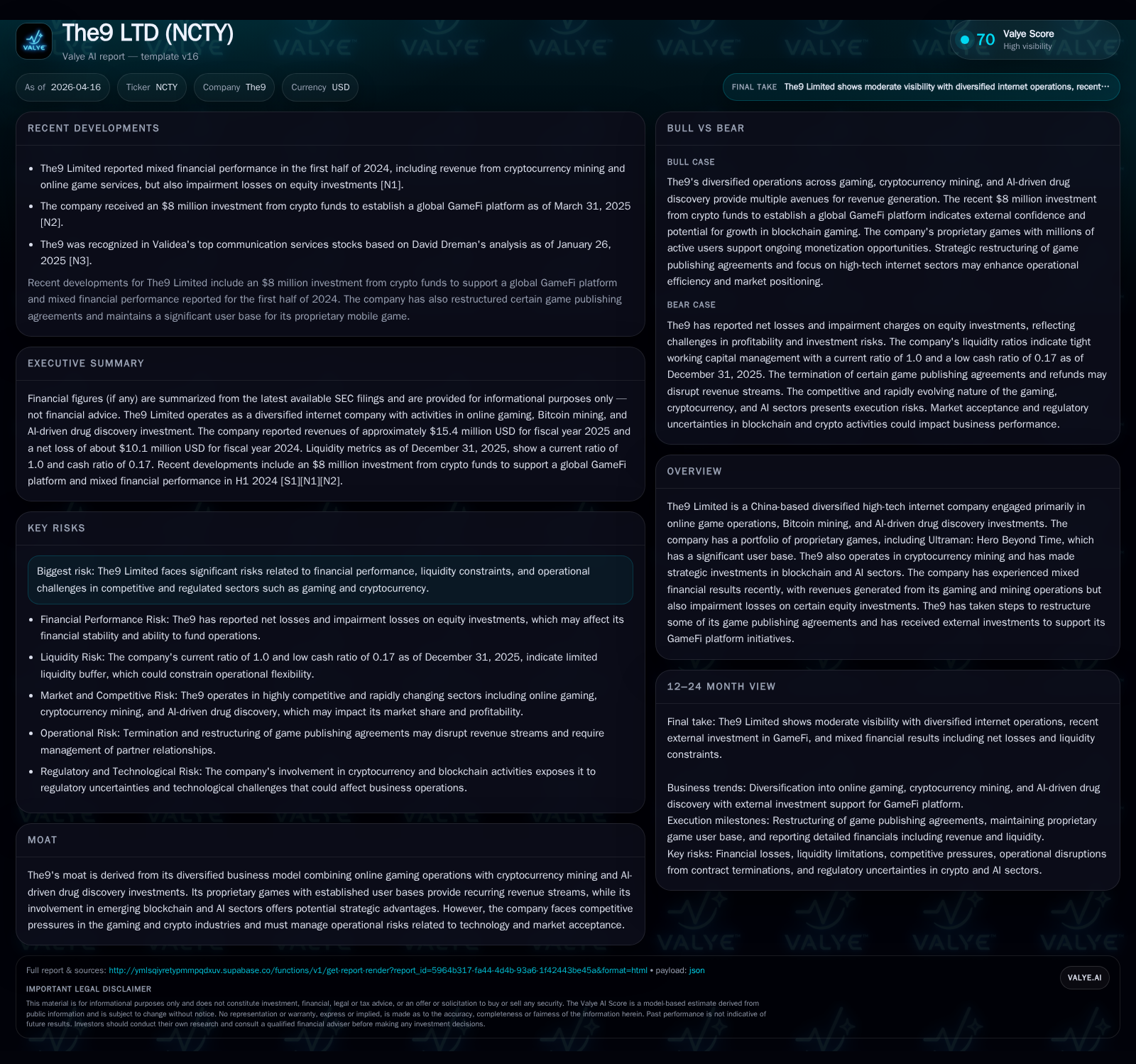

The9 Limited Navigates Strategic Shifts Amid Continued Operating Losses and Mixed Financial Results

The9 Limited’s evolution from online gaming to blockchain and AI investments shapes its current financial landscape, marked by revenue stabilization and significant operating challenges.

The9 Limited has transitioned from primarily online gaming to a diversified model including cryptocurrency mining and AI-driven initiatives. Revenues stabilized around $15.4 million in 2025, with gaming and mining contributing roughly equally. However, operating losses expanded sharply to approximately $40.2 million due to impairments and elevated expenses. The company’s liquidity remains tight, with current assets closely matching liabilities, while cash flow from operations is negative. Equity declined substantially amid cumulative losses. Key risks include cryptocurrency price volatility impacting secured loans and regulatory challenges affecting capital flows from Chinese subsidiaries. Growth prospects depend on successful development of GameFi platforms and AI-powered entertainment projects.

Company Overview

The9 Limited, listed on Nasdaq since 2004, has shifted its business focus from traditional online game operations toward a diversified technology company engaging in cryptocurrency mining and AI-driven drug discovery investments [S1]. The company’s original strength lay in proprietary mobile games such as Ultraman: Hero Beyond Time, but since around 2021 it has expanded into blockchain activities including Bitcoin mining [S1]. Concurrently, The9 is developing AI-powered interactive entertainment based on licensed IPs like "The Greed of Man" and investing in blockchain-based GameFi platforms to broaden its ecosystem [S3][N1].

Historical Financial Performance

The9's revenue trajectory reflects these strategic shifts. Total revenues declined sharply from approximately $25.2 million in 2023 to about $15.3 million in 2024 before stabilizing near $15.4 million in 2025 [F1]. Cryptocurrency mining dominated revenues earlier but contracted by 2025 when gaming services rebounded to comprise roughly half of total sales [S1][F1].

Operating losses remain substantial: after a deep loss of -$139 million in 2022, losses narrowed somewhat but were still significant at -$44.8 million in 2023 before increasing again to about -$40.2 million for the full year 2025 [F1]. These operating deficits reflect impairment charges on equity investments—such as a RMB42.8 million (approximately $6 million) impairment recognized for Beijing Weimingnaonao Science And Technology Co., Ltd. during H1 2025—and elevated general administrative expenses [S7][S8]. Net income similarly fluctuated, registering a loss of about -$10.1 million in 2024 following a small net income gain in 2023 [F1].

Cash flow remained under pressure with negative operating cash flow around -$4.5 million for FY2025 amidst minimal capital expenditures—indicating limited free cash flow generation capacity [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 15 | -5 | -40 | +0.8% | ||

| 2024 | 15 | -10 | -6 | -8 | -39.3% | -457.0% |

| 2023 | 25 | 3 | -7 | -45 | +46.3% | +102.0% |

| 2022 | 17 | -141 | -22 | -139 | -119.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | |

| 2024 | -21.7 |

| 2023 | 9.7 |

| 2022 | -2151.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue was essentially flat between FY24 and FY25 (+0.8%), while operating income deteriorated substantially (-399%) due to impairments and rising expenses.

Revenue Drivers and Business Segments

Cryptocurrency Mining

Since commencing mining activities around February 2021 [S1], cryptocurrency mining was the primary revenue contributor until recent years when its share decreased relative to gaming revenues. In FY25, mining accounted for about half of total revenues but remains exposed to Bitcoin price fluctuations which directly affect operational results and collateral valuations under secured loan agreements pledged against Bitcoin holdings at a loan-to-value ratio near 65% [S1]. Early in 2026 the company faced multiple default notices triggered by declines in collateral value necessitating cash top-ups or forfeiture of BTC collateral totaling approximately $3.6 million during loan settlements [S1].

Online Gaming & GameFi Initiatives

Following the amicable termination of the MIR M publishing agreement with Wemade in late 2025 due to market uncertainties [S9], The9 revitalized its proprietary mobile game portfolio including Ultraman: Hero Beyond Time, which had over two million monthly active users by late-2025 [S9][S7]. This resurgence contributed to a fourfold increase year-over-year in gaming revenues by mid-2025, representing roughly half of full-year revenue mix alongside mining activity [F1][S7].

Complementing this growth is The9’s push into AI-powered interactive movie games based on licensed television IPs and investment into blockchain-enabled GameFi platforms aimed at enhancing user engagement through decentralized ecosystems [S3][N1].

Cost Structure & Impairments

Significant general and administrative expenses have intensified operating losses alongside impairment charges related primarily to high-tech equity investments within blockchain and AI sectors [S7][S8]. These impairments underscore the inherent risks associated with venture-stage holdings amid uncertain performance outlooks.

Capital Allocation & Liquidity Position

As of December 31, 2025, The9 reported cash and cash equivalents of approximately $8.36 million against current liabilities near $49.1 million; current assets totaled about $48.97 million yielding a current ratio close to one—indicative of tight short-term liquidity without substantial cushion [F1]. Shareholders’ equity declined materially from $46.4 million at end-2024 down to about $27.3 million at end-2025 due mainly to accumulated deficits stemming from operating losses and impairments during this period [F1]. Capital expenditures have been minimal recently.

No recent share repurchase or dividend activities have been disclosed given ongoing negative cash flows and operational restructuring focus [F1][S1].

Regulatory & Operational Risks

Operating through subsidiaries across multiple jurisdictions—especially mainland China—subjects The9 to currency control regulations potentially restricting dividend distributions or fund transfers back to the parent company [S1]. Additionally, audit inspection limitations concerning Chinese auditors pose risks under U.S regulatory frameworks such as the Holding Foreign Companies Accountable Act that could threaten Nasdaq listing status if unresolved [S13][S1].

Further risk arises from cryptocurrency market volatility impacting collateralized loans secured by Bitcoin holdings; recent defaults requiring asset forfeiture highlight financial stress linked directly to price fluctuations within this segment [S1].

Future Growth Prospects & Considerations

Looking forward into FY26 and beyond, The9 aims to scale its GameFi platform leveraging blockchain technology while expanding AI-driven digital entertainment tied to popular IPs—a strategy intended to diversify revenue streams beyond traditional gaming and crypto mining sectors [N1][S3]. Continued growth depends on effective execution amid cost containment pressures.

Investors should monitor developments related to loan agreement settlements given recent default events as well as regulatory changes affecting cross-border capital flows or audit compliance relevant for Chinese firms listed on U.S exchanges.

Conclusion

The9 Limited exemplifies an internet technology firm navigating transformation amid volatile industry cycles spanning online gaming through emergent blockchain applications. While revenue has stabilized recently supported evenly by gaming and mining segments, large operating losses driven primarily by impairments continue constraining free cash flow generation.

Liquidity management remains cautious yet delicate given matched current assets-liabilities balances. Ongoing operational execution alongside evolving product portfolio development combined with exposure to cryptocurrency price swings and regulatory complexities will be key factors shaping The9’s medium-term outlook.

This analysis is based solely on publicly available filings dated through April 16th, 2026 ([F1], [S1], [S3], [S7], etc.) and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments