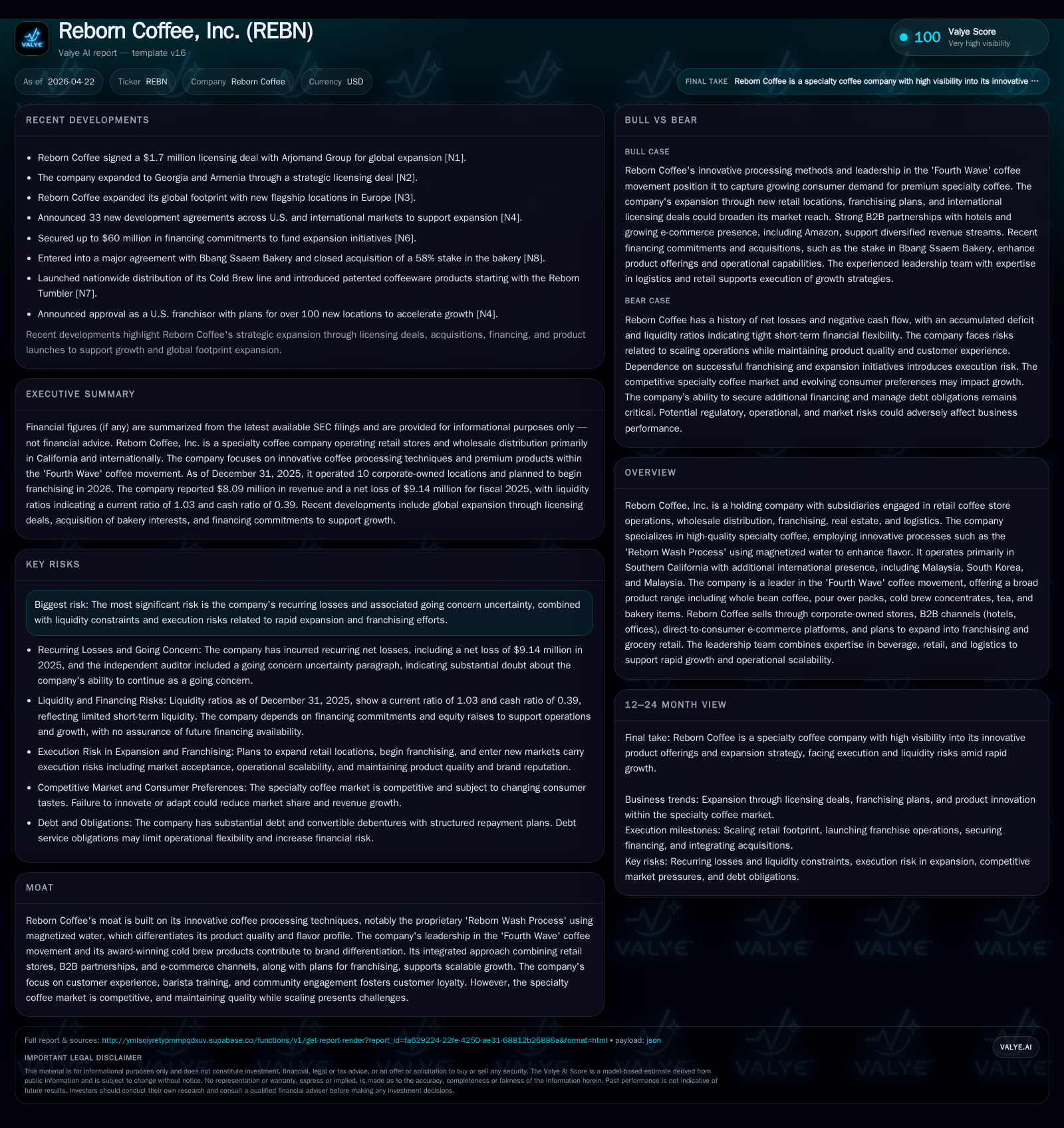

Reborn Coffee’s Forbearance Deal Unfolds: Assessing Growth Prospects Amid Financial Strain

The April 2026 forbearance agreement addresses immediate liquidity constraints, enabling Reborn Coffee to pursue growth initiatives within the competitive specialty coffee sector.

Reborn Coffee, Inc. secured a crucial amended forbearance agreement in April 2026 with its convertible debenture holders, establishing a structured repayment plan through September 2026 that mitigates near-term default risk and stabilizes liquidity. The company operates a vertically integrated specialty coffee platform spanning retail stores, wholesale, e-commerce, and emerging franchising channels. Its proprietary ‘Reborn Wash Process’ and participation in the Fourth Wave coffee movement underpin brand differentiation despite ongoing market competition and evolving consumer preferences. However, persistent operating losses, negative cash flows, and capital structure stress pose execution risks as the firm seeks to expand its footprint in California and select international markets. Key catalysts include the launch of franchise locations and continued B2B channel development.

April 2026 Forbearance Agreement: Stabilizing Near-Term Liquidity

The cornerstone recent development anchoring Reborn Coffee’s current operating landscape is the April 15, 2026 amendment and restatement of its Forbearance Agreement with Arena Investors, secured through a Form 8-K filing dated April 21, 2026 [S3]. This agreement structures repayment obligations tied to convertible debentures held by Arena Investors through September 30, 2026, effectively alleviating immediate default risk that otherwise cast substantial doubt on solvency earlier [S5]. By postponing potential acceleration events and providing defined repayment terms, this arrangement buys critical runway for Reborn to operationally stabilize and pursue growth avenues.

This near-term resolution contrasts against prior uncertainty regarding liquidity pressures stemming from recurring losses and strained cash flows. The amendment underscores how external creditor negotiations have become pivotal for Reborn given its limited internal cash generation capacity. It also sets a definable milestone when refinancing or additional capital injections will be required to maintain positive traction.

Reborn Coffee’s Integrated Specialty Model: Innovation Meets Market Reach

Reborn Coffee operates as a diversified holding company encompassing subsidiaries active across several domains integral to specialty coffee delivery [S1][S19][S20][S28]. At its core is Reborn Global Holdings managing retail store operations predominantly in Southern California—a mature specialty coffee market yet conducive due to store locations often replacing exodus sites of larger national peers [S17]. Complementing retail is wholesale distribution servicing hotels and office clients with products such as pour-over packs and cold brew concentrates that extend brand reach beyond storefronts.

Furthermore, the recently established Reborn Logistics entity provides in-house supply chain capabilities supporting material flow efficiency critical to scaling operations [S1]. Internationally, nascent operations span Malaysia and South Korea via wholly or majority-owned subsidiaries adding geographic diversity albeit at an embryonic scale [S1].

A distinctive pillar of the firm’s product relevance is its proprietary "Reborn Wash Process", leveraging magnetized water treatment during coffee bean processing—a technical innovation intended to enhance flavor profiles setting it apart from commodity or typical specialty offerings . This aligns with the company's alignment with the "Fourth Wave" coffee movement emphasizing artisanal production methods combined with sustainable sourcing practices.

Revenue generation funnels through multiple channels: corporate-operated stores building direct customer engagement; burgeoning e-commerce platforms targeting direct-to-consumer sales; B2B partnerships providing bulk order opportunities including corporate gifting; and an anticipated franchising program aimed at replicating retail experience rapidly starting in 2026 [S19][S20]. Alongside beverages, expansion into tea selections and bakery products at retail outlets increases dwell time and basket size.

The leadership team synergizes expertise across beverage innovation and retail management domains—a critical factor given operational complexity inherent in managing multifaceted sale channels while preserving premium quality standards [S19].

Competitive Differentiators Within the Fourth Wave Coffee Movement

Reborn is firmly positioned within the Fourth Wave specialty coffee sphere—a niche yet growing segment distinguished by consumers valuing traceability, sustainability, quality transparency, and experiential consumption [S26]. Its award-winning cold brew products exemplify success translating technical innovation into recognized consumer value.

Magnetized water processing is unusual within industry norms—this scientific approach appeals particularly to aficionados seeking taste nuances absent from mass-market blends. Such differentiation supports premium pricing justification but also requires continuous consumer education efforts executed via social media campaigns (Instagram giveaways), local community engagement (pop-up events at Facebook campus), and curated experiential offerings such as latte art competitions [S19].

Nonetheless, competitive intensity remains sharp with entrenched players possessing deeper capital reserves capable of aggressive marketing or price competition [S26]. Thus while the moat created by innovation and brand experience is meaningful it is not impermeable.

Industry Dynamics: Supply Chain, Customer Preferences, and Scaling Pressures

The specialty coffee industry continues evolving amid shifting consumer preferences prioritizing convenience but also authenticity. Scaling roasting capacity has been a logistical focus for Reborn as it seeks to meet increased wholesale demand without compromising artisanal quality [S7]. Investments into eco-friendly packaging align with sustainability imperatives increasingly demanded by elevating customer cohorts.

Operational challenges include synchronizing rapid retail expansion with training barista talent capable of consistently delivering complex brewing techniques—a core competency underpinning customer loyalty but costly to institutionalize [S19]. Also noteworthy is balancing premium pricing power against elasticity where price hikes risk alienating more price-sensitive segments especially amid broader economic pressures highlighted by ongoing negative cash flows [S6].

Growth Drivers: Franchising, B2B Channels, and Product Extensions

Looking ahead, franchising stands as a primary driver of growth volume expansion beyond Southern California's footprint. The company formed Reborn Coffee Franchise LLC with plans underway for systematic rollouts beginning in 2026 though no franchisees were onboard as of year-end 2025 [S1][S18][S28]. This channel promises scalability of brand presence while leveraging capital-light investment from franchisees but carries execution complexity including regulatory compliance across various U.S. jurisdictions [S27].

B2B relationships bolster revenue stability through contracts with hotels—offering pre-packaged pour over packets or cold brew concentrates—and corporate gifting programs notably expanding around winter holiday periods [S7][S20]. Penetration into grocery markets with both bulk roasted beans and kiosk-based fresh brews represents another vector anticipated to enhance accessibility.

On product innovation frontiers, expansions into tea varieties complement baked goods available onsite aiming at increasing average customer spend per visit while diversifying revenue sources beyond caffeine-focused drinks [S17].

Challenges Ahead: Recurring Losses, Execution Risks, and Market Competition

Despite top-line momentum—36.5% revenue growth in fiscal year 2025—the company incurred significantly increasing operating losses approaching $5.8 million accompanied by deepening net losses nearing $9.1 million [F1][S1]. Operating cash flow remains deeply negative ($6.5 million deficit), signaling persistent burn requiring recurring capital infusions [F1]. Capital expenditures sharply reduced (down over 95% YoY) potentially reflective of cash preservation tactics rather than sustained asset investment.

Debt burden remains substantial with reports citing accelerated service requirements limiting free cash flow availability for growth investments or unexpected contingencies [S4][S5]. Reliance on equity financing instruments such as an Equity Line of Credit Agreement (ELOC) provides flexible funding but adds future dilution risks tied to share issuances contingent on stock price performance [S21].

Execution risks include maintaining premium coffee quality amidst rapid geographic expansion especially via inexperienced franchise partners; navigating complex regulatory environments affecting franchise operations; potential shifts in consumer spending reducing discretionary beverage purchases; plus competition intensifying from well-capitalized incumbents or new entrants replicating aspects of Reborn’s model [S26].

Upcoming Catalysts and Milestones to Track

Key near-term monitoring points revolve around the expiry date of the Amended Forbearance Agreement on September 30, 2026—success here hinges on either refinancing or conversion of debt obligations sustaining operational runway [S3][S5]. Launch timing for first franchise openings in late 2026 will test scalability assumptions.

International expansion progress particularly in South Korea and Malaysia may validate cross-border adaptability but remains nascent at present [S1]. The initiation of a dedicated training school program aimed at cultivating skilled baristas and franchise operators presents a longer-term enabler for consistent quality standards [S19]. Finally, tracking incremental improvements toward operating profitability alongside revenue gains will serve as a bellwether signifying effective balance of growth versus cost control initiatives.

Financial Review: Revenue Growth Against Persistent Operating Deficits

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8 | -9 | -7 | -6 | +36.5% | -90.2% |

| 2024 | 6 | -5 | -3 | -5 | -0.4% | -20.2% |

| 2023 | 6 | -4 | -3 | -4 | +83.7% | -12.5% |

| 2022 | 3 | -4 | -3 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | |

| 2024 | -5 | -184.6 |

| 2023 | -4 | -254.0 |

| 2022 | -4 | -82.9 |

Source: SEC companyfacts cache [F1].

Revenue grew strongly by approximately 36.5% year-over-year from fiscal 2024 to fiscal 2025—a positive signal regarding market acceptance—but this was outpaced by worsening profitability metrics including operating income decline by over 25% year-over-year alongside doubling net loss severity reflecting elevated expenses related likely to expansion activities combined with fixed cost absorption challenges.

Operating cash flows deteriorated nearly twofold illustrating acute working capital demands compounded by limited capex investments indicating cautious capital deployment amid tightening liquidity conditions.

Equity stands relatively modest (~$2.6 million by end-2024), positioning financial leverage risks prominently especially as debt maturities via convertible debentures loom requiring vigilant management attention to ensure sustainable capital structure adjustments [F1][S4][S5]. The forbearance deal partly mitigates these immediate concerns but only until Q3 2026 expiration underscoring ongoing funding dependency.

This analysis synthesizes recent SEC disclosures alongside financial data headers reflecting Reborn Coffee’s operational complexities positioned between innovative specialty coffee ambitions confronting tangible financial constraints amid intensifying competition within a dynamic consumer marketplace.

Disclaimer: This document is for informational purposes only and does not constitute investment advice or recommendations regarding securities of Reborn Coffee Inc., or any other entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments