VINCE HOLDING CORP. Returns to Profitability Supported by Licensing Partnership and Channel Diversification

Vince stabilized operations after brand rationalization and a strategic licensing deal, returning to net income in fiscal 2025 with evolving channel strategies.

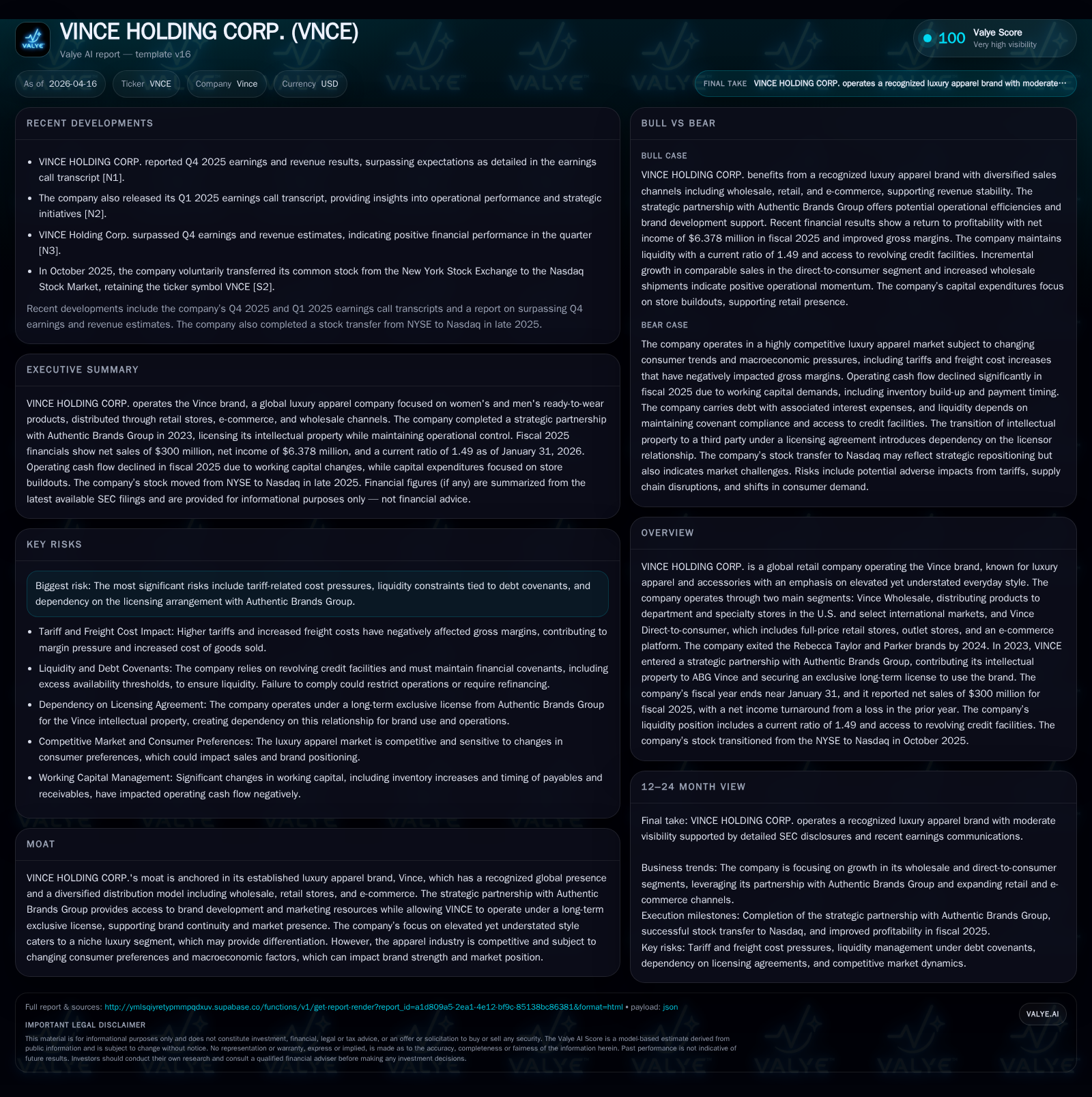

VINCE HOLDING CORP. reported $300 million in net sales for fiscal 2025, achieving a net income of $6.4 million compared to a loss the prior year, driven by a pivot towards the core Vince brand and a critical licensing partnership with Authentic Brands Group. The company operates through wholesale and direct-to-consumer segments, including retail stores and e-commerce, while having exited the Rebecca Taylor and Parker brands by 2024. Despite positive earnings, operating cash flow declined due to working capital changes and tariff-related cost pressures. Capital expenditures remain stable, focusing on retail presence enhancement. The company maintains liquidity via an $85 million revolving credit facility but faces risks from leverage constraints and reliance on its licensing arrangement.

Company Overview and Brand Strategy

VINCE HOLDING CORP. operates as a global luxury apparel retailer focused solely on the Vince brand following divestitures of its formerly owned Rebecca Taylor and Parker brands completed by mid-2024 [S1][S2]. Established in 2002, Vince is known for its elevated yet understated apparel and accessories targeting consumers seeking effortless everyday luxury style.

The company’s business structure is organized into two reportable segments:

- Vince Wholesale: Serving U.S. department stores and specialty retailers along with select international markets.

- Vince Direct-to-Consumer: Encompassing full-price retail stores (43 locations), outlet stores (12), plus e-commerce platform vince.com.

This multi-channel approach facilitates diversified customer access points but also requires integrated inventory management and brand consistency across physical and digital environments.

Strategic Partnership with Authentic Brands Group

In April 2023, VINCE entered into a transformational deal with Authentic Brands Group ("ABG"), transferring ownership of intellectual property rights related to the Vince brand to ABG’s subsidiary ("ABG Vince") for cash consideration coupled with a membership interest in ABG Vince [S1]. Concurrently, VINCE secured an exclusive long-term license to continue operating under the Vince brand within defined territories and accounts via this licensing agreement.

This partnership is crucial as it offloads certain IP ownership risks while granting VINCE enhanced marketing support capabilities accessible through ABG's platform, which manages portfolios of lifestyle brands globally. This licensing model aligns VINCE’s revenue generation focus more toward brand operation excellence rather than IP asset holding.

Historical Performance Drivers

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6 | 3 | 9 | 4 | +133.5% |

| 2024 | -19 | 22 | -17 | 4 | -174.9% |

| 2023 | 25 | 2 | 32 | 1 | +166.4% |

| 2022 | -38 | -19 | -25 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | 12.7 |

| 2024 | 18 | -45.6 |

| 2023 | 0 | 54.0 |

| 2022 | -22 | -189.3 |

Source: SEC companyfacts cache [F1].

Fiscal years end near January each year; revenue figures specifically disclosed for fiscal 2025 converge around the reported ~$300M sales milestone discussed during earnings [F1][N3][S1]. Operating income reversed from losses in prior two years driven partially by cost streamlining post-brand exits and royalty/licensing model benefits from ABG partnership.

Financial Results for Fiscal Year 2025

VINCE reported net income of $6.4 million in fiscal 2025 versus $19 million net loss last year, marking a definitive earnings turnaround anchored by operational efficiencies and revenue stabilization [F1][N3]. Operating income turned positive at about $9.2 million from a substantial loss in fiscal 2024 [F1].

However, operating cash flow decreased significantly to roughly $3 million from over $22 million last year due largely to working capital absorption—mainly inventory buildup influenced by tariff-cost pressures as well as increased accounts receivable balances amid disruptions in wholesale partner repayments such as those highlighted by Saks' reorganization impacts [F1][S1].

Capital expenditures remained consistent near $4.3 million annually dedicated largely toward store improvements including leasehold upgrades reflecting continued investment into physical retail footprint quality despite increased costs associated with inflationary pressures globally [F1][S1].

Balance Sheet & Liquidity Position

Liquidity remains centered around the company's recent revolving credit facility:

- An $85 million senior secured revolving credit facility arranged mid-2023 maturing June 2028 provides operational funding flexibility [S9][S10].

- As of January 31, 2026, borrowings stood at approximately $10.7 million against this line with letters of credit totaling about $6.2 million available but unused capacity remains robust at nearly $40.8 million net availability after loan caps are accounted for [F1][S13].

- VINCE's total long-term debt aggregates roughly $19.5 million combining revolver borrowings with subordinated third lien term loans totaling near $8.8 million payable primarily in kind interest at high spreads arising from legacy restructuring arrangements endorsed by prior controlling shareholders Sun Capital before majority stake acquisition by P180 Holdings in early 2025 [S16][S20][S22].

The balance sheet shows equity expansion supported by cumulative retained earnings post-profit recovery lifting book value north of $50 million from approximately $42 million last year reflecting capital preservation efforts through brand exits combined with new ownership's operational realignment strategies [F1].

Future Growth Prospects & Constraints

Growth drivers depend critically on:

- Wholesale channel expansion within solidified departmental relationships domestically as supply chain normalizes post-pandemic disruptions.

- Direct-to-consumer channel innovations, particularly enhanced omni channel integration between brick-and-mortar stores and ecommerce platforms to capture evolving consumer shopping habits.

- Leveraging Authentic Brands Group's marketing infrastructure is expected to accelerate brand recognition investments beyond VINCE's internal resource limits allowing entry into new geographies or market segments.

Conversely, growth faces capping factors including:

- Intense competition within luxury apparel balancing trend volatility against core design DNA requiring continual innovation.

- Tariff-induced cost pressures remaining an uncertainty given ongoing geopolitical trade tensions impacting sourcing predominantly in Asia where most manufacturing occurs [S21].

- Licensed IP dependency introduces operational risks—any disruption or non-renewal could hamper brand use rights essential to business continuity.

- Debt covenant restrictions limit dividends or share buybacks currently until July 2026 contingent on fixed charge coverage ratios meeting targets placing temporary brakes on capital return policies despite improving profitability metrics [S14][S15].

Returns & Capital Allocation

The approximate return on equity for fiscal 2025 stood near a moderate 12.7%, indicating modest profitability relative to equity invested especially following restructuring gains reversing multiyear losses ([F1]).

Free cash flow was negative around $(1.3) million reflecting operating cash flow shortfalls vs stable capex outlays pointing to short-term liquidity absorption linked mainly to inventory management nuances rather than operational losses per se ([F1]).

Dividend payments or share repurchases have been restricted per credit agreements; no financing costs were incurred during fiscal 2025 suggesting conservative financial stewardship amid ongoing debt amortization plans ([S17]). Capital discipline is evident given continued investments into retail experiences alongside cautious liquidity maintenance.

What to Watch Next (Analysis)

Future quarterly updates should be monitored for:

- Trajectory of comparable direct-to-consumer sales blending e-commerce alongside physical retail especially if further store remodels or openings occur.

- Wholesale channel demand signals from major US department stores adapting post economic cycles deeply tied to premium discretionary spending.

- Impacts from tariff mitigation initiatives possibly altering gross margin profiles amidst foreign production cost inflation.

- License agreement renewal terms or any amendments that might reshape intellectual property controls underpinning VINCE's operating license rights over the medium term.

- Progress toward lifting payment restrictions triggered by debt covenant improvements enabling potential returns enhancements through dividends or buybacks.

Inherent volatility characterizing luxury fashion consumer preferences demands ongoing innovation backed by strong brand identity cultivation combined with managing external shocks related to trade policies which could otherwise compress margins sharply.

Conclusion

VINCE HOLDING CORP.'s path back into profit territory underscores effective refocusing around its flagship Vince brand complemented by structural licensing capabilities afforded through its collaboration with Authentic Brands Group—a model increasingly prevalent among mid-size apparel players balancing asset-light positioning while leveraging scalable marketing platforms. Nonetheless, significant execution challenges persist primarily related to operational cash flow dynamics challenged by tariffs alongside stringent leverage constraints limiting financial flexibility even as top-line stability returns. Strategic vigilance remains warranted regarding evolving macroeconomic factors influencing discretionary apparel spend along with careful management of licensing dependencies shaping the firm’s competitive positioning going forward.

This report is based solely on publicly available information up to April 16, 2026; it contains no investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments