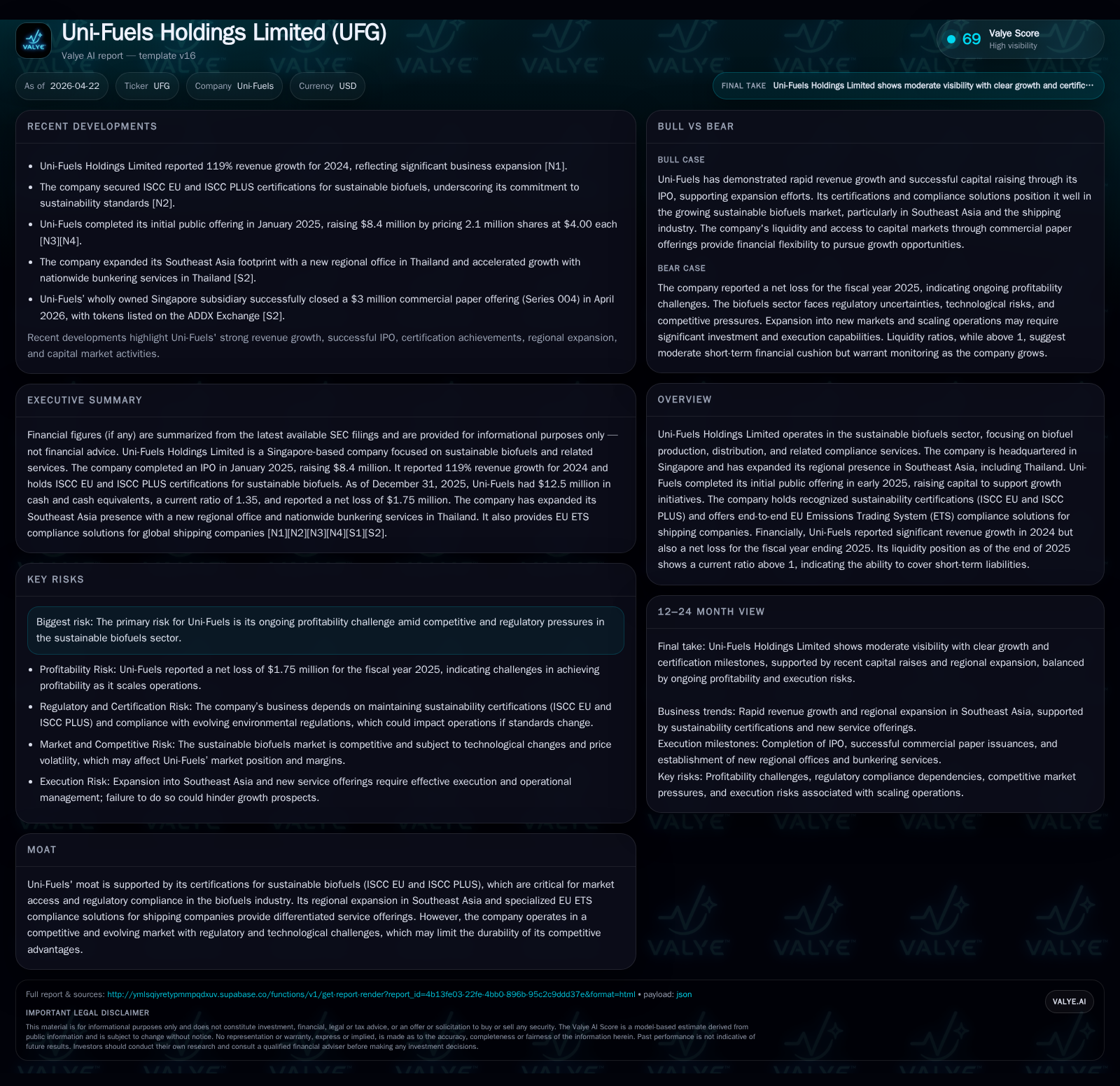

Uni-Fuels Holdings Advances Biofuel Growth with Novel Tokenized Funding Amid Margin Pressure

The company's recent $3 million tokenized commercial paper issuance exemplifies innovative liquidity management as it scales sustainable marine fuel volumes amid compressed margins.

Uni-Fuels Holdings closed its Series 004 tokenized commercial paper issue, raising $3 million to support its expanding operations in the Southeast Asian biofuels market. Despite strong revenue growth driven by higher marine fuel sales, gross margins compressed due to competitive pricing strategies aimed at capturing market share. The company’s ISCC EU and ISCC PLUS certifications and end-to-end EU ETS compliance services underpin its differentiated market position, especially in shipping fuel compliance. Challenges remain in operating profitability due to inflationary pressures and industry competition. Monitoring upcoming regulatory developments and execution on the new regional expansion in Thailand will be key.

Recent Quarterly Developments and Capital Raise

Uni-Fuels Holdings Limited announced the successful closing of its Series 004 commercial paper issuance on April 17, 2026, raising gross proceeds of US$3 million through tokenized debt instruments listed on the ADDX Exchange [S3]. This innovative financing approach underscores Uni-Fuels' adoption of blockchain-based capital market solutions to enhance liquidity access as it ramps up operations. The latest quarterly filing dated April 22, 2026 also presented updated financial results alongside strategic commentary [S2]. This fresh capital injection is pivotal for working capital management given the company's expansion plans and margin pressures.

Business Model and Sustainable Compliance Differentiation

Uni-Fuels operates primarily in the sustainable biofuels sector, producing and reselling biofuels tailored for maritime consumption, supplemented with related brokerage commissions [S1]. Central to its offering are ISCC EU and ISCC PLUS certifications, which are indispensable for regulatory compliance and market acceptance within the European Union's stringent carbon regulations . The company's revenue model blends physical fuel sales with value-added services that include end-to-end EU ETS compliance solutions designed for shipping firms seeking to meet increasing carbon allowance obligations [S8].

However, this business model faces unit economics challenges; Uni-Fuels has consciously sacrificed gross margin (from 2.3% in FY2023 down to approximately 2.1% in FY2024) to penetrate new markets aggressively through competitive pricing strategies aimed at accumulating volume [S1]. While this has fueled rapid revenue growth—marine fuel sales jumped from about $155 million in 2024 to $264 million by end-2025—the margin erosion reflects the trade-off inherent when prioritizing scale over immediate profitability.

Competitive Environment and Industry Dynamics in Southeast Asia Marine Biofuels

Within the Southeast Asian marine biofuels landscape, Uni-Fuels competes with both emerging local suppliers and established international fuel providers pivoting towards greener offerings . The sector remains fragmented with ongoing regulatory evolution impacting certification standards adherence, fueling complex barriers to entry and differentiation.

Pricing power appears constrained due to intensified competition, especially as more players chase the nascent but fast-growing sustainable shipping fuels segment. Additionally, supply chain complexities—ranging from feedstock sourcing to logistics—and the burden of maintaining costly sustainability certifications further compress margins [S1]. Regulatory uncertainty regarding maritime carbon regulations presents both risk and opportunity but contributes to demand volatility.

Growth Opportunities: Regional Expansion and EU ETS Compliance Services

Uni-Fuels’ strategic expansion into Thailand with establishment of a regional office coupled with nationwide bunkering capability marks a significant step towards strengthening its foothold across Southeast Asia [S9][S10]. Thailand’s strategic maritime location and rising environmental regulation adherence among shipping companies position it as a critical growth market.

The company also leverages its EU ETS compliance advisory services as a differentiation vector. By combining certified biofuel sales with emissions trading consultancy, Uni-Fuels aims to create customer stickiness by addressing adjacent regulatory compliance needs alongside traditional fuel delivery [S8]. As global emissions regulation intensifies within shipping lanes governed by EU mandates, this bundled service offering could build defensible niche positioning.

Challenges to Margins and Profitability in the Biofuels Sector

Despite top-line momentum, Uni-Fuels experienced a marked deterioration in profitability during FY2025. Operating income swung from a positive $214 thousand in FY2024 to a loss of approximately $1.58 million by year-end 2025 [F1][S1]. The net income mirrored this trajectory with a net loss of about $1.75 million. Factors contributing include gross margin compression due to competitive pricing tactics and escalating selling, general & administrative expenses which nearly doubled year-over-year.

Inflationary pressures—specifically increased personnel costs and overhead—exacerbate cost structures without fully matched revenue increases [S1]. The combination of relatively low gross margins (~2.1%) plus rising SG&A expenses (around 2.4% of sales) reflects industry-wide margin challenges where scale economies have yet to sufficiently materialize given early-stage expansion activities.

Forward-Looking Considerations: Milestones and Execution Risks

Key milestones ahead include further scaling physical supply chains across SEA markets while deepening ETS compliance service penetration—a domain sensitive to evolving maritime environmental frameworks implemented globally but spearheaded by regions like Europe [S8].

Adoption velocity of sustainable marine fuels remains tethered not only to regulations but also to shipping industry technology transitions towards greener engines or alternative fuel infrastructures—variables outside immediate control that pose execution risk.

Moreover, while recent tokenized commercial paper issuances ease liquidity concerns short term, further funding rounds may be required should operational cashflow remain negative amid investments or regulatory-induced cost spikes [S3][F1]. Monitoring customer onboarding rates vis-à-vis price elasticity will be crucial signals whether the current margin sacrifice translates sustainably into profitable scale or deeper losses.

Financial Health Overview: Profitability, Liquidity, and Capital Structure

Uni-Fuels’ financial profile evidences rapid revenue expansion tempered by stretched profitability metrics through end-2025. Revenue surged from approximately $155 million in FY2024 to nearly $264 million in FY2025 purely from marine fuel sales [F1][S1]. However, operating income declined significantly into negative territory (-$1.58 million), reflecting a sharp swing versus prior positive albeit modest profits ($214K) [F1]. The net loss widened correspondingly (-$1.75 million).

Liquidity conditions show current assets at roughly $39.1 million against current liabilities near $29 million yielding a moderate current ratio of about 1.35 — indicating reasonable short-term solvency though less buffer than desirable given scaling ambitions [F1]. Cash & equivalents stand around $12.5 million at fiscal year-end supported by successful recent tokenized debt issuances—the latest Series 004 raised $3 million listed on ADDX exchange [S3][F1].

Operating cash flows turned negative ($-2.33 million) while capital expenditures increased modestly ($36K), resulting in negative free cash flow circa ($-2.36 million) consistent with an investment-heavy growth phase [F1]. Equity expanded from approximately $4.54 million at end-2024 to over $10.5 million at end-2025 underscoring ongoing capital raises likely linked to IPO proceeds initially plus subsequent funding rounds including token sales [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($mm) | OpInc ($) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1750660 | -2 | -1578637 | 36159 | -1120.2% |

| 2024 | 171597 | 0 | 214642 | 9020 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -16.7 |

| 2024 | 0 | 3.8 |

Source: SEC companyfacts cache [F1].

In summary, Uni-Fuels is navigating an early-stage growth trajectory characterized by scaling volumes undercutting immediate margins requiring innovative liquidity instruments such as blockchain-enabled commercial paper issuance for operational funding [S3][S4][S5]. Improvement hinges on managing margin compression amidst competitive pressures balanced against continued regional expansion success.

Disclaimer: This analysis is solely for informational purposes reflecting publicly available statements and SEC filings as of April 22, 2026, without any investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments