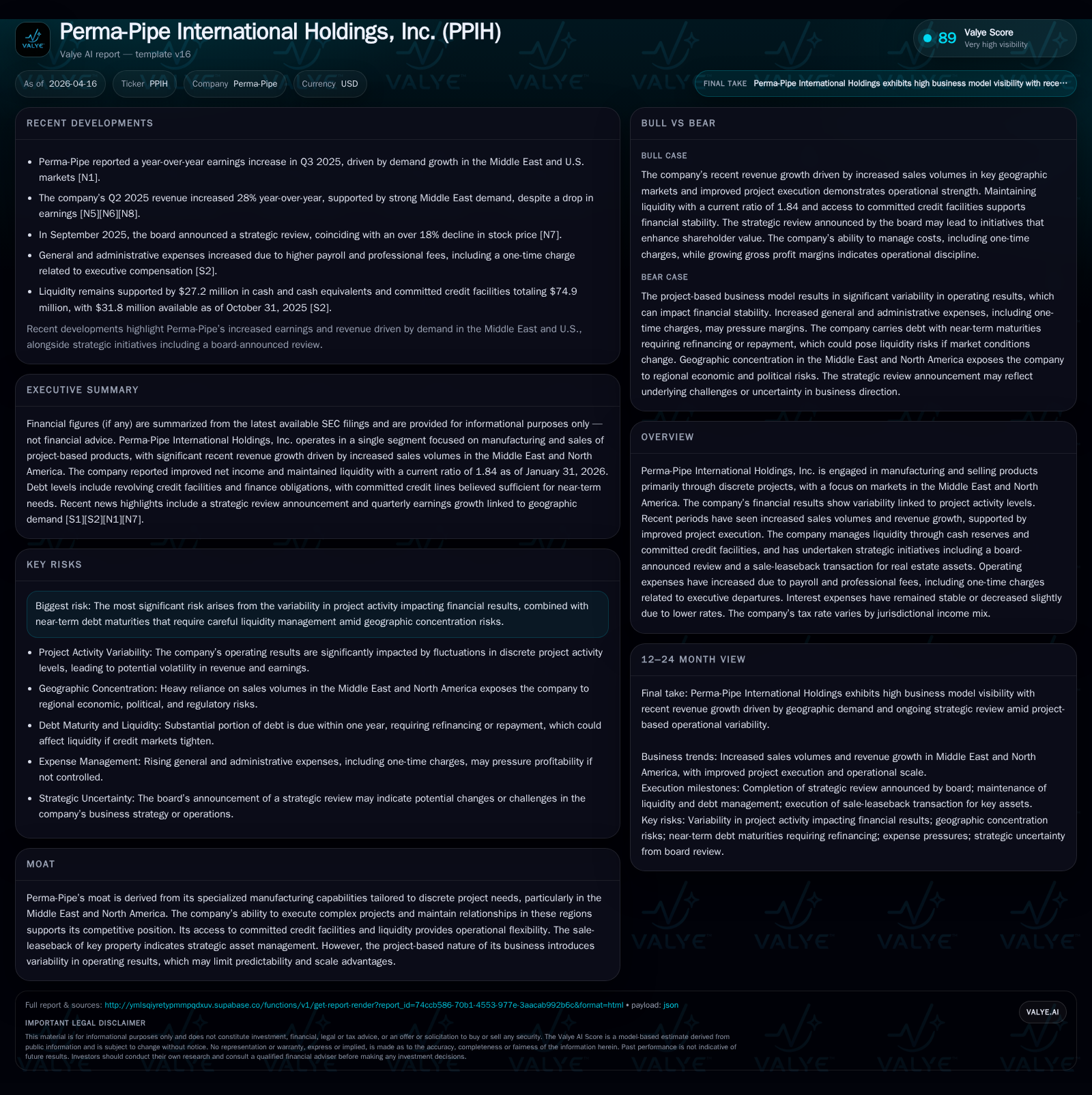

Perma-Pipe’s Project-Driven Revenue Growth and Liquidity Management Define 2025–26 Trajectory

Perma-Pipe International Holdings, Inc. delivers revenue and earnings growth but faces near-term liquidity and project variability challenges.

Perma-Pipe International Holdings, Inc. reported solid top-line growth in fiscal 2025 and further gains in 2026 driven by increased sales volumes and enhanced project execution in key geographic markets including the Middle East and North America. The company’s operating income and net income surged markedly year-over-year, reflecting leverage on higher revenues and operational efficiencies. Liquidity remains sufficient with $27.2 million cash on hand and credit facilities aggregating $74.9 million, but upcoming debt maturities within the next 12 months require careful monitoring. Perma-Pipe continues managing risks inherent in its discrete project business model by securing payment assurances and maintaining strong relationships with regional customers.

Historical Performance and Growth Drivers

Perma-Pipe International Holdings, Inc.'s revenue trajectory over recent years reflects a fluctuating pattern typical of its contract-driven business model focused on specialized infrastructure projects primarily in the Middle East and North America. After a peak revenue near $195 million in FY2014 followed by declines through FY2017, the company stabilized revenues around $100-$110 million annually.

In FY2026 (year ended January 31), Perma-Pipe posted revenue of approximately $105 million, marking a roughly 6.5% increase over FY2025 revenues around $98.8 million [F1]. This growth was underpinned by increased sales volume and improved project execution across core markets reported in the latest annual filing [S1, S3].

Operating income showed strong improvement, rising nearly 45% year-over-year to approximately $29.4 million (vs. $20.3 million in FY2025), indicating improved gross margins coupled with controlled SG&A expenses despite some increases due to payroll and professional fees including one-time costs related to executive transitions [F1], [S15]. Net income followed suit, almost doubling to $17 million in FY2026 from about $8.9 million a year prior [F1].

Despite operational improvements, cash flow from operations declined by around one-third to roughly $9.2 million while capital expenditures more than tripled—to just over $10.4 million—reflecting strategic investments likely aimed at capacity expansion or modernization initiatives [F1]. This divergence led to negative free cash flow near -$1.27 million for the year.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 17 | 9 | 29 | 10 | +89.6% |

| 2025 | 9 | 14 | 20 | 3 | -14.2% |

| 2024 | 10 | 15 | 13 | 11 | +76.1% |

| 2023 | 6 | -1 | 11 | 7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | -1 | 18.8 | |

| 2025 | 0 | 11 | 12.5 |

| 2024 | 942000 | 4 | 15.9 |

| 2023 | 69000 | -8 | 10.3 |

Source: SEC companyfacts cache [F1].

Table: Select Annual Financial Metrics (FY Ended January)

Future Growth Prospects

Looking ahead, Perma-Pipe's growth is closely tied to its ability to secure and execute sizable infrastructure projects which inherently vary between reporting periods due to their discrete nature [S2]. The backlog stood at approximately $121.6 million as of January 31, 2026, predominantly expected to be realized within the next fiscal year, providing visibility though not guaranteed stability given regional geopolitical factors in key markets like the Middle East [S1].

Customer concentration risk remains notable with one client representing about a quarter of accounts receivable at early 2026; however, risk is partly offset through irrevocable letters of credit backing payments and progress billing terms embedded in contracts [S1].

Supply chain management measures have been enacted to mitigate raw material price volatility and availability risks via advanced purchasing strategies and alternative supplier identification—critical steps given global commodity fluctuations impacting infrastructure materials recently [S1].

Capital spending trends suggest ongoing investments that may support incremental capacity or efficiency gains but could pressure free cash flows if not balanced with operating cash inflows or project scaling [F1], [S14].

Forecasts and Milestones

No explicit forward guidance was disclosed for upcoming fiscal years, consistent with the company's historically variable results linked to project timing [N#]/[S#] (none provided). Stakeholders should monitor backlog development updates reported quarterly as well as renewal status of key financing arrangements expiring late calendar year or early next fiscal year for insights into liquidity trajectory.

A critical milestone will be the company's ability to refinance or repay near-term debt obligations totaling roughly $19.5 million maturing predominantly under foreign revolving lines through late 2025 into early 2027 periods—failure could materially impact operations given concentrated credit relationships [S1],,.

Returns and Capital Allocation

On a returns basis, Perma-Pipe posted an approximate return on equity near 18.8% for FY2026 calculated as net income divided by average equity (~$90.6 million equity base) reflecting improving profitability after several years of modest earnings expansion [F1].

The company generated positive operating cash flows but free cash flow was negative due primarily to elevated capital expenditures which rose sharply compared to prior years suggesting a temporary drawdown for investment purposes rather than a structural cash deficit [F1].

Corporate actions such as dividends or share repurchases have been minimal or absent recently; share buybacks ceased after small repurchases in FY2024 following nominal purchases earlier year-over-year indicating current emphasis on conserving liquidity amid debt maturity ladders rather than returning capital to shareholders via buybacks or dividends [F1].

Liquidity and Financial Position

Liquidity remains a focal point as Perma-Pipe held roughly $27 million in cash plus access to committed credit facilities aggregating about $75 million as of late calendar year fiscal data, with approximately $32 million readily available after borrowings against these lines , [F1].

However, substantial current maturities approximating $17 million out of total debt near $30 million signal upcoming refinancing needs within the next twelve months including prominent revolving credit facilities across North America and Middle Eastern subsidiaries facing expiry dates mostly clustered through November 2025 to September 2026 windows ,[S24],. The company is proactively engaged with lenders towards renewal on comparable terms though no guarantees exist.

Furthermore, Perma-Pipe’s sale-leaseback arrangement on real estate assets provides balance sheet flexibility but also obligates ongoing lease payments modeled as finance obligations under ASC842 standards thus not eliminating fixed costs but converting them from ownership liabilities into lease liabilities over a long term horizon through mid-2030s [S13,S23].

Sector Context Analysis (Non-company-specific)

Infrastructure manufacturing firms deploying custom-engineered piping solutions often face lumpy revenue patterns due primarily to large-scale discrete contracts spaced unevenly across reporting periods—a feature that clouds predictability despite longstanding customer relationships especially in geopolitically complex regions such as the Middle East.

Debt management is crucial given that banks tend toward shorter-tenor product offerings for project financing which must be continually renewed or refinanced keeping companies vigilant about covenant compliance and liquidity runway during less active contract phases.

Similarly strategic asset-light transactions like sale-leasebacks are increasingly common among capital-intensive industrial firms seeking balance sheet optimization without relinquishing operational footprint control.

Conclusion

Perma-Pipe International Holdings experienced meaningful financial improvement in fiscal 2025-26 driven chiefly by stronger project execution increasing revenues and earnings significantly albeit accompanied by working capital pressures reducing free cash flow. The firm benefits from strong liquidity buffers including healthy cash balances supplemented by substantial revolving credit capacity but must carefully navigate concentrated customer exposure alongside tightly scheduled debt maturities principally associated with foreign facility renewal risks coming due shortly.

Absent explicit public guidance beyond normal disclosures, investors should track backlog conversion trends alongside financing negotiations as key determinants shaping near-term operational continuity combined with successful internal control remediation initiatives critical for sustaining reliable financial reporting.

This analysis is based exclusively on publicly filed information up to April 16, 2026; it does not constitute investment advice nor incorporate non-public data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments