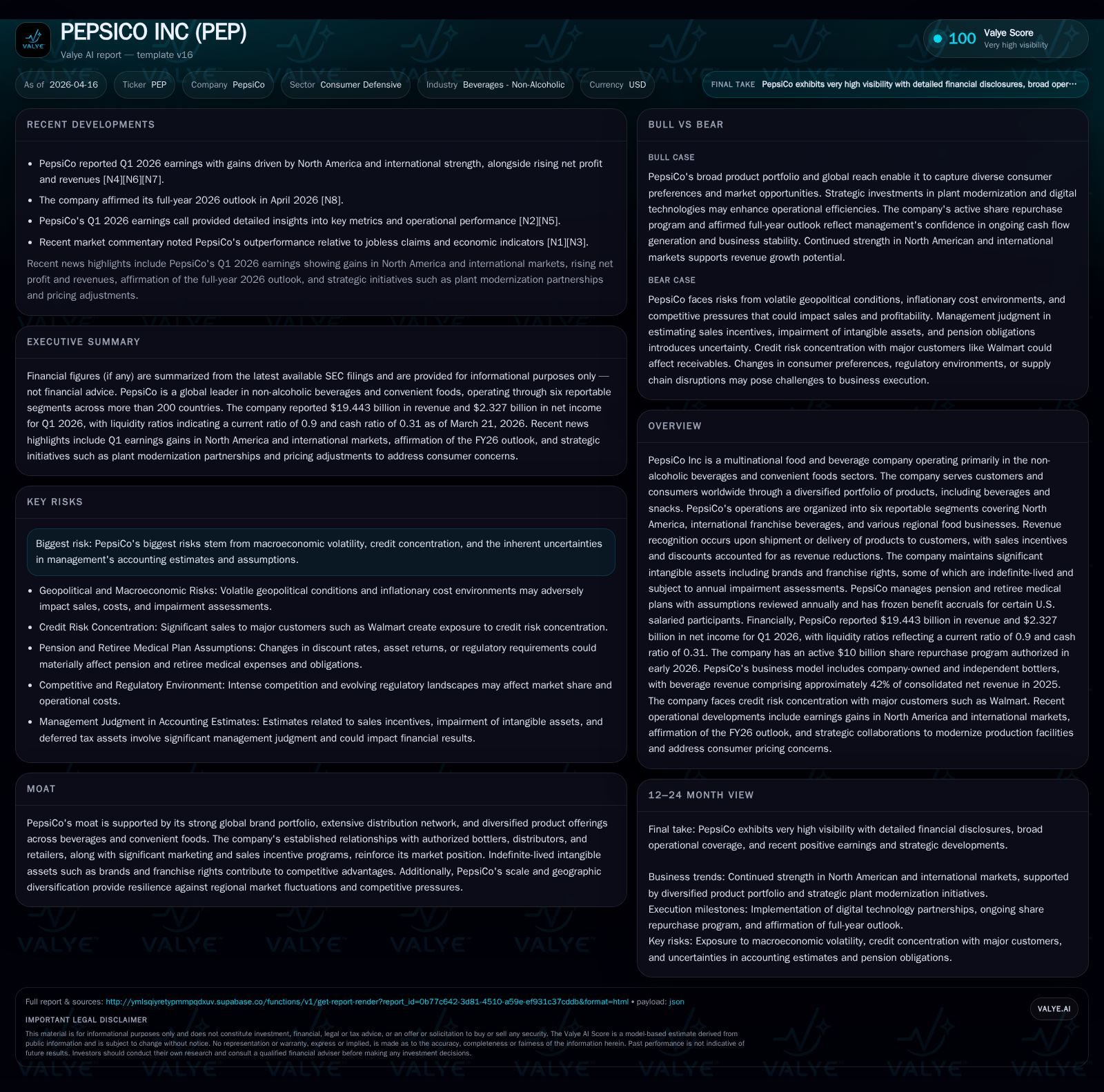

PepsiCo Inc’s Shifting Profitability and Growth Dynamics in 2025

A robust revenue expansion contrasts with profit compression as PepsiCo faces margin pressures while balancing capital returns and investments.

In 2025, PepsiCo achieved steady revenue growth driven by strong brand appeal and geographic diversification, yet experienced notable declines in both operating and net income. Margin contraction stemmed from elevated input costs and intensified sales incentive programs, impacting profitability despite resilient cash flows. The company maintained disciplined capital allocation through dividend growth and continued buybacks, supported by a solid balance sheet. Going forward, monitoring how well PepsiCo manages cost inflation, pricing power, and investment execution will be critical to its growth trajectory.

Revenue and Earnings Trends: Examining the 2025 Inflection Points

PepsiCo's top-line resilience persisted through 2025 with total revenues reaching approximately $93.9 billion, marking a year-over-year increase of nearly 2.3% from $91.85 billion in 2024 [F1]. This growth was achieved against a backdrop of modest economic expansion and evolving consumer preferences within non-alcoholic beverages and convenient foods.

Despite the positive revenue momentum, operating income receded sharply by about 10.8% to nearly $11.5 billion in 2025 from $12.9 billion the previous year, illustrating notable margin compression [F1]. Net income saw an even steeper decline of approximately 14%, falling to $8.24 billion from $9.58 billion annually [F1]. Operating cash flow (CFO), while still strong at roughly $12.1 billion, contracted by over 3%, highlighting the impact of increasing working capital requirements and selective cost control measures [F1]. Capital expenditure was cut back significantly by roughly 17% to $4.42 billion, reflecting disciplined investment amid inflationary cost pressures [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 93.9 | 8.2 | 12.1 | 11.5 | +2.3% | -14.0% |

| 2024 | 91.9 | 9.6 | 12.5 | 12.9 | +0.4% | +5.6% |

| 2023 | 91.5 | 9.1 | 13.4 | 12.0 | +5.9% | +1.8% |

| 2022 | 86.4 | 8.9 | 10.8 | 11.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 7.6 | 1000 | 7.7 |

| 2024 | 7.2 | 1000 | 7.2 |

| 2023 | 6.7 | 1000 | 7.9 |

| 2022 | 6.2 | 1500 | 5.6 |

Source: SEC companyfacts cache [F1].

Table: PepsiCo Historical Financial Summary showing revenue growth contrasted with declining profitability metrics over three fiscal years [F1]

The divergence between revenue strength and profitability erosion raises questions about underlying cost pressures and strategic execution.

Segment-Level Performance and Geographic Contributions

PepsiCo operates across six reportable segments including distinct North American beverage (PBNA), North American foods (PFNA), international beverage franchises, EMEA operations, Latin America Foods, and Asia Pacific Foods [S8], [S12]. In recent quarters, gains in the North American beverage business were notable contributors to overall revenue improvement as reported in earnings calls [N1], [N2]. The international franchise model plays a complex role; bottler funding programs designed to support marketing efforts appear to influence reported revenues through annual-volume target rebates that may compress net realizations [S1], [N1]. These franchise agreements create a balancing act between volume stimulation via funding incentives and margin dilution.

The company’s strategy leverages differentiated regional unit economics — for instance, beverage business margins differ materially between company-owned bottlers and franchise models due to varying fixed versus variable cost structures [S11]. Geographic diversification provides some mitigation against localized inflationary or competitive pressures; however, currency fluctuations have also impacted margin profiles recently [N1]. Given reliance on key retail partners who account for significant consolidated sales share (e.g., Walmart representing ~14%) [S8], sustained relationship management is critical.

Drivers Behind Margin Compression and Operating Income Decline

Margin deterioration emerged as a central theme for PepsiCo's financials in FY25 primarily driven by input cost inflation spanning agricultural commodities, packaging materials, and energy costs [S11], [N1]. Beyond direct product costs, expanded market spend on sales incentives—particularly bottler funding encompassing advertising support—constitutes a sizable component of selling expenses treated as revenue reductions under accounting policies [S1]. Such expenditures are based on estimated customer participation reconciled post-fiscal year-end.

Management highlighted that commodity price volatility along with strategic marketing commitments necessitated careful trade-offs on pricing actions versus retail price investments leading to compressed operating margins [N1], [N4]. Foreign exchange headwinds also weighed on results amid significant international exposure.

Sustaining profitable growth thus hinges on navigating these inflationary dynamics without compromising brand equity or volume momentum.

Capital Allocation Strategy: Dividends, Buybacks, and Investment Priorities

PepsiCo continues its hallmark commitment to returning capital prudently while supporting organic growth drivers through investments.

Dividend distributions expanded steadily reaching approximately $7.64 billion for FY25 up from $7.23 billion in FY24 reflecting ongoing shareholder yield focus [F1], [S4], [S7]. Share repurchases were steady at around $1 billion annually but notably declined from prior higher-dollar buyback levels suggesting cautious liquidity prioritization amid margin headwinds [F1], [S4]. The recently authorized $10 billion repurchase program commenced early February demonstrates board confidence balanced with cash flow discipline through at least early-2030 timeframe [S4].

Capital expenditure scaling back by roughly a sixth relative to prior year reflects targeted reinvestment in automation, supply chain enhancements, and R&D aimed at accelerating innovation velocity without overextending capex outlays during uncertain macroeconomic conditions [S16].

Balance Sheet Strength and Liquidity Metrics in Context

As of Q1/26 reporting dates, PepsiCo holds cash and equivalents near $10.5 billion alongside current assets approximating $30.9 billion against current liabilities of about $34.5 billion yielding a sub-1 current ratio (~0.9) which signals short-term liquidity pressure but is contextually offset by solid operating cash generation capacity [F1], [S6], [S23].

Debt maturities are well managed with staggered senior note obligations carrying coupon rates mostly below market averages for consumer staples peers indicative of prudent credit stewardship reflecting investment-grade rating norms [S6], [S19]. The company’s revolving credit facilities totaling up to $10 billion offer ample liquidity buffer for working capital needs or opportunistic acquisitions if assessed valuable under prevailing market conditions [S20], [S21].

Maintaining this financial flexibility supports defensive resilience amid episodic margin headwinds projected near term.

Outlook and Key Milestones to Monitor Through 2026

PepsiCo reaffirmed its FY26 guidance emphasizing sustained top-line growth aspirations coupled with improved operating leverage prospects contingent upon effective cost management initiatives highlighted during Q1 earnings commentary [N11].

Absent explicit numerical guidance updates beyond affirmation, key performance indicators warranting tracking include quarterly sequential revenue trends especially within high-growth emerging markets segments; stabilization signals in gross margin expansion reflecting input cost normalization or pricing optimization; and cadence of share repurchases executed versus announced plans as a proxy for free cash flow confidence.

These milestones will help contextualize PepsiCo’s ability to reverse recent profitability drags while nurturing long-term sustainable growth vectors.

Risks Embedded in Macroeconomic and Accounting Assumptions

Core risks detailed in SEC filings underscore PepsiCo’s exposure to macroeconomic volatility that can swiftly alter consumer demand patterns or input cost baselines impacting projections initially based on historical patterns plus management judgment inputs such as sales incentives accruals estimations subject to annual reconciliations post-delivery volumes accruals recognition policies [S1], [S2].

Accounting estimates around indefinite-lived intangible assets—particularly brand valuations—require periodic impairment assessments influenced by fluctuating market shares or consumer preference shifts amid geopolitical tensions or regulatory changes complicate earnings quality visibility.

Pension plan assumptions further introduce variability given discount rate sensitivity affecting annual expense recognition highlighting complexity layered within reported profitability metrics.

Investors should maintain awareness of these embedded uncertainties when evaluating reported financial outcomes or attempting forward extrapolations.

This analysis synthesizes publicly filed SEC documents and recent earnings transcripts without offering investment advice or projections beyond stated company disclosures.[F1][N1][N2][N4][N11][S1][S2][S4][S6][S7][S8][S11][S16][S19][S20][S21][S23]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments