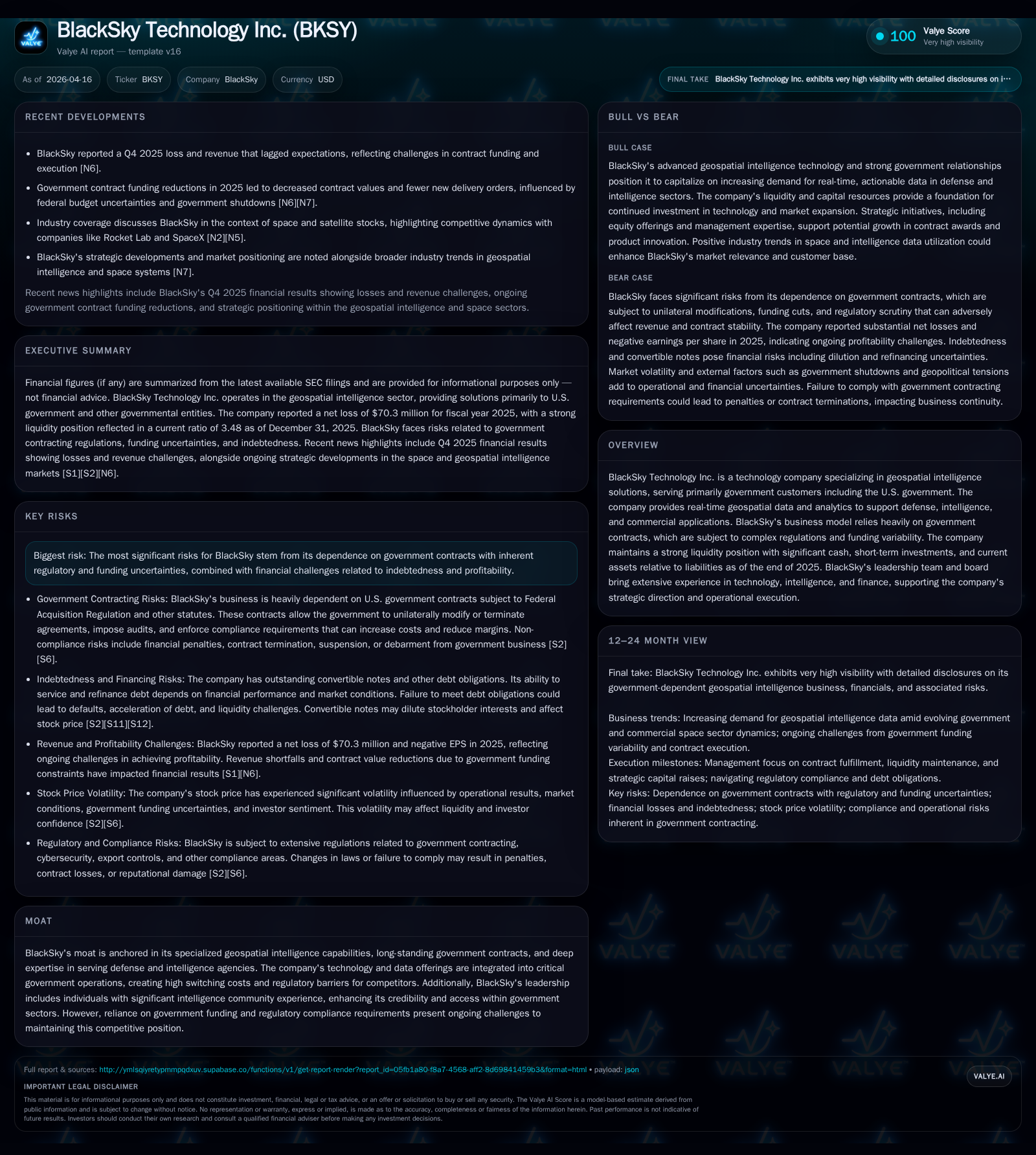

BlackSky Technology: Balancing Strategic Moats and Financial Pressures in Geospatial Intelligence

BlackSky’s entrenched government contract business confronts liquidity and profitability challenges amid evolving regulatory complexities.

BlackSky Technology operates at the intersection of geospatial intelligence and government contracting, leveraging its specialized capabilities and leadership expertise to maintain competitive moats. However, persistent operating losses deepened in 2025 despite narrowing operating income deficits, while net losses and operating cash flow deteriorated. The company’s liquidity remains robust with a strong current ratio, yet its capital structure includes substantial convertible debt that introduces refinancing and covenant risks. Growth prospects hinge largely on government spending cycles and contract awards, constrained by regulatory requirements intrinsic to U.S. federal contracting. Monitoring management changes and quarterly financials will be key to assessing BlackSky’s trajectory amid these headwinds.

The Foundation: Historical Performance Trends and Underlying Drivers

BlackSky Technology exhibits a complex financial profile blending narrowing operating losses with deteriorating net results and worsening cash flows through FY2025 [F1]. Operating income losses decreased steadily from approximately -$86.5 million in 2022 to -$46.9 million by the end of 2025, an improvement suggesting operational efficiencies or cost controls are taking hold. However, net income declined further into negative territory reaching nearly -$70.3 million in FY2025, largely reflecting non-operating expenses such as interest costs related to its indebtedness or adjustments not detailed explicitly [F1].

Compounding concerns is the sharp degradation of operating cash flow (CFO), which swung from a loss of -$6.4 million in FY2024 to a significantly larger negative value of around -$28.3 million in FY2025. This deterioration—over a threefold decline—points to increased working capital absorption or investment outlays exceeding operational inflows, culminating in a free cash flow deficit estimated near -$33.5 million when accounting for disclosed capital expenditures [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -70 | -28 | -47 | -22.8% |

| 2024 | -57 | -6 | -44 | -6.2% |

| 2023 | -54 | -17 | -56 | +27.4% |

| 2022 | -74 | -44 | -87 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -74.1 |

| 2024 | -60.9 |

| 2023 | -57.8 |

| 2022 | -60.9 |

Source: SEC companyfacts cache [F1].

The above data underscores a paradoxical dynamic: while core operational inefficiencies appear somewhat contained (operating loss gradually shrinking), broader income metrics deteriorate due to factors outside pure operations—likely driven by financial costs or strategic investments.

Government Contracts as Growth Engines and Regulatory Hurdles

BlackSky’s commercial model hinges predominantly on contracts with the U.S. government—a source both of competitive strength and inherent risk [S2], [S7]. These contracts are governed by the Federal Acquisition Regulation (FAR), introducing multilayered compliance complexities eg mandatory audits for cost/pricing accuracy and performance reviews that can lead to contract renegotiations or even penalties in case of non-compliance.

The FAR framework grants government agencies unilateral rights uncommon in commercial contracts; these include termination for convenience without prior notice and price modifications triggered by inaccuracies during contract negotiation [S7], [S10]. Moreover, the government retains the ability to cancel multi-year contracts if funding lapses or policy priorities shift—an ever-present tail risk given fluctuating federal budgets [S7]. This regulatory environment fosters elevated switching costs since integrating geospatial platforms within intricate defense ecosystems requires deep technical alignment with mission-critical workflows.

Sector-specific nuances like organizational conflict of interest rules prevent BlackSky from competing for certain follow-on projects if deemed conflicted by federal entities; coupled with mandatory socioeconomic compliance programs (affirmative action mandates, environmental policies), these contribute additional layers of administrative overhead [S7]. The scrutiny extends also through supply chain diligence mandates aimed at ensuring cybersecurity resilience against evolving threats.

Financial Health at a Crossroads: Liquidity, Indebtedness, and Cash Flow Dynamics

Despite reported losses and strained cash flows, BlackSky maintains a commendable liquidity profile exemplified by a current ratio of roughly 3.48 at year-end 2025—the ratio of current assets ($206.8 million) to current liabilities ($59.5 million)—suggesting the firm is well-positioned to cover short-term obligations [F1]. Notwithstanding this buffer, underlying free cash flow weakness signals potential challenges sustaining daily operations without external financing.

BlackSky’s capital structure features notable convertible notes encumbered with complex covenants that impose restrictions on incurring additional debt and outline conditions under which accelerated repayment may be triggered—including defaults on existing debts or fundamental changes affecting contractual terms [S4], [S5], [S6]. This creates a latent risk where failure to comply could cascade into defaults across multiple instruments simultaneously.

Additionally, conversion rights linked to these notes allow settlement in shares or cash; should BlackSky elect solutions involving cash payments at conversion events without sufficient liquidity support or refinancing capacity, it risks breaching indenture terms triggering an event of default [S4],[S12],[S15]. Market conditions impacting credit access could exacerbate refinancing difficulties by elevating borrowing costs or restricting capital raising opportunities.

These dynamics reveal tension between the company’s healthy asset-liability configuration at the balance sheet level and operational challenges manifesting through cash flow deficits compounded by intricate debt service obligations.

Strategic Leadership: Moats Built on Intelligence Community Expertise

BlackSky’s moat derives from its specialized geospatial intelligence technology tightly woven into U.S. defense and intelligence agency missions . The company's leadership comprises individuals with extensive backgrounds inside the intelligence community—providing invaluable domain insights that facilitate trust-building within government corridors often impenetrable to new entrants.

Integration complexity with legacy national security systems engenders steep switching costs for customers while elevating barriers for competitors lacking similar insider knowledge or tailored technical prowess . Government agencies' heavy reliance on BlackSky’s real-time analytics functions as both a moat enhancer via embedded mission dependence and a potential risk given concentrated revenue exposure.

The technology stack involves advanced satellite data assimilation blended with proprietary analytics platforms—factors that coalesce into unique value propositions supporting tactical decision-making across multiple federal agencies; this positions BlackSky as more than a commodity imagery provider but rather as an embedded solution partner.

Growth Outlook: Opportunities Within Constraints

Explicit growth guidance remains limited; however recent market discussions highlight contract award events as proximate catalysts capable of materially influencing revenue trajectories [N10]. With governmental appropriations setting boundaries on spending discretion amid geopolitical volatility and budgetary uncertainty measures such as continuing resolutions impacting new procurement timing [S8].

Innovations targeting automation-driven analytics pipeline improvements could provide incremental competitive differentiation but remain contingent on investment capacity encumbered by current financial constraints [N2]. While expansion into allied international governments is plausible given operational precedents abroad subject to sovereign procurement rules compliance , this avenue is not explicitly quantified.

Hence growth prospects appear tethered closely to cyclical public spending rhythms alongside successful navigation of rigorous procurement frameworks characteristic of the sector.

Capital Allocation Reality Check: Returns, Buybacks, and Cash Management

Capital return activities are muted reflecting financial conservatism amid mounting cash burn pressures [F1], [S24], [S28], [S29]. There have been no recent dividends declared nor meaningful share repurchase activity since FY2020 when cumulative buybacks exceeded $280 million historically signaling prior capacity yet currently inaccessible given fiscal priorities.

Approximate return on equity calculated from FY2025 net deficit (-$70 million) against shareholder equity ($95 million) is negative ~74%, indicating deep structural loss generation relative to invested equity capital [F1]. This level underscores urgent needs for operational refinement or strategic recalibration until profitability inflection points emerge.

The dispersed equity compensation arrangements retained for directors align incentives tightly with longer-term shareholder interests but do not offset immediate revenue-to-profit shortfalls constraining overall capital deployment flexibility.

Looking Ahead: Key Milestones and Market Signals to Monitor

Upcoming monitoring vectors include quarterly earnings disclosures expected throughout 2026 which may offer first insights into margin recovery efforts or worsening trends within working capital management reflecting operational execution improvements or setbacks respectively [N10], [S3].

Notably, executive stability signals warrant attention following the announced resignation of principal accounting officer effective April 24, 2026—transition management effectiveness will influence internal controls environment robustness pivotal for investor confidence amidst ongoing restructuring necessities [S3].

Additionally scrutinizing new contract wins anchored within shifting budget cycles offers real-time barometers on BlackSky's ability to compensate legacy revenue compression effects induced by prior government funding lapses documented late last year [S8]. Insight into debt servicing strategy evolution including capital raising initiatives under revolving credit capacities tied via Sales Agreement filings may also illuminate evolving financial tactical choices supporting liquidity preservation ambitions [S23], [S26].

This analysis synthesizes information disclosed by BlackSky Technology Inc., anchored solely on issued SEC filings and credible news sources up to April 16th, 2026 without speculative forward-looking benchmarks beyond stated facts or contextual industry interpretation consistent with standard financial analysis practices.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments