Data443 Risk Mitigation’s Revenue Growth Contrasted by Persistent Losses and Liquidity Strains in 2025

The company’s expanding customer base and diversified data security portfolio face financial and operational headwinds.

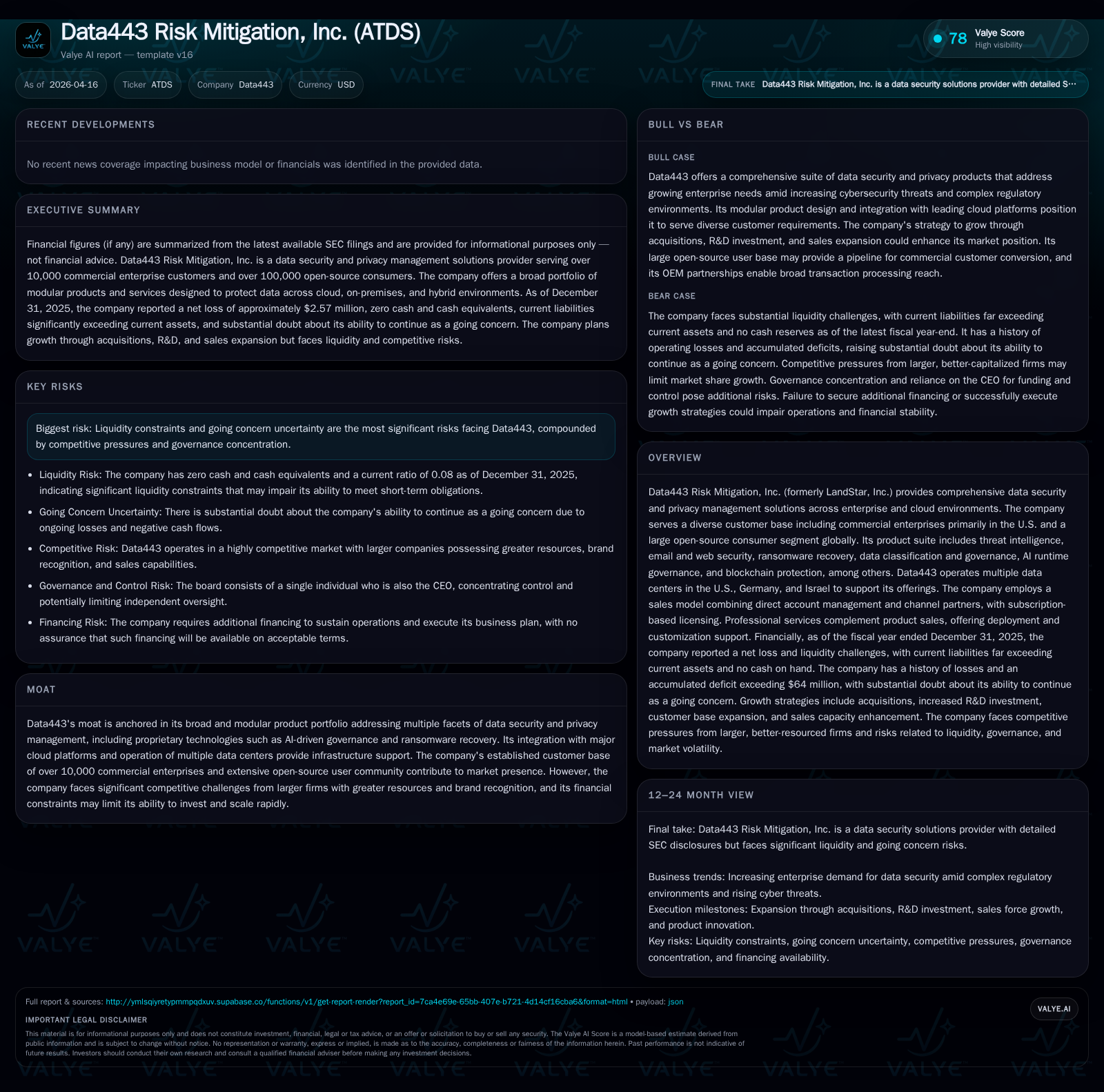

Data443 Risk Mitigation, Inc. reported continued revenue growth driven by a broad suite of data security and privacy products serving over 10,000 commercial customers and an extensive open-source user base. Despite improving operating losses year-over-year by over 30%, the company remains unprofitable with significant negative equity and fragile liquidity, posting a current ratio of just 0.08 at fiscal year-end 2025. Growth prospects hinge on scaling subscriptions, R&D innovation, and channel partner expansion, yet financial constraints and intense competition from larger incumbents cloud execution risks.

Company Overview and Historical Performance

Data443 Risk Mitigation, Inc., formerly known as LandStar, has positioned itself as a provider of comprehensive data security and privacy management solutions across enterprise and cloud environments. With roots dating back to its incorporation in 1998, the company offers a modular suite encompassing threat intelligence (Cyren Threat Intelligence Service), email/web security engines leveraging AI heuristics, ransomware recovery capabilities, data classification/governance solutions (including blockchain protection), as well as privacy compliance platforms such as Data443 Global Privacy Manager tailored to GDPR and CCPA regulations [S1,S3,S11,S15].

Serving more than 10,000 commercial enterprises primarily within the United States alongside over 100,000 globally distributed open-source consumers using freemium privacy plugins expands their market footprint substantially [S3,S9]. Their client base spans industries from financial services to healthcare and retail sectors.

Financial Performance Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | 1002250 | -2 | +57.8% | |

| 2024 | -6 | 1275006 | -3 | 185523 | -43.4% |

| 2023 | -4 | 782101 | -3 | 185523 | +56.3% |

| 2022 | -10 | -1252650 | -4 | 311128 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 17.9 | |

| 2024 | 1089483 | 46.5 |

| 2023 | 596578 | 53.1 |

| 2022 | -1563778 | 110.8 |

Source: SEC companyfacts cache [F1].

Operating income improved by approximately 30% in FY2025 compared to FY2024 while net losses narrowed by nearly 58% [F1].

Operating cash flows have been positive since FY2023 but declined about 21% from FY2024 to FY2025. Capital expenditures stabilized around $185k in recent years after peaking in FY2022 [F1]. Cash and equivalents stood at zero at December 31st, 2025 against $18.2 million in current liabilities resulting in a critically low current ratio near 0.08 [F1]. This creates significant liquidity risk.

Equity remains deeply negative at over minus $14 million due to accumulated losses exceeding invested capital which signals solvency pressures requiring capital restructuring or infusion [F1].

Business Model and Product Suite

Data443 combines subscription-based licensing with professional services including deployment support and customization training. Sales occur through direct account management supplemented by channel partners—resellers and distributors—to extend global reach [S3,S11]. The company also utilizes cloud marketplaces such as Microsoft Azure Marketplace and AWS Marketplace for additional distribution channels [S15].

Key products include:

- Cyren Threat Intelligence Service: Real-time malware/phishing detection via multiple scanning engines.

- AI-Powered Email & Web Security Engines: Detect phishing/spam using advanced heuristics with near-zero false positives.

- Ransomware Recovery & Data Classification: Enable rapid attack mitigation.

- Privacy Compliance Platforms: Manage GDPR/CCPA/GLPD privacy requests via modular WordPress plugins.

- Blockchain Protection Manager: Protects Ripple XRP blockchain transactions from inadvertent data leaks.

- Vaikora AI Runtime Governance Platform: Monitors trusted interactions among autonomous systems using decentralized policies [S11,S12].

These products support hybrid IT environments integrating on-premises infrastructure with virtualization technologies like VMware®, Citrix®, Oracle®, alongside public clouds AWS®, Azure®, and GCP® [S3].

Market Positioning and Growth Drivers

Operating in a highly competitive market dominated by large incumbents with greater capital resources poses challenges. Data443’s competitive edge stems from its breadth of modular products addressing comprehensive data security needs—combining proprietary AI tech with flexible deployment options to serve enterprise data privacy compliance and risk mitigation requirements [S8,S14].

Growth drivers include:

- Increasing complexity of global data privacy regulations driving adoption of turnkey compliance solutions.

- Rising ransomware attacks elevating demand for resilient data protection frameworks.

- Accelerated cloud adoption fueling need for integrated cloud/on-premises data security controls.

- Conversion of open-source users into paying commercial customers through premium feature upsells.

- Targeting mid-market enterprises (>500 employees) with potential for large subscription agreements [S3,S9,S15].

- Expanding sales force capabilities and partner ecosystem globally.

- Pursuing strategic acquisitions to broaden cybersecurity software/service offerings [S11,S15].

Risks Impacting Future Growth Prospects

Challenges include:

- Liquidity Constraints: Zero cash reserves versus high short-term liabilities limits operational flexibility; reliance on founder CEO Jason Remillard’s continued financing support is critical [S1,S7,S26].

- Competitive Intensity: Larger competitors possess deeper R&D budgets enabling faster innovation cycles and stronger channel relationships that may limit market share gains [S8,S14].

- Technology Pace: Rapid technological change requires sustained investment; delayed product enhancements could erode competitiveness [S14].

- Cybersecurity Vulnerabilities: Internal cyberattacks pose reputational risks despite mitigation efforts given adversaries’ sophistication [S10,S21].

- Regulatory Uncertainty: Evolving global privacy laws may necessitate costly product changes or impact customer purchasing behavior if not managed effectively [S16].

- Debt Burden: Secured debt constrains strategic options; potential dilution from debt-to-equity conversions could affect shareholder value [S24,S26].

- Organizational Complexity: Limited staff size (~15 including contractors) adds execution risk amid geographic expansion efforts [S6,S17].

Capital Allocation and Financial Management

The company currently does not distribute dividends or repurchase shares due to its financial condition. Capital allocation prioritizes research & development aimed at innovation alongside acquisitions intended to accelerate product portfolio expansion beyond organic growth alone [S9,S11].

Positive operating cash flow approximates $1.0 million annually while free cash flow after capex is around $817k indicating limited runway absent further financing or increased revenues [F1]. Careful balancing between operational needs and development investments will be essential given liquidity constraints.

Outlook Considerations

While explicit forward guidance is not provided:

- Continued reduction in operating losses would signal progress toward profitability.

- Improvements in working capital metrics or successful capital raises would alleviate liquidity pressure.

- Expansion of sales teams or key customer wins in larger enterprise segments could drive revenue growth.

- Innovations or partnerships especially around AI governance or blockchain protection may enhance competitive positioning.

- Broader channel partner engagement would extend market reach.

- Debt restructuring developments should be closely monitored for impacts on capital structure.

Conclusion

Data443 Risk Mitigation stands at a critical juncture balancing promising technology offerings addressing vital data security challenges against material financial constraints characterized by deep losses and negligible liquidity buffers. Progress narrowing losses alongside positive cash flow generation mark encouraging trends but do not resolve solvency concerns posed by substantial negative equity.

Success depends on executing growth strategies focused on expanding paid subscriptions through enhanced sales efforts while navigating intense competition requiring continuous innovation investments. Founder CEO dependence introduces governance risk amid this pivotal phase. Maintaining adequate capital will be key: failure to secure timely financing could jeopardize capturing opportunities created by rising cybersecurity threats globally.

Investors should evaluate forthcoming quarterly disclosures carefully to assess traction on mitigating financial risks while advancing top-line growth within dynamic regulatory landscapes shaping the sector.

This analysis is based solely on publicly filed SEC documents as of April 16th, 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments