Masco Corp Elevates First-Quarter Sales Despite Tariff Headwinds

Masco reports solid Q1 2026 sales growth led by Plumbing Products despite inflation and tariff pressures.

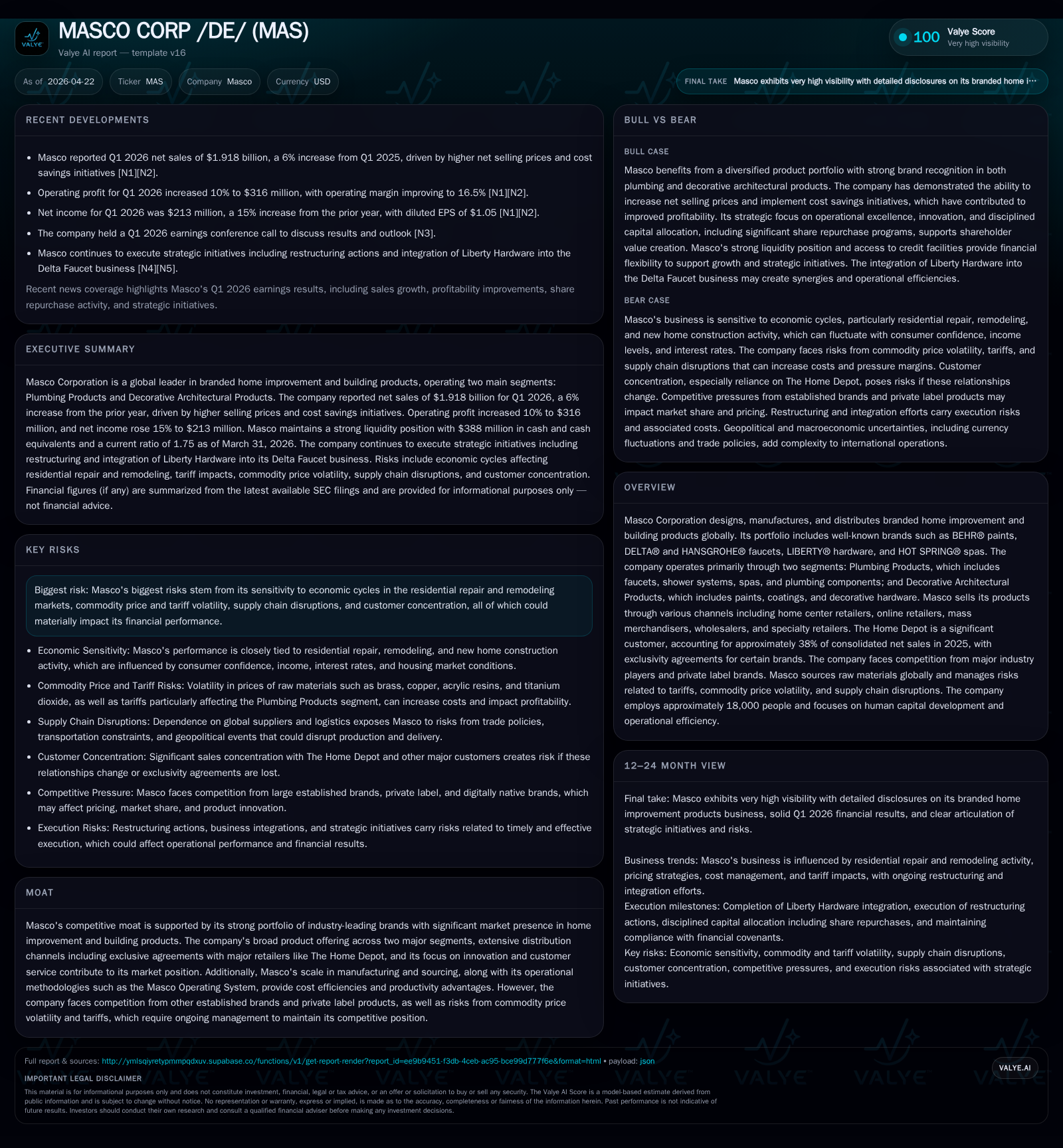

In Q1 2026, Masco Corp posted a 6% increase in consolidated net sales, driven primarily by a 9% gain in its Plumbing Products segment despite significant tariff-related cost inflation. The company executed strategic restructuring by integrating Liberty Hardware into Plumbing Products to optimize operations. While Decorative Architectural Products faced flat sales amid softer market demand, Masco's strong brand portfolio, exclusive retail relationships, and operational discipline support ongoing growth. Tariff uncertainties and consumer demand softness remain key risks to monitor alongside execution of cost-saving initiatives and capital allocation programs.

Q1 2026 Summary: Navigating Elevated Costs and Demand Dynamics

Masco Corporation’s first quarter ended March 31, 2026 showcased continued resilience amidst a challenging macroeconomic backdrop marked by tariff-induced cost inflation and subdued end-market demand. Consolidated net sales grew 6% year-over-year to $1.918 billion ([S2]), buoyed primarily by a robust performance in the Plumbing Products segment which expanded its top line by 9% to $1.364 billion despite heightened input costs from tariffs levied on imports principally sourced from China. Operating profit advanced 8% to $243 million in this segment, reflecting effective price recovery strategies coupled with ongoing productivity gains under the Masco Operating System.

Conversely, the Decorative Architectural Products segment saw flat net sales at approximately $554 million as market softness impacted repair and remodeling activity—its core demand driver. Nonetheless, this division achieved an 18% jump in operating profit to $104 million through aggressive cost containment and efficiency efforts ([S2]). These divergent dynamics underscore the segmented nature of Masco’s business exposure—Plumbing Products currently demonstrating more structural growth potential relative to the cyclical decorative segment.

The quarter also incorporated strategic realignment midstream as the Liberty Hardware business was formally integrated into the Plumbing Products segment ([S2], [S1]). This initiative targets operational synergies and streamlined reporting but complicates direct segment-to-segment comparisons with prior periods. Restructuring actions initiated late in 2025 continued into Q1 with related charges of approximately $8 million recognized, contributing toward an annual forecast of roughly $50 million in charges dedicated to optimizing headcount and consolidating manufacturing footprints ([S2], [S24]).

Tariff headwinds remain salient: costs linked to Chinese imports continue pressuring margins for plumbing components despite measured pricing actions. Importantly, Masco is tracking developments following a recent U.S. Supreme Court ruling concerning tariffs under the International Emergency Economic Powers Act—which may potentially yield refunds of prior payments. However, the timing and quantum of any such refunds are highly uncertain; Masco has not yet recognized amounts related to possible recoveries as of Q1 end ([S2], [S16]).

Company Strategy and Business Model: Leveraging an Industry-Leading Brand Portfolio

Masco operates through two primary segments—Plumbing Products and Decorative Architectural Products—that collectively encompass a broad range of branded building materials and home improvement solutions ([S1]). Its flagship brands include BEHR® paints (exclusive retail channel agreement with The Home Depot covering approximately 38% of consolidated net sales), DELTA® and HANSGROHE® faucets, LIBERTY® hardware, along with HOT SPRING® spas serving niche wellness markets.

The company’s business model centers on designing differentiated products that appeal across multiple channels including home center retailers like The Home Depot (a significant concentration risk), online retailers expanding internet market share, wholesalers, specialty stores, mass merchandisers and direct-to-consumer platforms. Innovation cycles focus on enhancing product utility while improving aesthetic appeal amid evolving consumer preferences.

Crucially, Masco’s reliance on residential repair and remodeling activity places it at the mercy of economic variables such as consumer confidence, mortgage rates impacting home equity accessibility, wage inflation trends affecting discretionary spend budgets, as well as the health of skilled tradespeople availability—all factors shaping near- to medium-term demand dynamics ([S1], [S21]).

Segment Overview: Realignment of Liberty Hardware into Plumbing Products

A material structural change implemented effective Q1 2026 was the internal reorganization realigning Liberty Hardware—a distributor providing cabinet hardware and shower door products—from Decorative Architectural Products into the Plumbing Products segment ([S2], [S24]). This integration aims to consolidate complementary plumbing-related offerings within a single reporting unit to enhance operational agility.

While this shift generates conversion noise in sequential reporting comparisons within each segment due to reclassification effects, strategically it facilitates supply chain optimization and cost synergies through tighter alignment of distribution channels and manufacturing processes under the Delta Faucet umbrella.

Competitive Environment and Market Positioning: Managing Customer Concentration and Private Label Pressures

Masco maintains a differentiated competitive position powered by established premium brands commanding loyal channel placements across North America and Europe ([S1], [S15]). However, its customer base exhibits pronounced concentration risk: The Home Depot accounts for about 38% of total net sales while Ferguson and Lowe’s individually contribute less than 10%. This dependence creates bargaining power asymmetries where major retailers can influence pricing structures or vendor selection protocols.

Additionally, private label products proliferate throughout e-commerce expansion corridors introducing margin pressure while increasing competitive intensity particularly against commoditized SKU offerings—a significant sectorwide trend ([S16]). Tariffs imposed chiefly on Chinese imports exacerbate supply chain complexities by inflating input costs unpredictably; mitigating these involves multifaceted sourcing strategies alongside negotiations aimed at preserving incremental price pass-through capabilities.

Growth Drivers: Innovation, Distribution Channels, and Operational Excellence

Masco’s growth engine relies heavily on its ability to innovate via product development that aligns with evolving consumer lifestyles—from smart kitchen fixtures to eco-conscious finishes—and extends utilitarian value-add through proprietary filtration systems or spa technologies ([S1]). Moreover, its expanding footprint within high-growth digital retail channels complements traditional brick-and-mortar sales by capturing shifting purchasing behaviors.

Operationally, Masco leverages the ‘‘Masco Operating System’’—a continuous improvement methodology driving systematic cost reduction while optimizing manufacturing throughput—critical under current inflationary environments ([S24], [S2]). Investments targeting automation enhancements continue alongside selective capacity expansions planned for later fiscal periods aimed at supporting volume scale.

Key Constraints: Tariffs, Commodity Inflation, and Consumer Confidence Risks

Elevated tariffs remain one of Masco’s most substantial cost headwinds particularly evident within plumbing components where import prices have spiked materially over baseline levels. Pricing adjustments implemented have only partially offset these pressures leaving residual margin erosion potential should commodity costs persist or escalate further ([S2], [S21]).

Likewise, employee-related inflationary pressures compound overall operating expenses necessitating efficiency offsets wherever possible without compromising service standards. Consumer demand stability is another risk vector; sustained weakness in housing renovation budgets stemming from erosion in consumer confidence or affordability constraints could depress shipment volumes significantly.

Capital Allocation and Shareholder Returns: Buybacks and Dividends Remain Priorities

Capital deployment reflects disciplined stewardship balancing reinvestment needs with shareholder remuneration. During Q1 2026 alone, Masco repurchased approximately 3.1 million shares for around $203 million—part of a broader authorization totaling up to $2 billion approved early in the year—and paid dividends totaling $65 million ([S11], [S8]).

This continuation underscores commitment toward maintaining shareholder value even as investment expenditures rise moderately; capital expenditures totaled about $34 million during Q1 primarily directed towards sustaining manufacturing capabilities ([S8], [S10]). The company’s balance sheet remains cautiously managed with liquidity enhanced through recently negotiated credit facilities amounting to $1 billion revolver plus a newly secured two-year delayed draw term loan capped at $500 million ([S4], [S5]).

Financial Snapshot: Revenue Growth Supported Despite Margin Pressure

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 810 | 1022 | 1248 | -1.5% |

| 2024 | 822 | 1075 | 1363 | -9.5% |

| 2023 | 908 | 1413 | 1348 | +7.6% |

| 2022 | 844 | 840 | 1297 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 261 | 571 | -437.8 |

| 2024 | 254 | 751 | -294.6 |

| 2023 | 257 | 353 | -720.6 |

| 2022 | 258 | 914 | -175.8 |

Source: SEC companyfacts cache [F1].

Cash & equivalents were reported at approximately $388 million as of March 31, 2026 ([F1]), supporting short-term obligations comfortably given current liabilities tallying roughly $1.653 billion nets out positive working capital dynamics (current ratio ~1.75).

Operating income for fiscal year ended December 31, 2025 totaled about $1.248 billion while net income was approximately $810 million ([F1]), setting a financial foundation for cautious optimism though noting modest margin compression trends attributable mainly to cost headwinds articulated above.

Investor Focus: Monitoring Tariff Refunds, Integration Milestones, and Market Demand Indicators

Looking ahead, key investor attention will pivot around developments linked to potential tariff refunds post-Supreme Court decision; any substantial recovery could provide unexpected earnings upside albeit timing remains opaque ([S2]). Likewise critical will be successful execution on integration milestones regarding Liberty Hardware consolidation into Plumbing Products—a process anticipated to unlock efficiencies over ensuing quarters per management guidance.

Furthermore, signs refuting further deterioration or signaling stabilization in consumer spending on home improvement projects would provide crucial validation points for sustaining growth trajectories amid macro uncertainty.

Lastly, closely watching cost-saving initiatives beyond restructuring charges will clarify if margin resilience can be preserved or enhanced against ongoing input price volatility.

Disclaimer: This analysis is for informational purposes only based exclusively on Masco Corporation's publicly filed SEC documents as of April 22, 2026 alongside related news disclosures. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments