Travelers Companies Expands Profitability Within a Challenging Insurance Environment

Examining how Travelers leverages underwriting expertise, disciplined capital allocation, and risk management to sustain growth amid industry pressures.

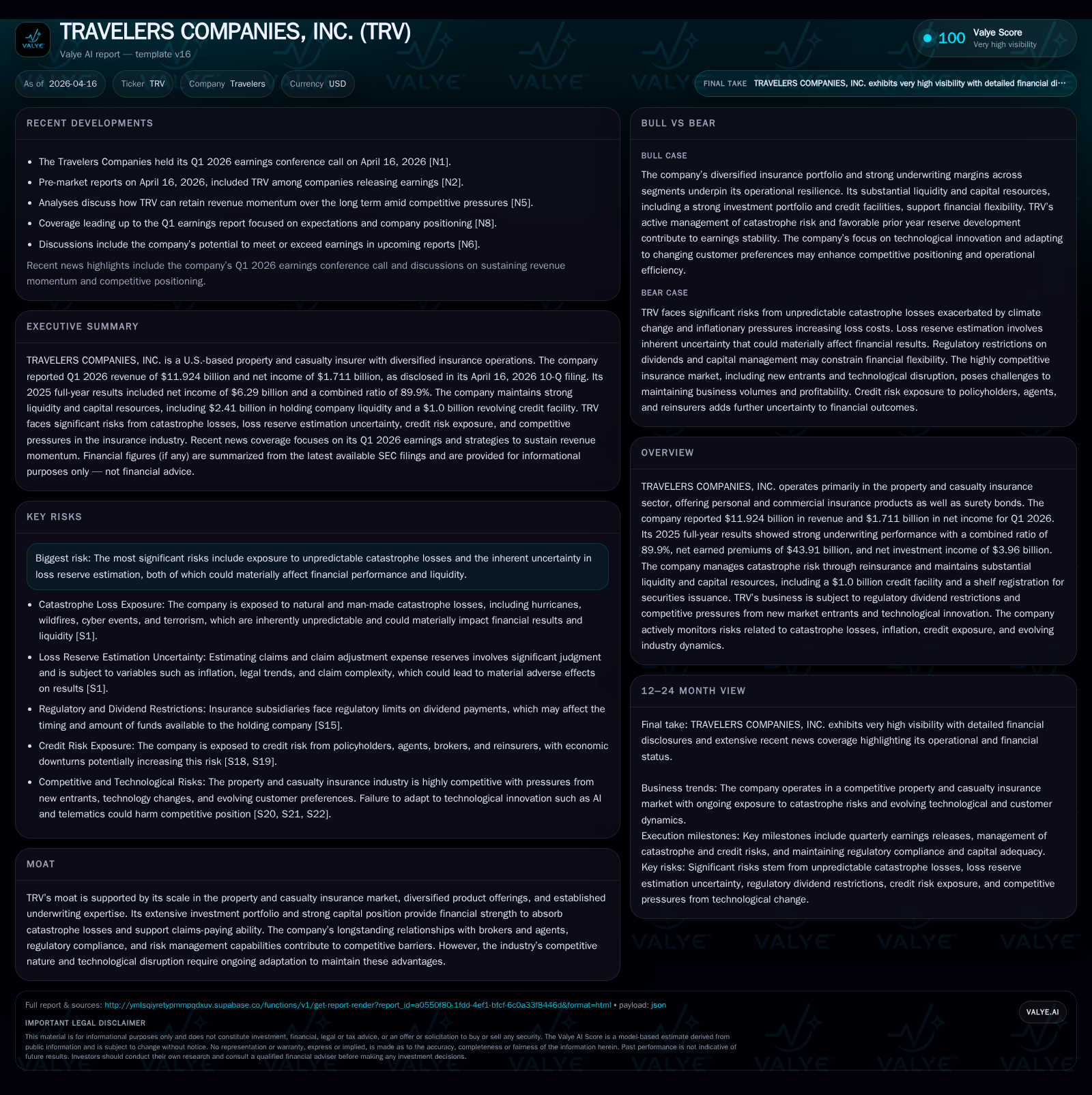

Travelers Companies, Inc. reported robust full-year 2025 results with revenue nearing $49 billion and net income growth of nearly 26% year-over-year, driven by a diversified premium base across personal and commercial property and casualty lines. Its underwriting discipline yielded a strong combined ratio of 89.9%, supported by rigorous catastrophe risk management through advanced modeling and reinsurance arrangements. The company maintains substantial liquidity and an active capital return program while navigating competitive pressures from new market entrants and regulatory constraints. Future growth will hinge on premium pricing trends, climate-related risk volatility, and technological adaptation within the evolving insurance landscape.

Steady Revenue Expansion Backed by Diversified Premium Growth

Travelers Companies has demonstrated consistent revenue growth over the past four fiscal years, culminating in reported revenues of approximately $48.8 billion for FY2025, up 5.2% from $46.4 billion in FY2024 [F1]. This top-line progression was underpinned by the company's diversified portfolio spanning personal lines (auto, home) and commercial lines (property, casualty), which cushions earnings against sector-specific volatilities [N10][N5]. The breadth of Travelers' product offerings provides resilience as it mitigates concentration risk inherent in any single segment.

The company's multi-channel distribution strategy leveraging long-established agent and broker relationships continues to deliver stable premium flows despite heightened competition from newer entrants employing digital-first models [N5][S20]. Technology facilitates enhanced underwriting capabilities but also accelerates market dynamics toward more price-sensitive consumer segments.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 48.8 | 6.3 | 10.6 | +5.2% | +25.8% |

| 2024 | 46.4 | 5.0 | 9.1 | +12.2% | +67.1% |

| 2023 | 41.4 | 3.0 | 7.7 | +12.1% | +5.2% |

| 2022 | 36.9 | 2.8 | 6.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 979 | 3.0 | 19.1 |

| 2024 | 951 | 1.0 | 17.9 |

| 2023 | 908 | 1.0 | 12.0 |

| 2022 | 875 | 2.0 | 13.2 |

Source: SEC companyfacts cache [F1].

Note: Figures sourced from [F1] reflect operational profitability improvements coincident with revenue acceleration through premium diversification.

Underwriting Performance and Catastrophe Risk Management

Travelers achieved an impressive combined ratio of roughly 89.9% in FY2025, signifying underwriting profitability that exceeds industry averages typically challenged by catastrophe exposures [F1][S1]. This performance is attributed to disciplined pricing strategies, rigorous risk selection, and expense management.

A core challenge in property and casualty insurance remains the unpredictable nature of catastrophes—ranging from severe weather events intensified by climate change to man-made disasters—which add volatility to loss experience [S1]. Travelers actively employs sophisticated catastrophe modeling tools incorporating multiple assumptions about peak perils including hurricanes, wildfires, hailstorms, and flood risks to estimate potential losses comprehensively.

These models are augmented by layered reinsurance programs helping to mitigate large loss shocks while preserving capital adequacy [S1]. However, Travelers acknowledges limitations due to variable model accuracy particularly for emerging risks like cyber insurance where historical data scarcity heightens uncertainty.

Inflationary pressures have increased claims settlement costs post-event due to demand surge effects on materials and labor —a factor Travelers integrates into its reserving [N10][S23]. Reserve estimation remains an inherently imprecise process affected by evolving judicial environments around mass torts such as asbestos claims that pose latent exposure risks [S21][S24].

Capital Allocation: Balancing Shareholder Returns with Growth Investments

Capital stewardship is a cornerstone of Travelers’ financial strategy blending attractive shareholder returns with prudential underwriting capital demands.

In FY2025 alone, the Company returned approximately $3 billion via share repurchases—a notable increase from $1 billion repurchased in FY2024—and paid nearly $1 billion in dividends reflecting modest sequential increases aligned with earnings growth [F1][S7][S9][S29]. This level of buyback activity underscores confidence in valuation support yet remains calibrated against maintaining sufficient surplus for underwriting expansion.

Strong operating cash flows underpin this flexibility; in FY2025 operating cash flow expanded nearly seventeen percent year-over-year reaching over $10 billion, comfortably funding both business investments and shareholder distributions without reliance on external debt issuance [F1][S4–S8].

Liquidity at the parent company level is robust with roughly $2.4 billion held in liquid assets exceeding annual interest expenses plus dividends obligations—a target designed for financial resilience—and access to a $1 billion credit facility expiring mid-2027 enhancing contingency readiness [S4][S6]. Regulatory dividend restrictions limit upstream transfers from insurance subsidiaries but current availability permits significant discretionary distributions without prior approval from the Connecticut Insurance Department [S12].

This framework highlights measured capital return pacing mindful of regulatory constraints while preserving capacity for premium growth opportunities.

Evolving Competitive Pressures and Regulatory Landscape

The property and casualty sector continues to face pressure from emerging competitors including private equity-backed entrants deploying digital platforms emphasizing direct-to-consumer sales and usage-based insurance models leveraging telematics data [N5][S20]. Such entrants challenge traditional agency-distributed carriers like Travelers on pricing agility and customer engagement innovation.

Conventional brokers are consolidating portfolios affecting negotiation dynamics whereby fewer insurers compete for packaged risks potentially compressing margins or necessitating enhanced differentiation strategies focused on service quality or specialized products [S27][S28].

Regulatory environments impose layered compliance complexities beyond base capital requirements encompassing scrutiny on product filings, cybersecurity controls, anti-fraud measures including model governance for artificial intelligence-based underwriting enhancements—areas requiring ongoing investment attention by Travelers [S19][S26].

Volatile macro conditions related to inflation affect claims severity while frequent litigation developments around long-tail exposures like asbestos or PFAS may generate periodic reserve adjustments impacting earnings stability [S23][S24][N10]. The confluence of these factors challenges insurers to balance innovation adoption against cost discipline to sustain competitive positions.

Outlook and Future Growth Drivers to Monitor

Near-term prospects rest on continued selective premium rate increases supported by disciplined underwriting adjustments responding to loss trends and expense inflation as articulated during Q1 2026 earnings communications [N1][N13]. Management underscores vigilance on catastrophe claim developments amid variable weather patterns linked to climate change risks.

Reinsurance renewal cycles remain pivotal; pricing environment hardening or softening will affect net retention strategies affecting combined ratios going forward [N6][S1]. Technological advancement adoption—particularly AI-driven pricing analytics or enhanced data integration—constitutes both opportunity for efficiency gains and threat if lagging behind competitors materially.

Investors are advised to monitor regulatory policy updates influencing dividend capacities or distribution practices alongside competitive shifts instigated by altered consumer buying behaviors fueled by digital transformation dynamics within P&C insurance markets.

Financial Health Confirmed by Strong Liquidity and Robust ROE

Travelers’ balance sheet reflects substantial capitalization growth with shareholders' equity increasing from approximately $27.9 billion at FY2024 to nearly $32.9 billion at FY2025-end supported by cumulative comprehensive income gains including unrealized investment improvements attributable partly to interest rate changes [F1][S18][S26].

Return on equity measured at circa 19.1% for FY2025 illustrates effective utilization of capital amidst inherent sector volatility associated with natural disaster exposure variability [F1]. Debt levels remain manageable with total capitalization around $42 billion maintaining conservative leverage ratios consistent with strong financial strength ratings which support competitive advantage in reinsurance procurement cost effectiveness.

The combination of solid operating cash flow conversion exceeding $10 billion annually alongside active capital redeployment programs through share repurchases sustains shareholder value creation balanced against prudent liquidity buffers required for underwriting commitments under volatile loss scenarios.

This analysis synthesizes publicly available financial data up to early April 2026 along with recently filed SEC disclosures and market commentary sources without projection beyond cited facts or speculative guidance estimates.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments