Build-A-Bear Workshop’s Revenue and Dividend Growth Define 2026 Outlook

Build-A-Bear Workshop demonstrates operational resilience with stable net income and strategic capital returns despite retail sector headwinds.

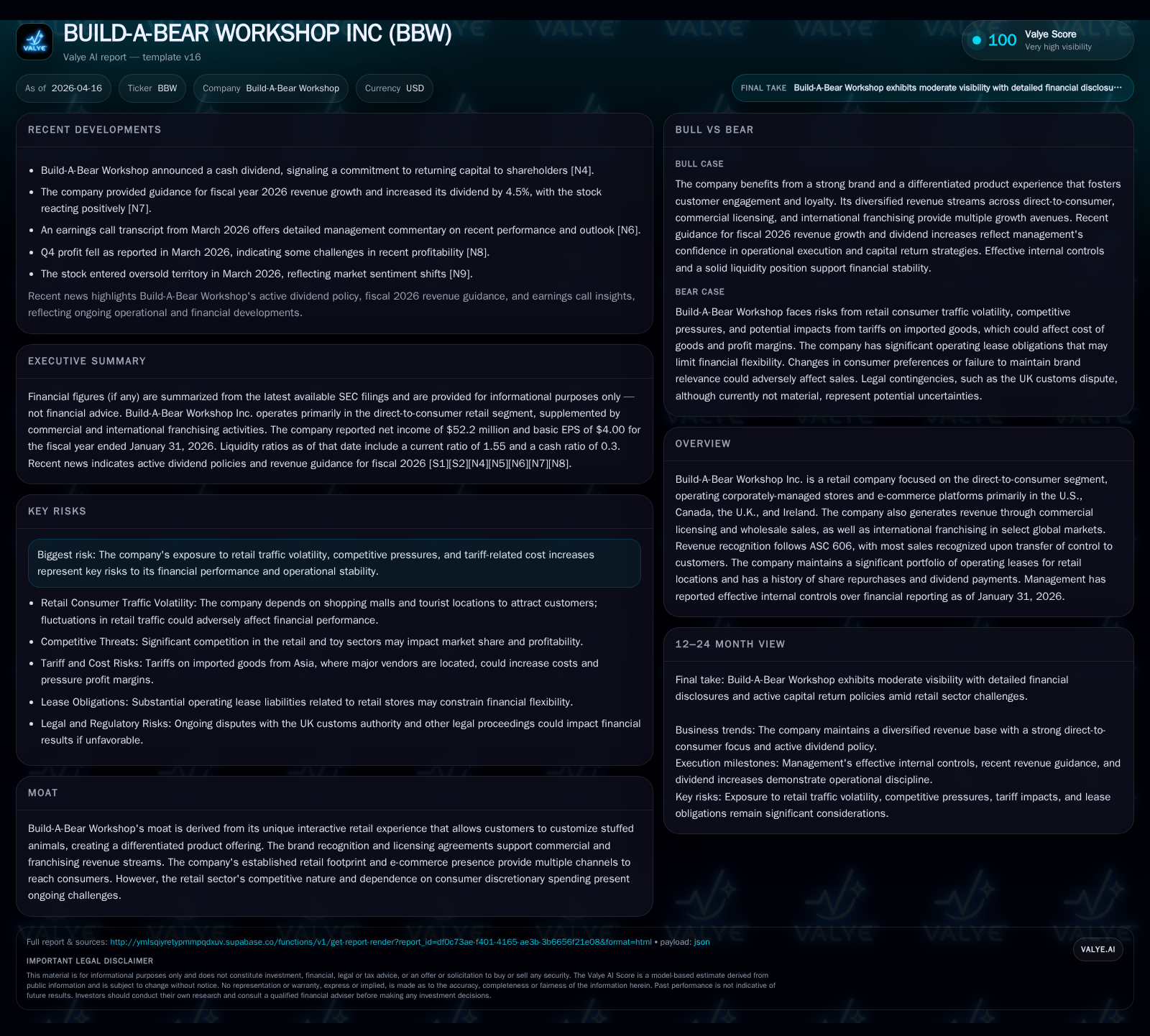

Build-A-Bear Workshop Inc. operates a distinctive retail model centered on customizable stuffed animals, which underpins its moat amid competitive pressures in discretionary consumer spending. The company’s FY2026 financials reflect a slight revenue decline of 1.7% but stable net income growth of 0.8%, supported by a robust 38.2% surge in operating cash flow and an elevated return on equity near 34%. Direct-to-consumer sales dominate revenues, complemented by licensing and international franchising segments that contribute modestly to margins. Management’s recent guidance projects revenue growth for FY2026, alongside a 4.5% dividend increase and continued share repurchases, signaling confidence in steady cash generation despite risks from tariff pressures and retail traffic volatility.

Historical Financial Performance and Growth Drivers

Build-A-Bear Workshop's financial profile over recent years reflects measured stability within a challenging retail sector dominated by discretionary spending fluctuations. The fiscal year ended January 31, 2026, saw total revenues of approximately $530 million, down marginally by 1.7% compared to the prior period [F1]. This modest top-line contraction contrasts with a slight improvement in net income, which rose by 0.8% to about $52.2 million, underscoring operational efficiency gains amid tighter margins.

Operating cash flow experienced a pronounced uplift, climbing 38.2% year-over-year to reach roughly $65 million, driven mainly by improved working capital management and expense controls [F1]. Concurrently, capital expenditures surged by 32.2%, totaling $25.5 million in FY2026—an investment primarily targeted at refurbishing existing retail locations and bolstering the company's digital commerce infrastructure [F1][S20]. Such capex intensity signals BBW's commitment to sustaining its interactive retail footprint alongside evolving e-commerce demand.

The company's return on equity stood near an impressive 33.7%, reflecting effective utilization of shareholder capital combined with consistent profitability [F1]. The balance sheet remains healthy with a current ratio around 1.55, indicating solid short-term liquidity cushioned by cash and equivalents nearing $26.8 million [F1][S27].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2026 | 52 | 65 | 26 | |

| 2024 | 52 | 47 | 19 | -1.9% |

| 2023 | 53 | 64 | 18 | +10.0% |

| 2022 | 48 | 47 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2026 | 12 | 28 | 40 |

| 2024 | 11 | 31 | 28 |

| 2023 | 22 | 21 | 46 |

| 2022 | 0 | 24 | 34 |

Source: SEC companyfacts cache [F1].

Note: Latest figures are based on the most recent full fiscal year data available as of April 2026.

Segment Analysis: Direct-to-Consumer, Licensing, and Franchising

BBW's business is segmented into direct-to-consumer (DTC), commercial licensing (including wholesale), and international franchising operations—all evaluated via contribution margin frameworks by management for resource allocation [S4][S13].

The DTC segment overwhelmingly dominates revenue generation, accounting for about $486 million or roughly 92% of total company sales in FY2026 [S4]. This segment comprises corporately managed retail stores across the U.S., Canada, the U.K., Ireland, alongside BBW's e-commerce platforms where customers enjoy personalized stuffed-animal customization—a key moat feature promoting brand loyalty.

Commercial licensing contributed approximately $39 million in revenues while the international franchising segment added around $5 million in FY2026 [S4], reflecting relatively smaller footprints but diversification beyond core geographies into select markets across Asia, Australia, the Middle East, Africa, and South America [S6][S14]. Contribution margins differ materially between these segments; licensing enjoys higher margins due to lower direct operational costs compared to the brick-and-mortar intensive DTC channel [S13].

BBW’s interactive retail experience is central to its differentiated positioning: customers engaging through store visits or online have low return rates below half a percent due to product customization locking in consumer satisfaction—a notable advantage over commoditized stuffed animal products [S14].

Recent Earnings Review and Market Reaction

In Q4 FY2026 earnings announced March 12, BBW reported a decline in quarterly profits impacted by softer seasonal sales and inventory challenges linked to tariff-driven cost upticks [N8][N2]. Despite this near-term softness, management expressed confidence with upward revised guidance for full-year revenue growth spanning fiscal 2026 accompanied by the announcement of a dividend increase of approximately 4.5%—a reaffirmation of steady cash flow expectations based on underlying fundamentals [N3][N2].

Investor reception favored this optimistic stance; BBW stock rebounded strongly post-earnings with shares surging over 13%, recovering from earlier oversold technical conditions predicated on short-term margin compression fears [N9]. The market appears receptive to BBW's blend of experiential retail resilience combined with prudent capital returns.

Capital Structure, Liquidity, and Capital Allocation Strategy

The company benefits from an enhanced revolving credit facility extended through December 2030 with capacity expanded to $40 million from $25 million previously under amendments executed late calendar year 2025 [S5][S7][S18]. Interest rates were also lowered marginally improving borrowing economics while key covenants remain manageable—requiring maintenance of minimum availability thresholds ensuring liquidity buffers.

Cash holdings stood at nearly $27 million at fiscal year-end providing immediate liquidity backup alongside undrawn credit lines [F1][S27]. Total current liabilities were $90.6 million contrasted against current assets of about $140 million yielding a comfortable current ratio of approximately 1.55 as noted above [F1].

Capital allocation remains shareholder-focused: dividends paid during FY2026 amounted to approximately $11.5 million while share repurchases totaled around $27.7 million under authorized buyback programs continuing from prior years [F1][S9][S22]. The consistency of dividends combined with sizeable buybacks highlights management’s emphasis on disciplined deployment aiming at enhancing per-share metrics supported by robust free cash flow generation estimated near $39.5 million after capex investment [F1].

Outlook: Growth Opportunities and Operational Constraints

Building on its unique experiential format within the specialty toy segment BBW sees sustainable growth fueled primarily through expanding same-store sales productivity alongside incremental contribution from newly opened locations as well as ramping online penetration trends enhancing direct-to-consumer reach beyond physical stores [N3][N4][S10]. Encouraging investment in store refurbishments coupled with marketing initiatives seeks to strengthen brand engagement.

Nevertheless external risks temper outlook upside: tariff costs particularly impact merchandise sourcing from Asian suppliers inflating cost-of-goods sold components hence constraining margin expansion potential despite pricing adjustments efforts documented internally by management discussions during earnings calls [N4][S10]. Moreover consumer discretionary spending uncertainty tied to macroeconomic cycles introduces volatility risk especially relevant given brick-and-mortar store dependency on foot traffic patterns influenced by mall visitation trends and tourism flows impacting DTC performance segments disproportionately relative to commercial licensing which is less exposed stance-wise [S10].[N8]

Risks Impacting Profitability and Strategic Position

Competitive pressures remain acute within specialty retail arenas as numerous entrants vie for limited discretionary budget allocations often favoring digitally native or diversified lifestyle brands challenging BBW's relatively niche positioning focusing predominantly on customized plush stuffed animals [S10]. Furthermore geopolitical tensions influencing international trade regulations add complexity affecting cost structures potentially requiring ongoing mitigation strategies such as supplier diversification or localized production shifts not yet detailed extensively in filings.

Legal proceedings related primarily to regulatory compliance in foreign jurisdictions including an ongoing UK customs dispute highlight operational exposures necessitating provisions though management expects no material adverse impact based on current reserves established at about $3-4 million range associated with this matter [S16].[N8]

What to Watch: Upcoming Milestones and Indicators

Monitoring comparable sales growth metrics across corporately managed stores remains vital given their outsized contribution accounting for over ninety percent of total revenues—fluctuations here would offer early insight into consumer demand sustainability beyond headline revenue figures thus critical for analysts tracking operational momentum independently from licensing revenue streams.

Tracking capital expenditure pacing relative to store upgrade projects or e-commerce platform enhancements will reveal if planned modernization investments continue apace supporting future growth potential intrinsic within omnichannel strategy architecture increasingly pivotal post-pandemic.

Liquidity fluctuations against backdrop of ongoing dividend policies plus buyback cadence will serve as barometers for financial policy rigidity versus opportunistic flexibility amidst any unexpected macro shocks or supply chain disruptions encountered going forward.

Conclusion: Valuing BBW’s Resilience and Strategic Position

Build-A-Bear Workshop presents a compelling portrait of resilience anchored firmly in its interactive customization moat enabling it to sustain profitability amid uneven top-line trends characteristic of its narrowly focused but beloved product offering within discretionary consumer discretionary sector challenges.[F1][S1] Robust operating cash flow improvements paired with evident prudent capital reinvestments into both bricks-and-mortar stores as well as digital channels underpin its capacity for shareholder returns via dividends and buybacks sustainably at current scale.[N3] While risks such as tariff exposure and foot traffic variability impose caution flags aside from general macroeconomic uncertainties,[S10] BBW’s adaptive leasing strategies further offer natural hedges against variable rental costs aiding margin stability. Close attention should continue toward emerging same-store sales performance metrics alongside margin development given sensitivities stemming largely from supply chain cost inputs rather than consumer demand per se.

Disclaimer: This analysis is intended solely for informational purposes without offering investment recommendations or price targets concerning Build-A-Bear Workshop Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments