Mega Matrix Inc's 2025 Transition to Asset-Light Content Model Deepens Losses Amid Revenue Decline

A strategic pivot to licensing short dramas and AI integration aims to stabilize margins within a competitive streaming landscape.

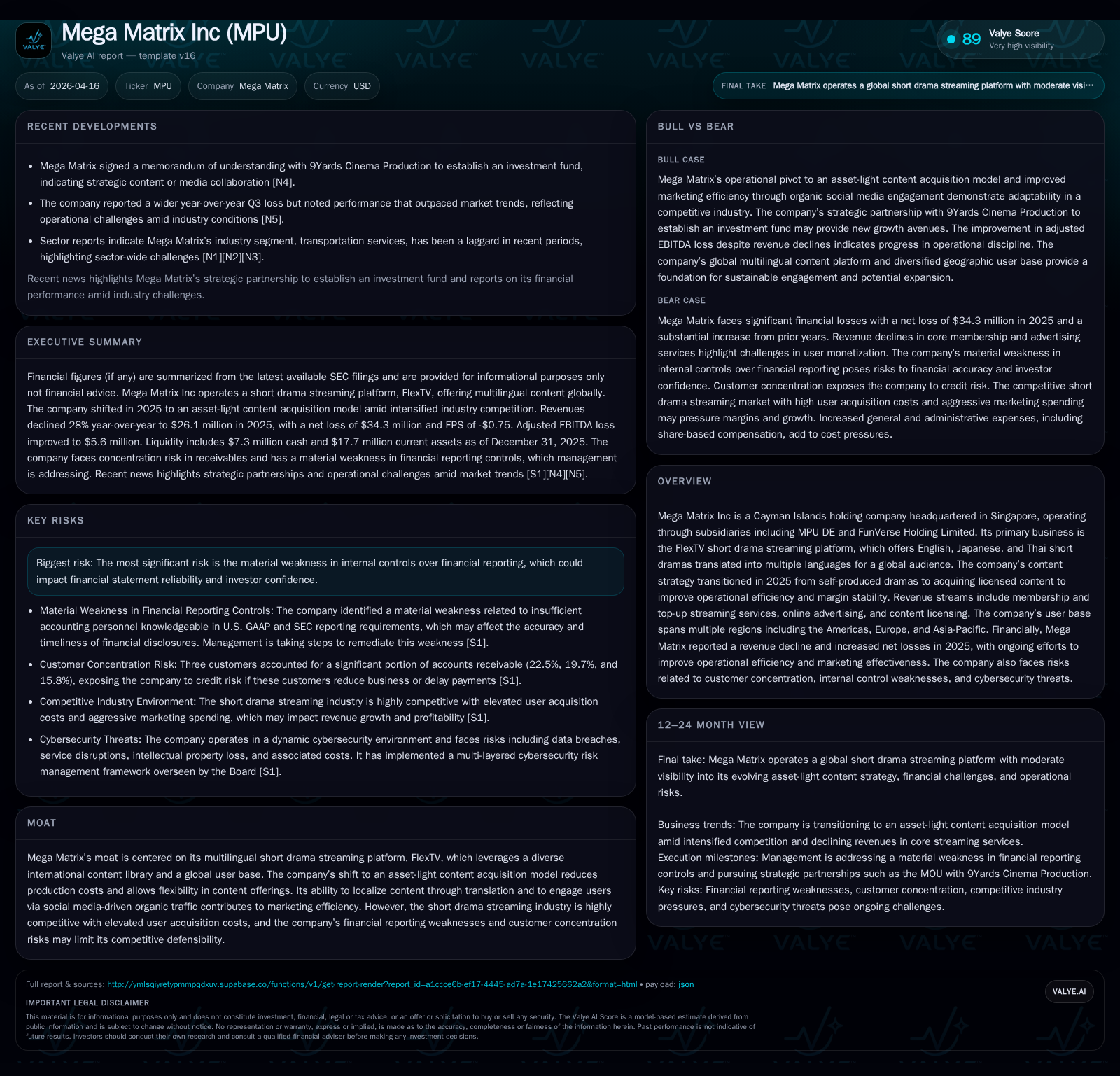

Mega Matrix Inc experienced a significant revenue decline of 27.9% in 2025, driven by intensifying competition and elevated marketing costs in the global short drama streaming industry. The company shifted from self-produced content to an asset-light licensing model and improved marketing efficiency via social media channels, increasing ARPU from $3.15 to $3.42. Despite these operational moves, net losses expanded sharply to $34.3 million, reflecting increased general administrative expenses and a one-time share-based compensation charge. The firm plans wider adoption of AI-generated content to reduce costs and drive future growth but faces financial reporting weaknesses and customer concentration risks that may constrain its competitive position.

Company Overview and Industry Context

Mega Matrix Inc is a Cayman Islands holding company headquartered in Singapore that operates primarily through subsidiaries including MPU DE and FunVerse Holding Limited, with FlexTV as its flagship product — a multilingual short drama streaming service offering English, Japanese, and Thai content globally across Europe, Americas, Asia-Pacific, among other regions [S1]. The platform employs translation capabilities catering to diverse international audiences.

The short drama streaming arena has grown increasingly competitive since early 2020s, characterized by rising user acquisition costs and intensified marketing battles amongst peers leading to widespread operating losses industry-wide. This environment placed heavy pressures on companies like Mega Matrix seeking sustainable profitability while scaling user bases.

Historical Performance and Growth Drivers

Mega Matrix recorded revenue of approximately $36.2 million in FY2024 but experienced a marked decline to about $26.1 million in FY2025, a drop of around 27.9% [F1]. This reflected softness primarily across membership and top-up streaming services plus reductions in online advertising sales resulting from fewer paying users placing ads [S9][S21].

Despite this top-line contraction, the company executed a deliberate pivot in its content strategy during FY2025 — shifting from costly self-produced short dramas filmed worldwide toward acquiring licensed third-party content with focused language translation for the FlexTV platform (asset-light model) [S1][S6]. This transition aimed at improving operational efficiency and achieving more stable margin profiles during volatile content production cycles.

Economically, this strategy produced tangible effects: the average revenue per user (ARPU) increased by approximately 8.6%, reaching $3.42 vs $3.15 the prior year reflecting enhanced monetization capabilities through optimized subscription conversions and retention programs supported by organic social media traffic growth [S1][S21]. Concurrently, advertising expenses were tightly controlled—dropping from representing 62% of total revenues in FY2024 down to 47% in FY2025—showcasing gains in marketing efficiency despite overall revenue shrinkage [S1][S6].

However, cost control was uneven; general and administrative expenses surged dramatically — more than doubling from roughly $10 million prior year to nearly $31 million — largely attributable to a one-time equity grant accounting for about $19 million in share-based compensation expense along with increased IT support costs following acquisitions which expanded headcount and infrastructure needs [S6][S18].

These dynamics translated into significant operating losses increasing year-over-year: operating income declined from -$11.6 million (FY2024) to -$28.9 million (FY2025), a worsening exceeding 149%. The net loss similarly expanded steeply — plunging from -$8.8 million up to -$34.3 million — rendering profit generation elusive during this period amidst strategic restructuring efforts ([F1], combined SEC sources).

Summary Financials

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 26 | -34 | -10 | -29 | -27.9% | -286.1% |

| 2024 | 36 | -9 | 4 | -12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -189.8 |

| 2024 | -63.0 |

Source: SEC companyfacts cache [F1].

Operating Cash Flow turned negative as profitability pressures intensified despite effective cost-cutting measures.

Adjusted EBITDA losses narrowed modestly from -$7.1 million (FY2024) to -$5.6 million (FY2025), excluding major non-recurring items such as share-based compensation ($19.4 mln) and digital asset fair value losses ($5.5 mln) unconnected directly to core operations [S7][F1].

Future Growth Prospects

Looking forward beyond FY2025, management's strategic priorities include integrating AI-generated short dramas into FlexTV’s content lineup aiming at reducing content development expenditures while enriching quality offerings tailored for global subscribers [S3][S21]. This initiative is expected to improve user engagement metrics through novel programming while lowering costs.

The company plans a hybrid approach combining continued third-party licensed acquisitions with selected proprietary AI-driven production capabilities — potentially positioning FlexTV uniquely compared with pure-play content creators or platforms relying solely on external libraries [S1][S21]. This aligns with broader industry trends embracing AI tools for scalable video content creation.

Additionally, Mega Matrix’s digital asset treasury initiatives including Ethereum staking resumed during mid-2025 alongside investments into stablecoin governance tokens could provide supplementary finance avenues through yield generation although these remain adjunct rather than core revenue sources at present [S16].

Capital Allocation and Liquidity

Mega Matrix enhanced liquidity throughout the challenging year by raising gross proceeds upwards of roughly $18 million via private placements ($16 million at July close) and At-The-Market (ATM) public offerings ($2.8 million net proceeds), strengthening cash position sufficiently amid losses [S14][S16][F1].

As of December 31, 2025, cash & equivalents stood at approximately $7.3 million against working capital near $13.3 million highlighting manageable near-term obligations coverage despite negative operating cash flow of nearly -$10 million for full-year activities [F1][S14].

Capital allocation prudence is evident given absence of share repurchases or dividends during the period; equity issuance remains primary funding mechanism amid accumulated deficit expansions totaling ~$60+ million since inception reflecting ongoing investment phases [F1][S8].

Key Risks and Challenges

Material risks confronting Mega Matrix include:

- A disclosed material weakness in internal controls over financial reporting raising concerns about reliability and investor confidence impacting capital access or valuation considerations [S12];

- Customer concentration risk with three customers accounting for about 58% of accounts receivable suggesting revenue dependency vulnerabilities if major clients reduce purchases or delay payments [S10];

- Cybersecurity exposure inherent in digital platform operation requiring robust defenses against data breaches or service disruptions that could impair reputation or trigger regulatory penalties given personal user data handling obligations across jurisdictions [S12];

- Highly competitive short drama market marked by escalating user acquisition costs alongside pressure on subscription pricing necessitating continued innovation on marketing fronts for sustainable margin improvement.

Analytical Observations

Mega Matrix’s shift towards an asset-light licensing model represents an effort to contain escalating production complexity/costs seen elsewhere within Asia-focused short drama sectors as well as embrace emerging content supply-chain efficiencies enabled by globalization of rights markets plus AI-powered creative tools—a sophisticated evolution matching trends observed among global OTT platforms integrating hybrid content sourcing strategies.

Yet the sharp rise in G&A expenses driven largely by substantial stock-based compensation underscores potential misalignment risks between operational performance improvement pacing versus shareholder dilution pressures.

Improved ARPU indicates success at incremental monetization despite subscriber base softness; however absolute membership declines cast shadows on near-term topline stability requiring focus on organic user acquisition leverage through social channels complemented by judicious paid advertising spend reductions [S1][S6].

Investments into Web3 initiatives such as Ethereum staking signal forward-looking treasury diversification though remain marginal relative to core subscription/advertising/licensing revenues under current scale.

Overall Mega Matrix navigates balancing innovation-led growth aspirations against structural industry cost pressures while managing liquidity stewardship risks inherent with prolonged negative cash flow trajectories.

Conclusion

Mega Matrix Inc’s FY2025 results reveal a company undergoing intensive transformation amid an unforgiving competitive environment reshaping the short drama streaming segment globally.[F1][S1] Its pivot away from costly original productions towards an asset-light licensing model combined with marketing optimizations yielded improvements in operational leverage—as indicated by ARPU gains and lowered advertising spend ratios—though insufficient yet to arrest significant revenue declines or bottom-line loss expansions exacerbated by one-time expenses.[F1] The planned integration of AI-generated dramas offers plausible pathways toward sustainable cost efficiencies critical for long-term value creation. Meanwhile challenges persist notably on financial control rigor plus customer concentration risks which management must address transparently if confidence is to be restored among stakeholders. Liquidity cushions strengthened by fresh equity raise provide runway but underscore dependence on executing strategic pivots successfully without further capital raises. Investors should watch closely for milestones related to AI content rollout effectiveness, membership trends reversal signals, margin stabilization progress excluding non-cash charges, and remediation actions addressing internal control gaps.

This report is based solely on publicly available information including SEC filings as referenced herein; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments