Grupo Financiero Galicia Rebounds with Accelerated Profit Growth and Risk Management

The Argentine financial services firm achieved robust growth in 2024 through integrated banking operations while containing balance sheet risks amid complex regulatory and market headwinds.

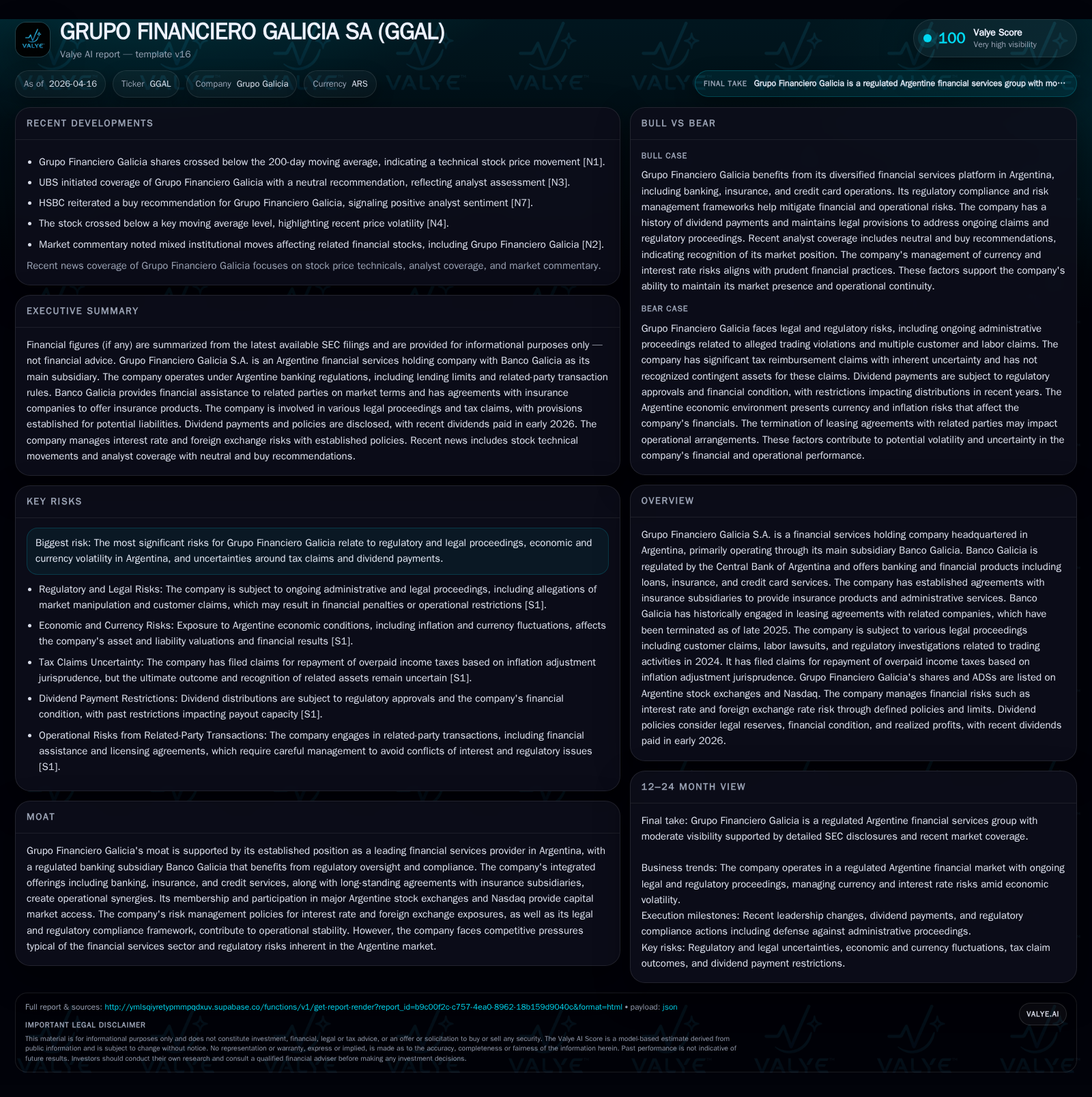

Grupo Financiero Galicia delivered a remarkable rebound in fiscal year 2024, doubling revenue and growing net income by nearly 160%, driven by Banco Galicia’s diversified loan portfolio, strong brokerage margins, and operational synergies with insurance subsidiaries. The company navigated Argentina’s high inflation and volatile exchange rates with disciplined interest rate risk management policies that kept potential losses well below internal limits. Despite ongoing legal proceedings and administrative investigations, Galicia maintained solid capital adequacy and an approximate 27% ROE while pursuing structured dividend payments under Central Bank-imposed restrictions. Institutional governance changes and regulatory dynamics will remain key to monitoring the firm’s future performance.

Financial Surge: Historical Growth Dynamics from FY2023 to FY2024

Grupo Financiero Galicia demonstrated a striking financial transformation in fiscal year 2024, highlighted by revenue reaching ARS 408.7 billion, which more than doubled (+111.7%) compared to ARS 193.1 billion reported in FY2023 [F1]. This explosive growth was mirrored by net income skyrocketing by nearly 160%, from ARS 679.7 billion in FY2023 to ARS 1.76 trillion in FY2024. Equity as of year end also expanded robustly to ARS 6.58 trillion from ARS 4.07 trillion a year prior.

This performance reflects Banco Galicia's effective leveraging of its net portfolio composition that integrates both trading and non-trading assets, predominantly government securities and various loan products including UVA-indexed mortgage loans. The gross brokerage margin (GBM), an important source of financial margin for the bank, benefited from favorable interest rate spreads despite macroeconomic volatility.

The revenue surge was bolstered by increased banking fees, credit card turnover growth facilitated through regional credit card companies, as well as synergies from insurance product distribution agreements with subsidiaries like Galicia Seguros S.A.U., creating cross-selling avenues [S13]. The rapid expansion also coincides with heightened equity market activity on BYMA (Buenos Aires Stock Exchange) where Grupo Galicia is a leading issuer ([S1]).

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 408.7 | 1763.8 | +111.7% | +159.5% |

| 2023 | 193.1 | 679.7 | +1297.4% | |

| 2022 | 48.6 | +56.4% | ||

| 2021 | 31.1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | 26.8 |

| 2023 | 16.7 |

| 2022 | 8.0 |

| 2021 | 10.2 |

Source: SEC companyfacts cache [F1].

Equity and profit figures scaled to billions of ARS; ROE calculated as net income divided by equity for respective years[F1].

Interest Rate Sensitivity and Exchange Rate Exposure: Managing Balance Sheet Structural Risks

Banco Galicia operates within a highly inflationary environment paired with significant currency volatility, necessitating sophisticated interest rate risk controls intrinsic to commercial banking asset-liability management practices [S1][S4]. The institution confronts the structural balance sheet risk arising from mismatches between fixed- and variable-rate assets relative to liabilities.

The bank simulates scenarios altering domestic interest rates by up to +550 basis points for Peso assets among other scenarios for USD (+100 bps) and UVA-indexed liabilities (+200 bps), utilizing historical repricing behavior data [S8]. These simulations inform limits set on potential negative deviations in Gross Brokerage Margin (GBM) within the first year post-risk event.

Concretely, Banco Galicia maintains a loss threshold capped at a maximum of -20% variation in GBM under stressed scenarios but recorded only approximately -2.4% deviation across combined rate shocks as of December 31, 2025 — underscoring resilient risk containment protocols [S1][S19]. This aligns with common regulatory expectations for buffer capital adequacy against market risk exposures.

On foreign currency frontiers, Banco Galicia controls its foreign exchange exposure stringently; at fiscal close in December 2025 its net foreign currency liability position stood at roughly 4.4% of its Regulatory Capital (RPC), well inside BCRA established bounds (-9% max liability allowed) [S7][S17]. This low net liability stance mitigates potential adverse revaluation impacts during Peso depreciations—a critical safeguard given Argentina's FX volatility.

Regulatory Framework and Legal Proceedings Impacting Operations

Grupo Financiero Galicia operates under supervision by Argentina’s Central Bank (BCRA) along with capital markets authority CNV oversight due to its public listings on BYMA and Nasdaq [S1][S21]. Compliance frameworks extend over multiple domains including stringent limits on related-party lending and continuous reporting on credit exposures involving executives and significant shareholders [S13].

The company currently faces several legal challenges:

- Various customer claims spanning issues like fraud attempts on safe deposit boxes and service billing disputes,

- Labor lawsuits alleging employment-related violations,

- Ongoing administrative proceedings initiated by CNV related to alleged market manipulation transactions conducted in early 2024 on certain government securities which led to a reported Ps.23 billion loss claim by BCRA; though the case is contested vigorously with payment offered under "without admission" terms [S6][S10][S21].

Provisions have been prudently established against possible losses arising from these disputes including anticipated class action settlements amounting to sub-billion Ps values [S22]. Management maintains an assessment that these litigations are unlikely to inflict material adverse effects on consolidated operations or financial results but continues close monitoring due to inherent regulatory uncertainties.

Strategic Capital Allocation: ROE, Dividends, and Shareholder Returns

Despite an elevated ROE approximating 27% for fiscal 2024 indicating efficient equity utilization [F1], dividend distributions remain subject to Central Bank regulations aimed at preserving banking system stability amidst inflationary pressures [S9][S11][S16]. For instance, dividends corresponding solely to profits realized in fiscal year ended December 31, 2025 may be distributed up to a maximum cap of 60%, with payments spread monthly through the remainder of the calendar year per BCRA Communication A8410 issued March 12, 2026.

Banco Galicia has historically paid sizeable dividends when feasible — exemplified by total cash dividends paid over Ps.388 billion during fiscal year ending December 31, 2024 — albeit some dividends are deferred or split into installments conditioned upon regulatory approvals and available liquid earnings [S11][S16][F1]. Dividend payments on Grupo Financiero Galicia shares rely predominantly on upstream transfers from Banco Galicia plus earnings from other subsidiaries including credit card issuer Naranja X (which conducts its own dividend payouts subject to tax considerations) [S9][S12].

Share repurchase activity has not been prominently disclosed recently pointing towards retained capital focus rather than repurchasing shares at present levels amidst macro uncertainty.

Future Outlook: Institutional Changes and Market Challenges Ahead

Governance adjustments surfaced early in calendar year 2026 with Banco Galicia appointing a new Chairman of the Board reflecting efforts toward enhanced stewardship amid challenging sector conditions [S2]. Dividend announcements communicated promptly signal commitment toward shareholder value balanced against operational prudence required by external policy constraints [S3].

Looking forward through an analytical lens given current filings:

- Resolution outcomes from ongoing regulatory complaints remain pivotal milestones influencing both reputational standing and operational risk premiums,

- Macroeconomic factors such as sustained inflation trajectories could pressure loan book quality impacting provisioning trends,

- Liquidity management will necessitate continuous alignment with BCRA mandates especially under prolonged currency depreciation stress environments,

- The company’s ability to resume normalized dividend disbursements hinges on sustained profitability coupled with realized (not merely accounting) retained earnings as mandated by Argentine corporate law.

Risk Management Practices Within a Complex Macro Landscape

Banco Galicia embodies comprehensive credit risk oversight consistent with Central Bank requirements entailing rigorous borrower evaluation procedures documented extensively within company disclosures [S1][S6]. Operational controls supplemented by internal audit functions aim at mitigating fraud exposure alongside managing loan concentration across sectors sensitive to Argentina’s economic cycles.

Market risk management tools include parametric Value-at-Risk models calibrated daily incorporating volatilities derived from active trading data ensuring timely identification of adverse price movement potentials primarily concerning Government securities trading portfolios governed under strict maximum tolerable loss policies [S15].

Cross-border exposures enjoy controlled limits based on international credit ratings and transaction types mitigating concentration risks abroad [S15], while ongoing contingency plans prepare for critical scenario actions preserving capital cushions.

Taken together these protocols underpin Grupo Financiero Galicia’s capacity to maintain operational resilience amid frequent Argentine economic policy shifts—optimizing financial margin stability without jeopardizing capital integrity over time.

This report is intended solely for informational purposes based on publicly available SEC filings and company disclosures as of April 16, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments