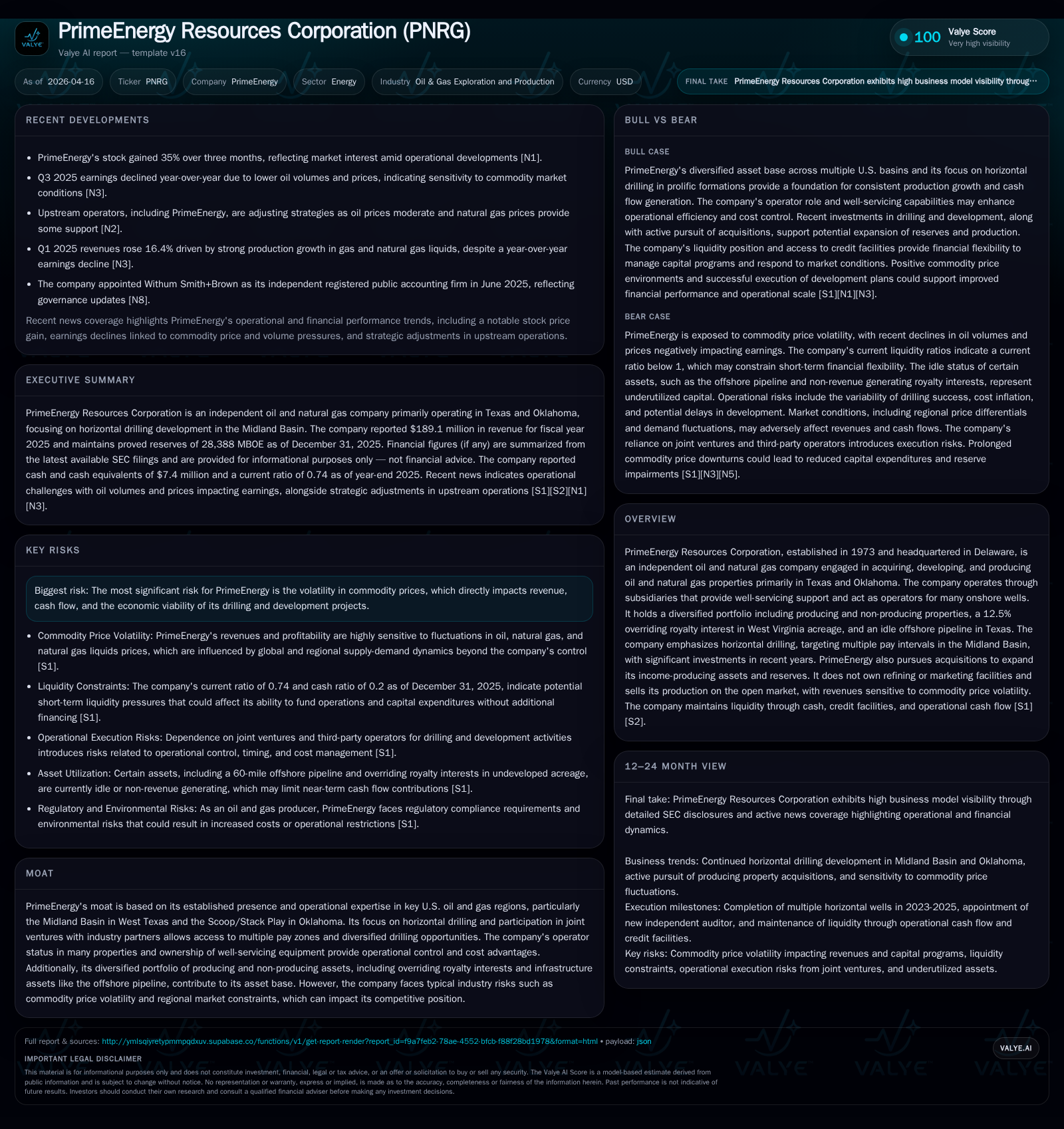

PrimeEnergy Resources Corp’s Revenue Retreat and Strategic Resilience in 2025

Declining revenues in 2025 contrast with expanded margins and disciplined capital management amid commodity price volatility.

PrimeEnergy Resources Corp experienced a significant revenue decline of about 20.5% in 2025 but demonstrated remarkable operational leverage, with operating income and net income surging over 1100% and 2200% respectively relative to prior years. The company’s focus on horizontal drilling in the Midland Basin and Oklahoma, combined with asset diversification—including non-producing royalties and idle infrastructure—underpins its strategy against volatile commodity prices. Robust liquidity maintained through an expanded borrowing base, coupled with prudent buybacks and continued capex commitment, reflect its financial resilience. However, commodity price fluctuations remain a key risk factor influencing future growth and operational flexibility.

Historical Growth Performance and Profitability Surges

PrimeEnergy Resources Corp faced meaningful top-line contraction in fiscal year (FY) 2025 with total revenue declining approximately 20.5% to $189 million from nearly $238 million in FY2024 [F1]. This downturn correlates closely with weakening oil prices—a key revenue driver—where WTI averaged $65.34 per barrel in 2025 versus $75.48 previously [S1]. Despite this decline in sales volume or price realization, PrimeEnergy achieved substantial earnings quality improvement: operating income surged over eleven-fold compared to prior comparable periods (historical peak operating income was about $59.7 million as of FY2022) [F1]. Net income followed suit, posting an unprecedented leap of roughly 22 times from the comparative year data available up to FY2022 [F1]. These gains underscore significant margin expansion enabled by enhanced cost controls and operational efficiencies.

Operating cash flow (CFO) remained robust at about $96.7 million in the latest year, a moderate decrease from $115.9 million the year before but still providing substantial free cash flow overall after capital expenditures [F1]. These figures suggest that PrimeEnergy effectively navigated revenue pressures by optimizing its cost base and prioritizing financially accretive projects.

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | Rev YoY |

|---|---|---|---|

| 2025 | 189 | 97 | -20.5% |

| 2024 | 238 | 116 | +79.0% |

| 2023 | 133 | 109 | +6.2% |

| 2022 | 125 | 33 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) |

|---|---|

| 2025 | 14 |

| 2024 | 13 |

| 2023 | 8 |

| 2022 | 7 |

Source: SEC companyfacts cache [F1].

Note: Operating income and net income exact values for FY2024 and FY2025 are not detailed in [F1]; YoY percentages calculated using available prior year data.

Operational Backbone: Horizontal Drilling and Midland Basin Focus

PrimeEnergy’s operational resilience hinges on its technical expertise in horizontal drilling, primarily within the Midland Basin of West Texas and the Scoop/Stack plays across Oklahoma [S1]. By targeting multiple pay intervals with horizontal wells, the company enhances reservoir contact area significantly compared to vertical wells, enabling better stimulation and higher initial production (IP) rates per well with a reduced surface footprint—key in managing operational costs and environmental impact.

Their precise application of horizontal drilling stimulation techniques permits tapping into stacked formations efficiently, allowing for flexibility in addressing reservoirs yielding either high early cash flows or those offering longer-term value with steadier returns on invested capital [S1]. These methods align with industry trends favoring multi-zone completions that optimize EURs (Estimated Ultimate Recoveries) while mitigating capital intensity per production barrel.

Additionally, PrimeEnergy functions as operator for many of its wells through subsidiaries, granting enhanced cost control capabilities and operational oversight [S1]. Ownership of well-servicing equipment further reduces outsourced dependency costs, contributing to notable margin improvement visible in recent financial results.

Commodity Price Volatility: Impact and Mitigants

The company remains distinctly sensitive to commodity price fluctuations—particularly WTI crude oil and Henry Hub natural gas prices—as delineated in its risk disclosures [S1]. Oil prices softened from an average $75.48 per barrel in 2024 to $65.34 in 2025, while natural gas prices increased from $2.13 to $3.39 per MMBtu over the same period [S1]. This dual-direction pricing influenced revenue contraction but offered some offset via gas sales.

Broader market volatility drivers include geopolitical tensions, OPEC production decisions, weather disasters affecting supply chain logistics, regulatory changes including methane emissions standards enforced by EPA, and shifts in domestic versus foreign supply-demand balances [S1]. PrimeEnergy currently avoids derivative hedging instruments except where mandated by bank covenants, thus maintaining full exposure to price swings but preserving upside potential when markets improve [S23].

The company’s ability to adjust its capital program responsively is a key mitigant; the capital budget for 2025 was scaled based on expected cash flow availability, with flexibility to divest non-core assets or adjust drilling plans if prices remain pressured [S18]. This agility is crucial given the unpredictable nature of energy markets.

Future Growth Outlook: Asset Development and Acquisition Strategy

PrimeEnergy emphasizes expansion of high-return horizontal drilling campaigns in Midland Basin acreage (~17,138 gross acres predominantly located in Reagan, Upton, Martin, and Midland counties), with potential to support approximately 100 additional horizontal wells contemplating current technological approaches [S23]. Concurrently, it develops reserves within Oklahoma counties including Canadian, Grady, Kingfisher, Garfield, Major, and Garvin, where it holds about 4,021 net acres under active development [S23].

Apart from producing properties, PrimeEnergy maintains a non-revenue generating overriding royalty interest covering roughly 30,000 acres in West Virginia; this asset offers long-term optionality pending commencement of development activities [S1]. It also owns an idle offshore pipeline infrastructure off Texas coast whose commercial deployment could provide midstream integration advantages if activated.

Strategic acquisitions form part of the growth palette as well; the company pursues joint ventures to acquire producing properties enhancing income stability while balancing exploration and development risk [S1]. Decisions incorporate tradeoffs between wells delivering high initial production rates favorable for near-term cash flow versus lower-rated reservoirs projecting higher lifetime ROI.

Capital Structure Evolution and Liquidity Cushion

Capital structure management underscores PrimeEnergy’s strategic resilience amid fluctuating commodity environments. It operates under a revolving credit facility initially sized at $75 million but incrementally increased semi-annually due to improving financial metrics tied to asset valuations—reaching a borrowing base of $115 million by mid-2024 with extended maturity to 2028 [S4], [S9], [S20].

As of late 2025 reports, borrowings were minimal relative to total availability at approximately $20 million drawn against a $115 million limit, reflecting conservative leverage usage and strong liquidity maintenance [S6], [S9]. The facility is secured against substantially all oil and gas properties with covenants requiring adherence to minimum liquidity ratios and capped indebtedness relative to EBITDAX.

Cash & equivalents stood at roughly $7.4 million at the end of FY2025, supplemented by current assets totaling $27.7 million albeit offset by current liabilities around $37.4 million resulting in a sub-1 current ratio of ~0.74 indicating working capital pressure but manageable given revolving credit accessibility [F1].

Management actively monitors borrowing base redeterminations coinciding with half-year financial updates maintaining flexibility for capital spending aligned with cash flow projections.

Returns Enhancement: Share Repurchases and Capital Allocation

PrimeEnergy has consistently returned capital through share buybacks amounting to approximately $13.55 million in FY2025—a figure closely tracking levels from prior periods ($13.43 million in FY2024) even amid revenue softness highlighting disciplined capital deployment backed by positive net income generation [F1]. The company targets sustaining ROE around 22.6%, underscoring efficient equity utilization despite cyclical headwinds.

Free cash flow (operating cash flow less estimated capex) remained positive at roughly $20.8 million suggesting capacity for both reinvestment into drilling programs and shareholder returns without excessive reliance on external funding sources [F1]. Dividend payments remain subject to credit agreement restrictions but are calibrated conservatively consistent with liquidity preservation priorities.

Capital expenditures focus remains on horizontal well developments prioritized by economic returns with exploration budgets adjusted dynamically per commodity outlooks and internal cash availability metrics [S18].

Key Risks: Market Dynamics and Regulatory Environment

Key risks prominently feature commodity price volatility exacerbated by unpredictable global supply-demand imbalances impacting profitability directly [S10], [S11]. Regulatory risks are material as evolving EPA methane emissions standards (NSPS Subparts OOOOb/OOOc), potential expansions of Clean Water Act jurisdiction under Supreme Court rulings, and heightened climate change legislation may impose incremental operational costs or delay permitting processes thereby hindering development cadence or inflating capital intensity [S11], [S13], [S14], [S25], [S26].

Environmental liabilities from historic operations pose contingent exposures though insurance coverage mitigates some risk — notably absence of business interruption insurance tempers full coverage against operational disruptions [S26]. Additionally, reputational risk associated with fossil fuel investments could influence financing access over time as ESG investment paradigms evolve.

Operational hazards inherent in well servicing and production further temper upside but are deemed manageable within current risk management frameworks.

Forward-Looking Indicators to Watch

Absent explicit forecasts from PrimeEnergy beyond general guidance on capital programs calibrated to commodity prices and liquidity status [S18], market participants should monitor:

- WTI crude oil pricing trends juxtaposed against Henry Hub natural gas movements as primary drivers influencing realized revenues.

- Mid-year borrowing base redetermination outcomes reflecting lender asset valuations signaling potential debt capacity adjustments.

- Exploration success rates including IP data from new horizontal wells influencing reserve replacement metrics.

- Quarterly operating results outlining margin trajectory amid input cost inflation or efficiencies gains.

- Disclosures on regulatory developments affecting permitting cycles or compliance costs relevant for US operations.

- Cash flow generation consistency underpinning ongoing buyback programs and capex funding abilities.

- Developments related to activating non-producing royalty interests or redeploying idle infrastructure like the offshore pipeline for diversification or midstream synergies.

Maintaining vigilance over these indicators will be critical for assessing PrimeEnergy’s continued navigation through cyclical pressures while leveraging operational strengths embedded in its portfolio strategy.

This analysis is based solely on information contained in publicly filed documents as of April 16, 2026 ([F1], [S1]–[S29]) without speculative assumptions or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments