Jocom Holdings Corp.'s AI Platform and Mobile Commerce Ambitions Spur Growth Challenges

Jocom Holdings Corp. leverages patented AI software to reshape grocery analytics, yet financial pressures and client concentration pose growth hurdles.

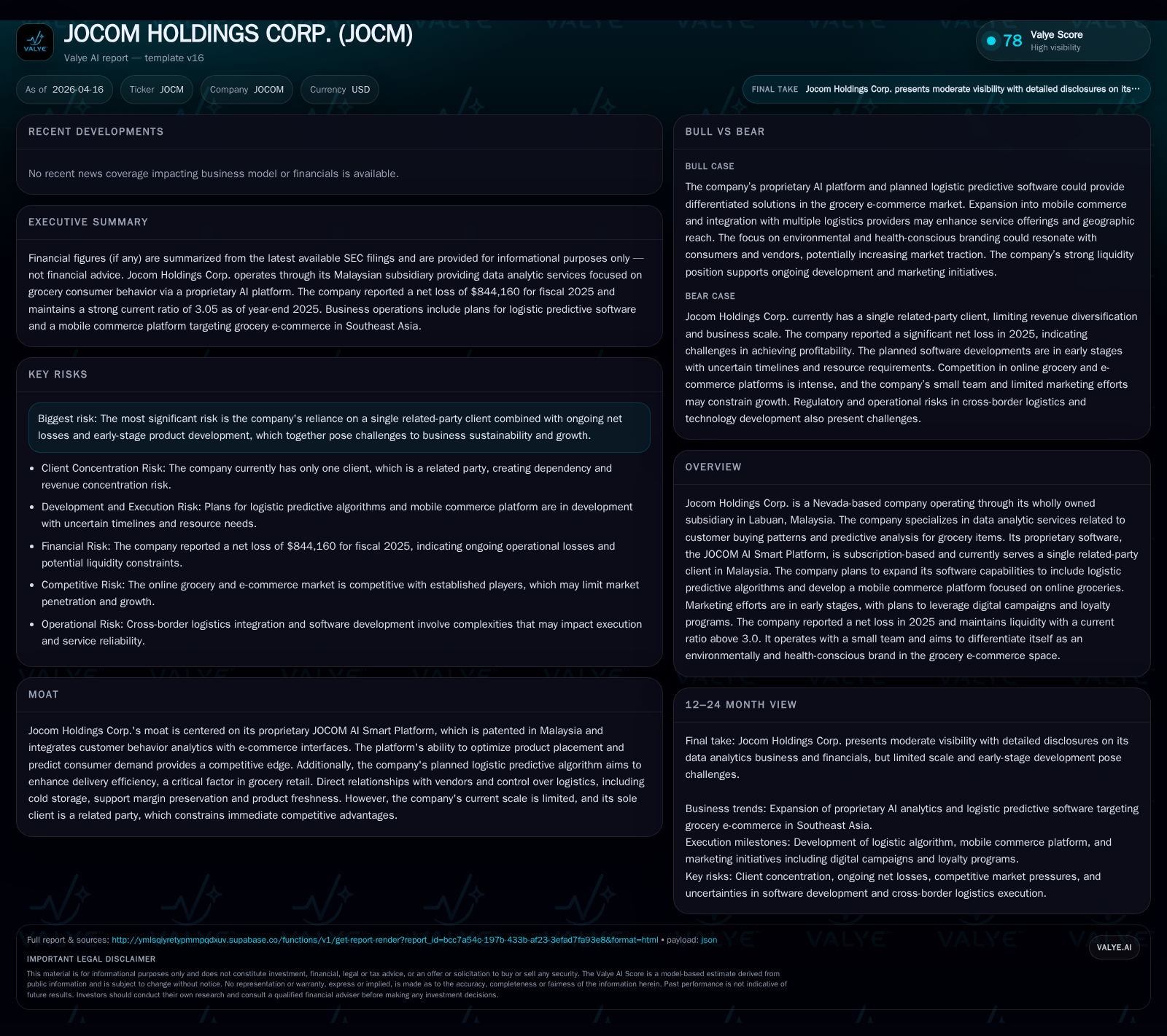

Jocom Holdings Corp. operates a proprietary AI-driven platform for grocery customer analytics primarily serving one related-party client in Malaysia. Despite innovative software capabilities and plans to expand into logistic predictive algorithms and mobile commerce for groceries, the company faces substantial financial losses and operational constraints. Historical financial data reveals fluctuating net incomes and challenging cash flows, while capital allocation has focused on sustaining liquidity rather than returns. Jocom’s single-client dependency amid early-stage product development underscores key risks as it strives to establish a foothold in Southeast Asia’s evolving grocery e-commerce sector.

Tracing Jocom’s Early Growth and Revenue Trajectory

Since its incorporation in early 2021, Jocom Holdings Corp. has exhibited a turbulent earnings trajectory reflective of early-stage tech ventures in emerging markets. The company reported net losses of approximately $428K USD in FY2022, which narrowed significantly by FY2023 to about $157K loss [F1]. In an unusual reversal, FY2024 saw net income turn positive at $68.5K USD, signaling potential initial market traction or operational improvements. However, FY2025 reversed these gains sharply with a net loss ballooning to $844K USD — almost thirteen-fold decline year-over-year [-1332% YoY] [F1].

Operating cash flow (CFO) mirrored this pattern: negative CFO of -$294K USD in 2022 improved slightly but remained negative at -$115K USD in 2023 before turning marginally positive ($2.3K) in 2024, only to deteriorate drastically again to -$491K USD in 2025 [-21648.5% YoY] [F1]. This volatility indicates ongoing challenges translating analytical innovations into scalable revenue streams.

Historical performance (annual)

| FY | Net ($) | CFO ($) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -844160 | -491306 | -1332.0% | |

| 2024 | 68519 | 2280 | +143.7% | |

| 2023 | -156891 | -115318 | 2163 | +63.4% |

| 2022 | -428327 | -294054 | 2163 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 794.6 | |

| 2024 | -99.9 | |

| 2023 | -117481 | 114.4 |

| 2022 | -296217 | 705.0 |

Source: SEC companyfacts cache [F1].

Note: Capex figures are stable but limited; absence of recent investments may reflect capital constraints or strategic focus on software development.

The Proprietary JOCOM AI Smart Platform: Core Driver and Patent Advantages

Central to Jocom’s business model is its proprietary "JOCOM AI Smart Platform," which combines advanced customer buying pattern analytics with SKU forecasting accuracy to optimize inventory levels and enhance product placement strategies for grocery items within Malaysia [S3][S6]. The platform's patent LY2021W02673 secures exclusive rights over this AI-driven analytical approach within Malaysian jurisdiction—a meaningful moat that integrates demand forecasting with e-commerce interface capabilities.

Practically speaking, the platform’s AI engine processes granular demographic data such as gender, age distribution, geographic location, and consumption habits across categories like dry goods, chilled products, frozen items, powders, and liquids. These insights generate monthly production output suggestions tailored by SKU clusters—a capability that can supplant traditional retailer forecasting methods by accelerating sales cycles.

To further amplify value creation for vendors—often not fully familiar with e-commerce complexities—the platform supports supply chain efficiencies through integration with third-party logistic providers (3PLs). It provides real-time stock availability alongside demand prediction models that enable just-in-time inventory management paired with optimized delivery frameworks.

Expanding Horizons: Mobile Commerce and Logistic Predictive Algorithms Development

Beyond analytics alone, Jocom aims to extend its value proposition through development of enhanced logistic predictive algorithms that incorporate inputs like fleet availability metrics, incoming order volumes, road network conditions including potholes or traffic signals, and accident-prone zones—all feeding into a real-time delivery routing system [S4][S6]. This will allow dynamic adaptation of delivery paths optimizing fulfillment speed for perishable grocery products—a crucial differentiator given the sector’s emphasis on freshness and timeliness.

Moreover, plans are underway for a specialized "JOCOM Mobile Commerce Platform" dedicated primarily to online groceries with embedded machine learning capable of user behavior tracking and demand anticipation [S3]. Early marketing initiatives remain nascent but set to accelerate via Facebook campaigns, digital ads, voucher systems and loyalty rewards intended to boost consumer engagement.

Cross-border logistics integration is also envisioned whereby multiple international couriers like DHL or FedEx would be synchronized within the system enabling multi-modal shipment oversight including air/sea freight tracking—an ambitious scope for regional e-commerce expansion within Southeast Asia.

Development remains at an early stage with no definitive timelines or capital estimates available; this creates uncertainty surrounding return on investment pacing [S4].

Financial Performance Deep Dive: Navigating Net Loss Trends and Cash Flow Realities

The oscillating profitability is compounded by strained operational cash flows culminating in an approximate free cash flow deficit of nearly half a million dollars in the latest fiscal year when deducting capex from CFO [F1]. Despite maintaining a notably strong current ratio above 3.0—derived from $371K current assets against $122K current liabilities as of September and December 2025 respectively—the company’s cash & cash equivalents stood precariously low at $11K USD at year-end [F1]. This restricts room for operational maneuvering absent additional financing.

Equity levels remain negative throughout the period analyzed—from approximately -$61K USD in 2022 worsening to around -$106K at end-2025—complicating ROE interpretation though approximated at an inflated figure due to negative equity base distortion [F1]. These figures highlight ongoing balance sheet fragilities despite substantive intellectual property possession.

Capital Allocation Review: Equity, Liquidity, and Absence of Dividend Returns

Capital injections manifest primarily through private share issuances reported in mid-2025 months totaling approximately $500K USD from four separate equity sales priced at $0.10 per share directed toward working capital support [S14][S15][S20][S21][S22][S23]. There have been no dividends declared nor share repurchase programs indicating prudent retention policies aligned with growth funding needs amid sustained losses.

Recent managerial turnover introduced seasoned executives with significant corporate governance experience including Dr. Jimmy Loke as CEO/CFO bringing deep audit and IPO process knowledge—signaling intent to stabilize operations strategically [S24]. Meanwhile dissolution of subsidiary JHC Digital Sdn Bhd in mid-2025 possibly reflects refocusing efforts or shedding non-core activities constraining capital outflows [S1][S10].

All told, capital allocation remains tightly focused on sustaining operational continuity rather than capital returns or aggressive expansion—a typical posture for companies transitioning from product incubation stages toward market scaling.

Competitive Advantages and Challenges within Regional E-Commerce Landscape

Jocom leverages direct vendor negotiations circumventing wholesalers or retail chains aiming to deliver margins near the ~20% mark considered attractive within grocery retail logistics vertically integrated with cold storage facilities ensuring product freshness—a key margin preservation strategy given perishability constraints [S5][S7][S9]. The focus on Asian groceries represents a niche specialization targeting ASEAN markets where fragmented rural producer-vendor networks benefit from digital supply chain unification.

On marketing frontlines plans include geo-targeted push notifications triggered by proximity to local warehouses augmenting consumer outreach into lower IT literacy demographics who traditionally underutilize e-commerce channels—all supported by machine learning for personalized promotions enhancing customer acquisition modeling efficiency [S5][S7].

However competitive intensity remains pronounced due to scale limitations—currently evidenced by sole related-party client dependency—and rapid entry by ecosystem players adopting diversified product assortments without environmental or health-conscious branding differentiators yet articulated by competitors providing some branding protective buffering for Jocom [S5][S7].

Risks on the Horizon: Single Client Dependency and Development Stage Product Risks

The concentration risk deriving from reliance on one related-party e-commerce operator client presents significant business sustainability concerns should contract terms evolve or if market shifts undermine revenue continuity [S8][S11][S12]. This exposure is magnified by the embryonic nature of planned logistic predictive algorithm developments along with nascent mobile commerce platform efforts which require considerable resource investment against uncertain commercialization schedules.

Other operational challenges include talent capacity given only two full-time employees currently supplemented by part-time management complicating rapid scaling possibilities without material headcount expansion expected as operations mature [S9].

Key Milestones Ahead: What Investors Should Monitor

With no explicit formal guidance disclosed by the company, critical indicators moving forward include successful onboarding of new clients beyond the existing related party establishing proof of value outside concentrated revenues; timely deployment milestones for logistic predictive algorithm versions capable of integrating cross-border logistics effectively; ramp-up metrics on mobile commerce active users reflecting traction beyond initial phases; measurable improvement toward positive operating cash flow signaling nascent business model sustainability; as well as marketing campaign effectiveness judged via customer acquisition costs relative to modeled lifetime values.

These benchmarks will collectively validate whether Jocom can transcend its current prototype stage financial strain environment into a scalable profitable entity within Malaysia's burgeoning grocery analytics niche expanding regionally.

Disclaimer: This report reflects analysis based solely on publicly available SEC filings and company disclosures as cited without offering any investment recommendation or price forecast.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments