SOUTHEAST AIRPORT GROUP’s Growth Anchored in Regulated Airports and Diversified Revenue Base

ASR leverages regulated Mexican airports, a strategic Caribbean presence, and U.S. terminals to drive growth amid regulatory constraints.

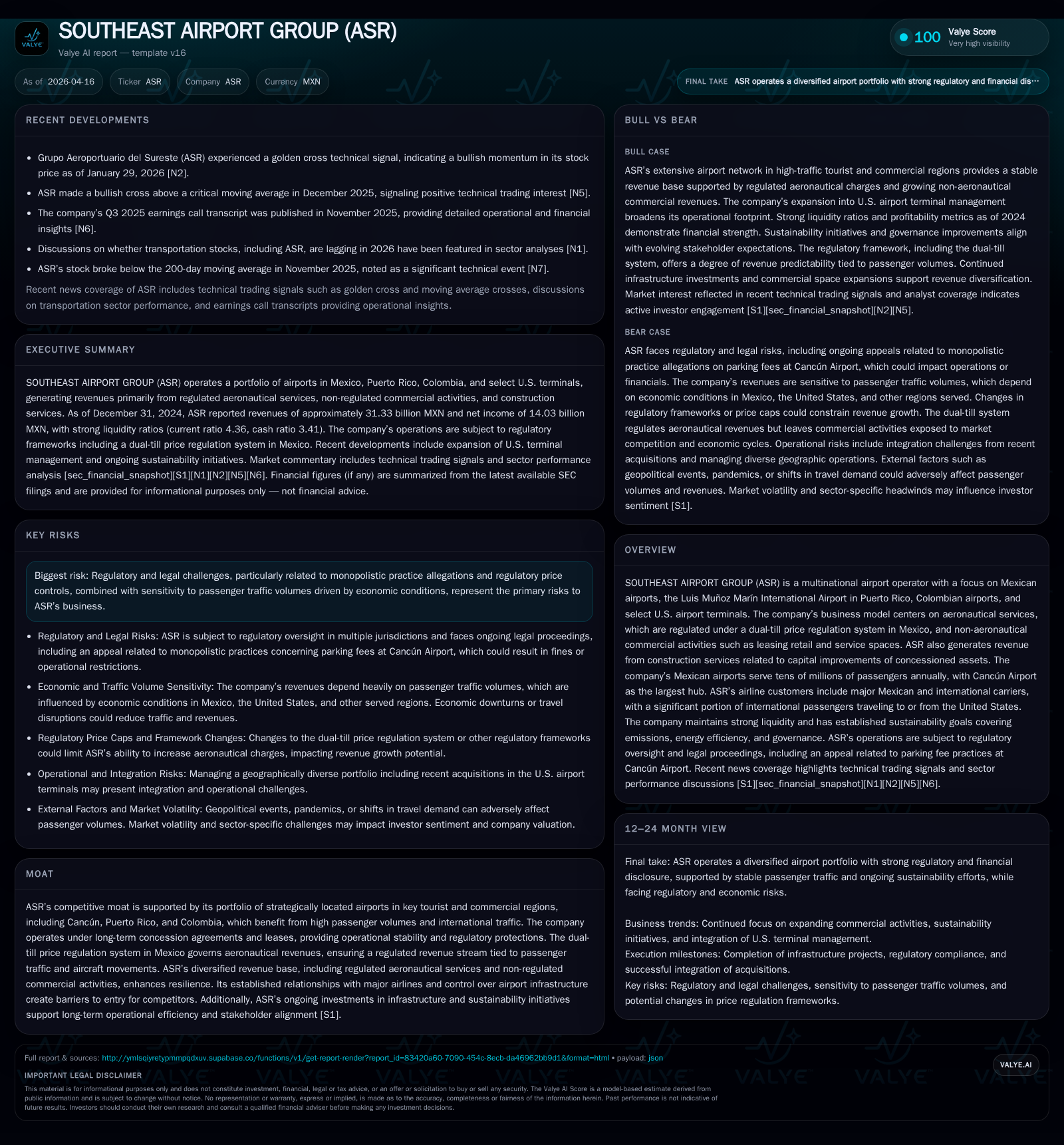

SOUTHEAST AIRPORT GROUP (ASR) operates a portfolio of airports concentrated in Southeast Mexico, Puerto Rico, Colombia, and select U.S. terminals. Its business model balances regulated aeronautical revenues under Mexico’s dual-till system with non-aeronautical commercial activities and construction services related to concession improvements. Historical growth has been strong, fueled by passenger traffic recovery and expanding commercial revenue streams. However, the company faces regulatory rate caps and legal risks that could limit future upside. ASR maintains robust liquidity, invests in infrastructure, and emphasizes sustainability initiatives as part of long-term value preservation.

Company Overview

SOUTHEAST AIRPORT GROUP (ASR) is a multinational airport operator focused primarily on Mexico’s southeast region—including Cancún—but also extending operations to Puerto Rico via its majority stake in Aerostar, Colombian airports through concession agreements, and selected U.S. airport terminals acquired recently through URW Airports LLC [S1][S10][S11]. The company’s model centers around regulated aeronautical services—primarily governed under Mexico's dual-till price regulation framework—coupled with robust non-aeronautical commercial activities such as leasing retail spaces, concessions, and airline service facilities. ASR also participates in construction services focusing on capital improvements within its network of concessioned assets.

Historical Performance

ASR has demonstrated solid top-line growth over the past four years, with revenues rising from approximately 18.8 billion MXN in FY2021 to over 31.3 billion MXN in FY2024 [F1]. This growth was supported by a recovering global travel environment post-pandemic alongside strategic expansion into higher-margin commercial areas and acquisitions. Net income improved correspondingly from 6.4 billion MXN to 14 billion MXN during the same period representing a healthy profitability trajectory.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 31.3 | 14.0 | +21.3% | +31.4% |

| 2023 | 25.8 | 10.7 | +2.0% | +0.3% |

| 2022 | 25.3 | 10.6 | +34.8% | +66.4% |

| 2021 | 18.8 | 6.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2024 | 60 | 22.8 |

| 2023 | 69 | 20.7 |

| 2022 | 34 | 21.7 |

| 2021 | 14.0 |

Source: SEC companyfacts cache [F1].

Revenue is reported in Mexican pesos; growth measured year-over-year where data available [F1]

The key driver of this growth has been the passenger volume rebound at ASR's airports—particularly Cancún Airport—which accounts for around three-quarters of Mexican passenger volume and over three-quarters of its Mexican revenues [S10]. Non-aeronautical service revenues have increased steadily due to growing demand for retail space leasing and associated airport commerce, enhanced by the rise of international travelers primarily from the United States.

Construction services showed significant expansion between FY2023 and FY2025 as capital improvement projects accelerated notably at several key assets [S11].

Regulatory Environment & Pricing Mechanism

ASR's Mexican airports operate under a dual-till regulatory framework where aeronautical services are subject to maximum tariffs set by regulatory authorities based on elaborate inputs including forecast workload units (passengers or cargo), operating costs excluding depreciation/amortization, capital expenditure projections tied to master development plans, discount rates reflecting weighted average cost of capital plus risk premiums, among others [S21][S23]. These maximum rates adjust annually factoring efficiency improvements projected at about 0.8% per year through at least December 2028 [S21].

While this system ensures predictable revenue ceilings linked closely to traffic volumes and operating efficiency, it limits price increases beyond set maximums—even if demand surges—capping some upside potential.

In Puerto Rico, ASR’s subsidiary Aerostar operates Luis Muñoz Marín International Airport under a 40-year lease agreement emphasizing compliance with FAA regulations alongside fixed annual contributions negotiated with signatory airlines [S6][S8]. Aerostar also shares governance responsibilities with co-investors through an amended joint operating agreement paired with financial covenants ensuring prudent liquidity management [S5][S9].

Growth Prospects & Strategic Drivers

Looking forward, ASR’s growth potential primarily lies in:

- Passenger traffic growth in core hubs driven by tourism expansion mainly at Cancún and regional Caribbean destinations.

- Incremental monetization of non-aeronautical commercial activities including expanded retail footprint especially at U.S. terminals newly managed via URW Airports acquisition [S10].

- Construction service revenues from ongoing infrastructure modernization projects across Mexico and Colombia concession networks aimed at capacity enhancement, operational efficiency gains, and quality standards compliance [S22].

- Development of sustainability initiatives detailed in their recent Sustainability Report including carbon neutrality targets potentially unlocking cost efficiencies and regulatory goodwill [N#][S1].

However, these opportunities remain constrained by regulatory ceilings on pricing as well as by external risks including geopolitical tensions that could impact cross-border travel demand notably between Mexico/Caribbean and the U.S., economic fluctuations affecting discretionary travel spenders, or unfavorable changes to airport concession terms.

Financial Position & Capital Allocation

Maintaining a strong liquidity buffer is central for ASR given large capex needs typical for airport operators under long-term concessions [F1][S4][S19]. As of FY2024 end, ASR held over 20 billion MXN in cash and equivalents against current liabilities below six billion MXN—translating into a high current ratio above 4x demonstrating ample short-term financial flexibility [F1].

Capital expenditures have been significant but targeted towards capacity expansions aligned with forecasted passenger load growth supported by regulatory-approved budgets [S18][S22]. The company finances these largely through a mix of internally generated cash flow streams combined with structured financing agreements consistent with maintaining investment-grade credit profiles.

Dividend payments to shareholders have increased over recent years—reaching about $60 million USD in FY2024 from $34 million USD in FY2022—reflecting confidence in sustainable earnings power while balancing reinvestment needs [F1][S20]. Share buybacks or other forms of capital returns were not explicitly highlighted.

ROE estimated at about 23% based on trailing net income relative to equity signifies efficient use of capital within the constraints of regulated returns typical for infrastructure operators [F1].

Risks

Key risks include:

- Price regulation complexities where maximum rates may be adjusted downward if aggregate revenues per workload exceed prescribed limits or penalties arise for pricing breaches [S21][S23].

- Legal challenges accosting monopolistic practice allegations which could lead to heightened scrutiny or revision of concessions.

- Passenger volume volatility influenced by macroeconomic cycles or unforeseen crises affecting travel sentiment.

- Restrictions imposed on ownership transfers within subsidiaries such as Aerostar requiring multi-party approvals potentially limiting strategic flexibility [S6][S7].

- Compliance obligations stemming from aviation authorities (FAA/TSA) especially concerning safety standards and concession conditions.

What to Watch / Analysis

Absent explicit company guidance for near-term periods given latest filings up to April 2026 [N#][S#], observers should monitor:

- Passenger traffic trends especially out of Cancún and Puerto Rico given their contribution weight.

- Regulatory updates around maximum tariff adjustments after December 2028 horizon or changes driven by political shifts.

- Progress on sustainability objectives as fulfillment rates may impact operating costs or access to green financing options.

- Expansion moves into other Latin American markets or additional U.S.-based terminal management contracts broadening commercial diversification.

- Effects of any litigations or government investigations tied to concession policies or compliance matters.

Collectively these factors will shape ASR’s capacity to sustain growth within its unique position straddling heavily regulated markets but benefiting from captive demand within prominent tourist gateway airports.

This analysis synthesizes publicly filed financial statements, regulatory disclosures, and operational descriptions pertaining to SOUTHEAST AIRPORT GROUP as of April 2026 without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments