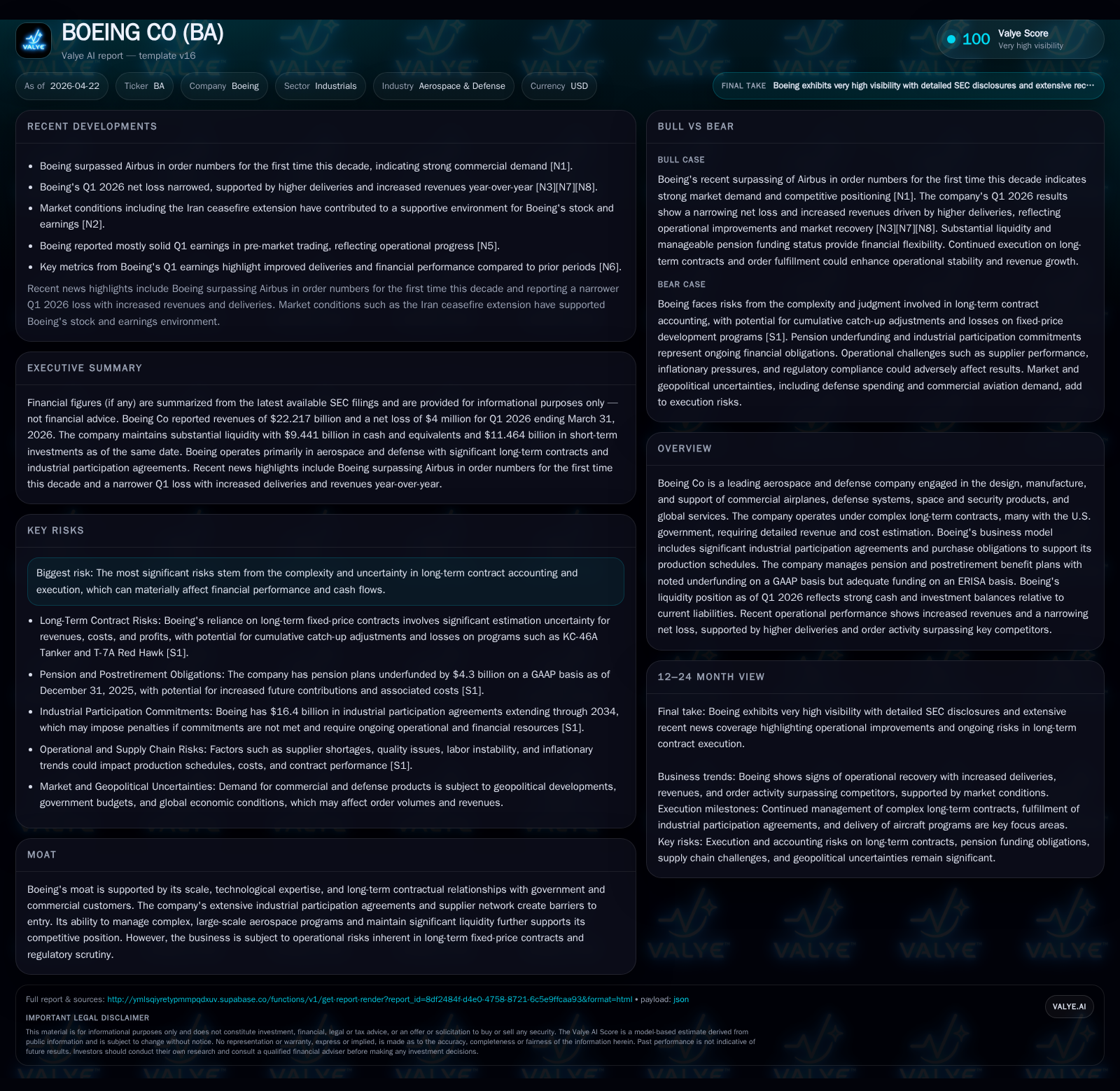

Industrial Strength and Contract Complexity Drive Boeing’s Recovery

Boeing’s Q1 2026 results showcase robust revenue growth, tightening losses, and increased deliveries amidst intricate contract dynamics supporting its aerospace leadership.

In Q1 2026, Boeing reported significant sequential momentum with revenues increasing notably and net losses narrowing, driven by a higher delivery cadence in commercial airplanes and steady defense contracts. The company operates within a complex business model reliant on large-scale aerospace programs, long-term fixed-price government contracts, and extensive industrial participation commitments, which together create considerable barriers but also impose execution risks. Boeing’s scale, technological depth, and entrenched customer relationships underpin a competitive moat amid recovering global aerospace demand. Key growth factors include backlog expansion and balanced segment contributions, while operational risks from program accounting and regulatory scrutiny remain critical. Financially, Boeing is improving profitably with positive operating income in 2025 following multi-year losses and maintains solid liquidity to support ongoing execution.

Recent Quarterly Operating Update: Signs of Recovery and Scaling Delivery

Boeing’s Q1 2026 results released in the April 22 filing [S2] reveal notable operational progress manifesting in increased revenues alongside a narrowing net loss compared to prior periods [N11][N14]. Revenues surged as the company accelerated delivery volumes particularly in its commercial airplanes division—capitalizing on easing pandemic-related disruptions and aligning with improved global airline demand [N3]. This upscaled production rhythm helped reduce fixed overhead absorption costs amplifying operating margins incrementally from recent years’ losses toward profitability.

While the quarter still reflected a net loss, it was significantly narrower than consensus estimates confirming better cost management and contract execution efficiency. Defense & space segments maintained steady performance owing to long-term government contracts cushioning against commercial cyclicality [S2][S3]. Importantly, order intake during this quarter outpaced key peers signaling sustained demand strength that supports Boeing’s multi-year production schedules.

Underpinning Business Model: Aerospace Programs and Complex Contracts

Boeing operates on a capital-intensive model centered around designing, manufacturing, and servicing large aerospace platforms requiring vast multi-year investments anchored in long-term customer engagements including substantial U.S. government defense contracts [S1]. Critical to its business is program accounting where revenues and costs are estimated progressively over contract lifecycles often covering up to several years or even decades.

This model involves significant purchase obligations tied to raw materials procurement and supplier ecosystem management constrained by stringent production planning horizons necessitating early commitment [S1]. Moreover, Boeing manages numerous industrial participation agreements representing economic flow-back or technology transfer mandates totaling $16.4 billion through 2034 that embed the company deeply into global supply chains [S1]. Though no penalties were incurred in 2025 from these commitments, failure to meet them could invoke consequences underscoring added operational complexity.

Competitive Moat: Scale, Contractual Network, and Regulatory Navigation

Boeing's competitive strengths are largely rooted in its unmatched scale as one of the largest producers of commercial aircraft worldwide alongside sophisticated defense systems [S1][F1]. The company's technological expertise—the result of decades-long R&D enmeshed with industrial participation agreements—creates high switching costs for customers especially governments who rely on complex integrations tailored over years.

Long-term contractual relationships with the U.S. government provide stability but require adept navigation of regulatory oversight which continues to increase post previous certification challenges [N3]. Boeing's liquidity position—with nearly $9.44 billion in cash equivalents at March-end—further cushions against industry cyclicality and program execution volatility [F1][S2]. Its comprehensive supplier network managed under long-term contracts further fortifies barriers against new entrants.

Industry Dynamics: Global Aerospace Demand, Supply Chains, and Pricing

The broader aerospace sector is experiencing recovering demand after pandemic-induced downturns spurred fleet modernizations globally [S1][N3]. Airlines’ increasing utilization rates along with geopolitical defense spending contribute to improving order books; however, inflationary pressures persist influencing raw material costs which constrain pricing upside.

Supply chain resilience remains challenged due to semiconductor shortages and materials bottlenecks affecting delivery cadence across key platforms [S1]. In this context, Boeing’s ability to synchronize supply chain logistics through its industrial commitments becomes a notable differentiator but also a potential risk point demanding tight orchestration.

Growth Enablers: Backlog Expansion and Commercial-Defense Balance

Boeing's backlog expanded as new orders outpaced deliveries underpinning forward revenue visibility [S2][F1]. The interdependence between the commercial airplane segment's ramp-up—where higher delivery numbers translate directly into near-term revenue growth—and steady defense contracts providing margin resilience creates a balanced portfolio supporting financial recovery.

Internal cross-border industrial participation arrangements help deepen penetration into foreign markets where offsets facilitate sales wins illustrating Boeing's strategic approach towards sustaining global reach despite competitive headwinds [S1][N3]. This strategy enhances customer stickiness by embedding Boeing’s supply chains within purchasers' local economies.

Growth Constraints: Execution Risks and Contractual Accounting Volatility

Despite positive developments, Boeing faces meaningful constraints linked to execution uncertainties intrinsic to large fixed-price contracts requiring precise forecasting of costs over extended cycles [S5][S1]. Poor estimation can lead to margin erosion or contract losses impacting earnings unpredictably.

Pension plan underfunding at $4.3 billion on GAAP basis—though more than 90% funded under ERISA guidelines—and the possibility of future regulatory or compliance penalties add layers of financial risk [S1][S5]. While past experience shows prudent management avoiding penalties on industrial participation agreements so far, this remains latent risk worth monitoring closely.

Regulatory scrutiny intensified following prior certification issues necessitates ongoing mitigation efforts which may delay program timelines or increase compliance expenditures affecting operating cadence.

Key Milestones Ahead: Delivery Targets, Program Execution, and Order Flows

Key near-term milestones include tracking quarterly delivery numbers against planned targets since these are critical drivers of revenue recognition under program accounting frameworks [S2][N11]. Monitoring incoming order flows will also provide leading signals about market health particularly in commercial aviation segments.

Capital deployment plans disclosed via recent filings indicate continued cautious share repurchase activity primarily involving restricted stock unit-related transactions rather than open market buybacks for now [S2][S4], reflecting balanced priorities between liquidity preservation versus shareholder returns in this recovery phase.

Additionally, any announced changes in pension funding policies or major regulatory developments could materially influence capital planning and risk profile going forward.

Supporting Financial Analysis: Performance Trends and Cash Flow Dynamics

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 89.5 | 2.2 | 1.1 | 4.3 | +34.5% | +118.9% |

| 2024 | 66.5 | -11.8 | -12.1 | -10.7 | -14.5% | -431.8% |

| 2023 | 77.8 | -2.2 | 6.0 | -0.8 | +16.8% | +55.0% |

| 2022 | 66.6 | -4.9 | 3.5 | -3.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($bn) | ROE% |

|---|---|---|

| 2025 | -1.9 | 41.0 |

| 2024 | -14.3 | 302.4 |

| 2023 | 4.4 | 12.9 |

| 2022 | 2.3 | 31.1 |

Source: SEC companyfacts cache [F1].

Boeing has demonstrated a material turnaround moving from substantial operating losses in FY 2024 to positive operating income of $4.28 billion in FY 2025 representing a year-over-year improvement exceeding +140% [F1]. Revenue growth of +34.5% YoY underscores effective scaling of delivery volumes particularly post-pandemic rebound phases while net income swung from deep red to modest profit.

Operating cash flow remains positive though free cash flow reflects continued investment demands tied to capex spending rising nearly +32% YoY due to modernization initiatives supporting future programs [F1]. Liquidity measured by cash & equivalents stands robust at $9.44 billion as of March-end 2026 helping ensure operational flexibility within an environment marked by complex contract fulfillment requirements [F1][S2].

This analysis synthesizes Boeing's latest SEC disclosures alongside relevant market data underscoring how operational recovery dovetails with strategic scale advantages inherent in its aerospace business model but tempered by the intricacies of long-duration contracts requiring vigilant execution oversight.

This report is for informational purposes only; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments