Awareness Group's Financial Trajectory Amid an Emerging Solar Ecosystem

TAAG’s integrated TAG GRID platform fuels top-line growth despite persistent operating losses and liquidity challenges in the nascent solar services sector.

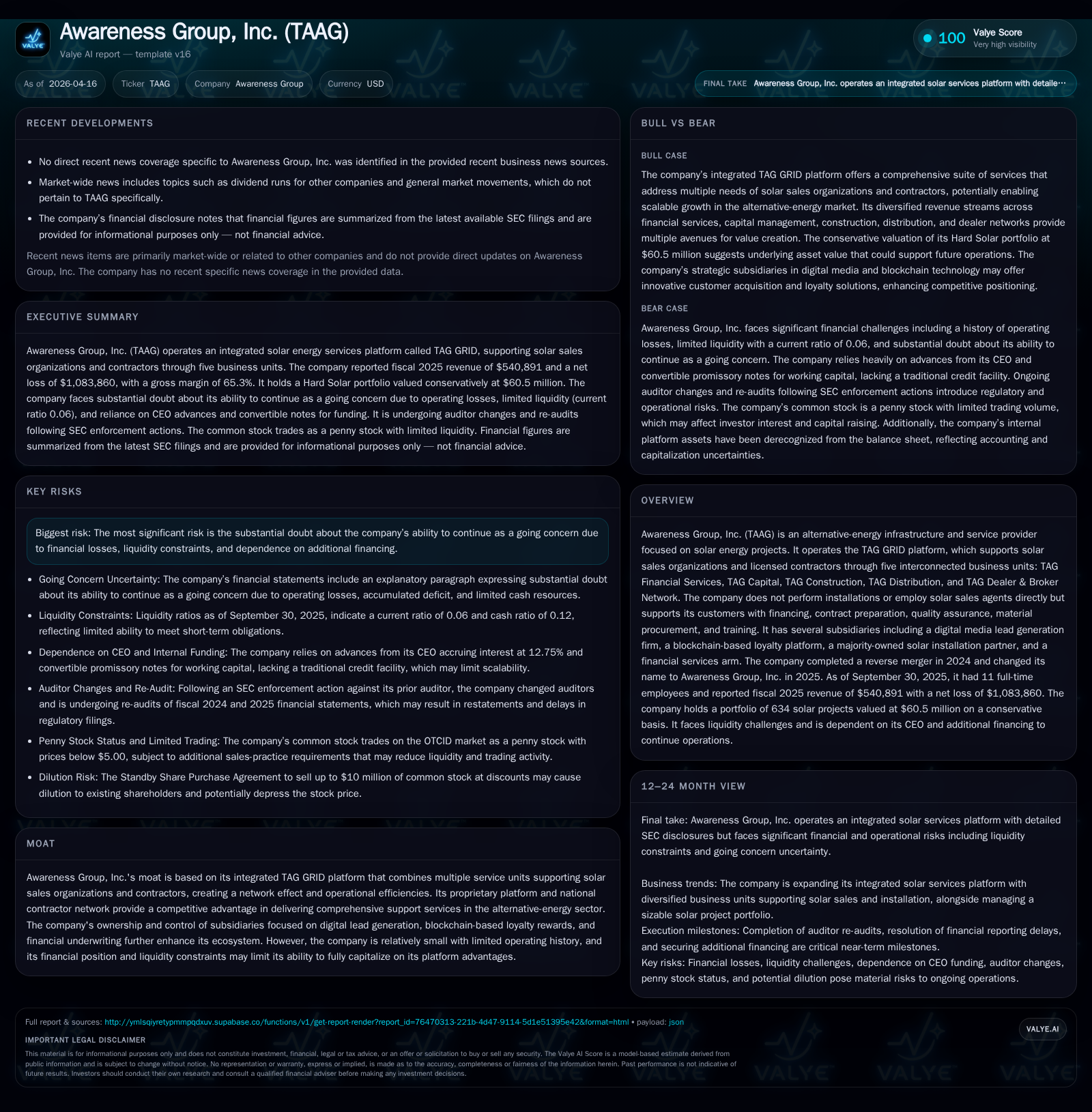

Awareness Group, Inc. (TAAG) operates an integrated solar services platform, TAG GRID, supporting sales organizations and contractors with a suite of financing, contracting, and operational services. The company delivered a dramatic revenue increase in fiscal 2025 driven by prepaid Power Purchase Agreements and consumer loan origination, though recognized revenue declined due to ASC 606 timing. Expanding the operational footprint introduced significant cost base increases leading to margin compression and substantial operating losses. Liquidity remains severely constrained with working capital deficits and going-concern doubts, necessitating ongoing capital raises and CEO advances. Management's forward-looking projections assume robust project pipeline growth, but audit uncertainties and limited operating history present risks for investors tracking this micro-cap alternative energy player.

Evolution of the TAG GRID Platform: From Concept to Market Reality

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 540891 | -1083860 | -495134 | -614330 | +932.2% | -322.8% |

| 2024 | 52400 | -256362 | 99214 | -278573 | +35.9% | |

| 2023 | 0 | -399918 | -51706 | -395456 | -548.2% | |

| 2022 | -61698 | -27775 | -76078 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -24.9 |

| 2024 | -0.9 |

| 2023 | 97.1 |

| 2022 | 15.0 |

Source: SEC companyfacts cache [F1].

Awareness Group, Inc. (TAAG) centers its business strategy around its proprietary TAG GRID platform—an integrated infrastructure and service offering targeting residential and commercial solar energy projects [S1][S13]. Distinctively, TAAG does not engage directly in solar installations nor employs sales agents. Instead, it supports solar sales organizations and licensed contractors through five interconnected units: TAG Financial Services handles contract preparation, financing structuring, quality assurance, and servicing consumer loans; TAG Capital serves as an internal fund manager issuing prepaid PPAs and consumer loan notes; TAG Construction operates a vetted national contractor network providing labor markup services; TAG Distribution procures materials nationally for resale to contractors; while the TAG Dealer & Broker Network vets independent sales representatives who refer projects—all collaborating to create a comprehensive service ecosystem [S13].

This hybrid model focuses on enabling rather than performing core installation or sales activities, yielding network effects that differentiate TAG GRID within the alternative-energy services market. By leveraging proprietary financing instruments like PPAs alongside its blockchain-powered loyalty platform Candela Coin and digital lead generation via Captain Manicorn subsidiary, TAAG aims to offer seamless integration across project origination through completion stages [S15]. This breadth mitigates competition risks tied solely to installation or manufacturing while targeting value creation via operational scale and financial engineering.

Revenue Surge Driven by Contractual Pipeline and Prepaid Agreements

Fiscal year 2025 saw a striking reported revenue figure of approximately $540,891—up roughly 932% from the restated FY2024 total of $52,400 [F1][S1]. However, this top-line expansion belies underlying complexity: the company’s recognized revenue declined when strictly compared using ASC 606 accounting standards due to timing differences between economic activity and revenue recognition triggers [S1][S9].

The surge was primarily fueled by executing a significantly larger volume of prepaid Power Purchase Agreements (PPAs) alongside originating consumer loan notes that carry high gross transaction values unreflected immediately as revenue under ASC 606 performance obligations rules [S1]. Accordingly, while transaction pipeline activity accelerated strongly—with contractual expansions signaling positive market traction—accounting constraints mean much economic value will be reflected in future periods according to project milestones or time amortization protocols [S4].

This disconnect between cash flows or transaction volumes versus revenue recognition underscores critical analytical vigilance regarding fiscal performance measures for TAAG’s evolving business model.

Decomposing Margin Compression: From Administrative Support to Operational Execution

The company's gross margin decreased markedly from approximately 94.3% in FY2024 to about 65.3% in FY2025 [F1][S1]. This margin decline does not stem from pricing or demand deterioration but is tied closely to TAAG’s strategic pivot from primarily administrative coordination toward more operationally intensive service delivery.

During fiscal 2025, TAAG expanded utilization of licensed third-party solar contractors under its TAG Construction unit along with higher commission payouts to external third-party sales organizations incentivized through the dealer network [S8]. These activities inherently contribute direct costs absent or minimal in prior periods dominated by low-cost origination functions [S9]. The resulting margin compression reflects scaling pains associated with shifting from a lean administrative model toward fulfillment responsibilities encompassing labor markups and broader service delivery costs.

From a unit economics perspective, this transition may yield longer-term durability alongside operational leverage once critical mass is reached; however, short-term profit metrics are negatively impacted as evidenced by falling gross margins alongside escalating costs.

Operating Expenses and Their Implications on Profitability Trajectory

Operating expenses surged roughly 38% year-over-year from $702,068 (restated FY2024) to $967,315 in FY2025 [F1][S1][S26]. These expenses were almost exclusively selling, general and administrative (SG&A), inflating losses given concurrent cost of revenue increases.

The primary driver behind this rise has been expanded professional services including legal advisory fees related to Securities and Exchange Commission (SEC) reporting compliance amid the ongoing S-1 registration process following TAAG's public company transition [S1][S26]. Other contributors include amplified back-office staffing levels meant to support operational scaling requirements plus audit-related costs following auditor changes [S26].

An important nuance was the elimination of previously recorded stock-based compensation ($254K initially booked as expense in FY2024 but reclassified as capital contributions upon restatement), which artificially reduced operating expense comparables for FY2024 [S1]. Absent this adjustment, operating expenses appear even more elevated in FY2025 on normalized basis.

Collectively these factors deepen operating losses—FY2025 operating income declined further into negative territory at approximately -$614K compared with -$279K the prior year—highlighting a challenging profitability landscape despite revenue growth [F1].

Liquidity and Capital Structure: Navigating Going-Concern Doubts

Liquidity constraints represent TAAG’s most acute challenge heading into fiscal 2026. At September 30, 2025 year-end, cash and cash equivalents stood at just $73,566 against current liabilities exceeding $11.46 million—yielding an exceptionally low current ratio near 0.07 [F1][S19]. The working capital deficit eclipsed $10 million underscoring highly stretched short-term financial flexibility.

Accumulated deficit totaled approximately $1.36 million pointing toward sustained net losses since operations acquired via reverse merger in late 2024 [F1][S12]. Financing has predominantly relied on advances from CEO Pablo Diaz bearing interest at nearly 13% annually totaling roughly $965K alongside convertible promissory notes reflecting tight credit provisions without traditional institutional credit lines available [S10][S19][S22].

These conditions led the independent registered public accounting firm to include an explanatory paragraph expressing substantial doubt about TAAG’s ability to continue as a going concern without securing additional equity or debt financing or generating sufficient revenues/cash flows [S12][S19]. Failure to raise needed capital could force operational contraction or cessation.

Subsidiary Ecosystem’s Strategic Role in Value Creation

TAAG reinforces its core platform benefits through several subsidiaries enhancing various value-chain aspects. Captain Manicorn majority ownership facilitates digital media customer acquisition utilizing content creation and sweepstakes campaigns targeting lead generation specifically for solar finance prospects [S15]. Candela Coin integrates blockchain technology delivering tokenized loyalty rewards pegged to verified solar energy production—a differentiator marrying fintech innovations with clean tech incentives.

Additionally, Standard Eco acts as TAAG’s majority-owned partner specializing in nationwide licensed residential/commercial installations handling permitting through commissioning phases—anchoring execution capabilities beyond pure coordination functions. Southwest Financial administers underwriting processes for consumer loan notes and prepaid PPAs managing credit assessment rigor critical in developing project finance portfolios within alternative energy markets [S15].

Together these subsidiaries form a horizontally integrated ecosystem that supports growth scalability while embedding technology-driven competitive moats uncommon among small-cap peers.

Management’s Forward-Looking View and Projected Growth

Management articulates optimistic assumptions underpinning future enterprise value built around accelerating contract pipelines currently estimated near $45 million of backlog supported by existing customer momentum [S5]. Key forward-looking model inputs include an annualized project growth rate target of roughly 25%, expected stabilized gross margins around 40%, coupled with a weighted average cost of capital (WACC) pegged at an elevated 15% reflective of microcap status with limited operational history.

A long-term terminal growth rate assumption near 3% aligns with broader clean energy sector expansion expectations referencing macroeconomic GDP trends [S23]. Nonetheless these forecasts come with typical cautionary language emphasizing risks including permitting delays, incentive program volatility, equipment/labor price fluctuations, financing availability challenges, competitive dynamics within residential/commercial solar markets plus regulatory uncertainties—all factors capable of materially impacting future results versus projections [S23]. These forward-looking statements comply with federal safe harbor provisions requiring skepticism toward overly sanguine extrapolations absent confirmatory outcomes.

Key Legal and Audit Developments Impacting Financial Transparency

TAAG’s financial reporting reliability has faced headwinds stemming from SEC enforcement actions against former auditor Olayinka Oyebola & Co., precipitating auditor dismissal in April 2025 followed by engagement of Shah Teelani & Associates tasked with auditing fiscal years ended September 30 for both 2024 (re-audit) and 2025 (initial audit) periods [S1][S3][S6][S25].

The prior auditor faced allegations related to antifraud violations including failure to act on fake audit reports bearing a principal signature used in filings [S11][S14], prompting regulatory scrutiny adversely affecting investor confidence.

Consequently there have been significant delays filing required periodic reports including outstanding Form 10-K filings past due dates raising risk of losing current filer status or invoking SEC listing limitations [S11][S21]. The comprehensive re-audit effort may also result in financial restatements amplifying disclosure risk contours undermining transparent financial communication during this transitional phase.

Capital Allocation Strategies: ROE, Cash Flow, Dividends,

and Buybacks Overview

Financial returns remain negative reflecting an enterprise still positioned within early-stage investment cycles focused on platform buildout rather than generating shareholder distributions or earnings returns. Approximate return on equity stands at -24.9% based on latest net loss relative to shareholders’ equity funds reported at September-end fiscal year data points [F1][S15].

Operating cash flows were strongly negative at approximately -$495K driven partly by working capital strains linked partly to prepaid contract assets/liabilities movements though reconciliation gaps pending final audit clarification exist [F1][S19][S27]. Capital expenditures remain modest consistent with asset-light model emphasizing fee-based income rather than heavy plant investment reducing free cash flow complexity albeit underscoring reinvestment needs not yet met.

No dividends have been declared nor share buybacks initiated reflecting precautionary stance given liquidity stresses although potential equity line funding agreements pursue dilutive issuance capacity as near-term financing alternatives under standby purchase agreements potentially depressing per-share valuations [F1][S24].

Disclaimer: This analysis is based solely on factual disclosures obtained from SEC filings dated April 16, 2026 ([F1],[S1]-[S28]) supplemented by recent industry news transcripts ([N1],[N3],[N5],[N11]) without speculative assertions or investment advice recommendations. Past performance is not indicative of future outcomes. Readers are encouraged to consult primary source documents directly for detailed information.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments