Arrive AI Advances Autonomous Last Mile Network While Facing Liquidity and Profitability Constraints

The company builds an integrated hardware-software platform for drone and robot delivery but remains challenged by financing and scale.

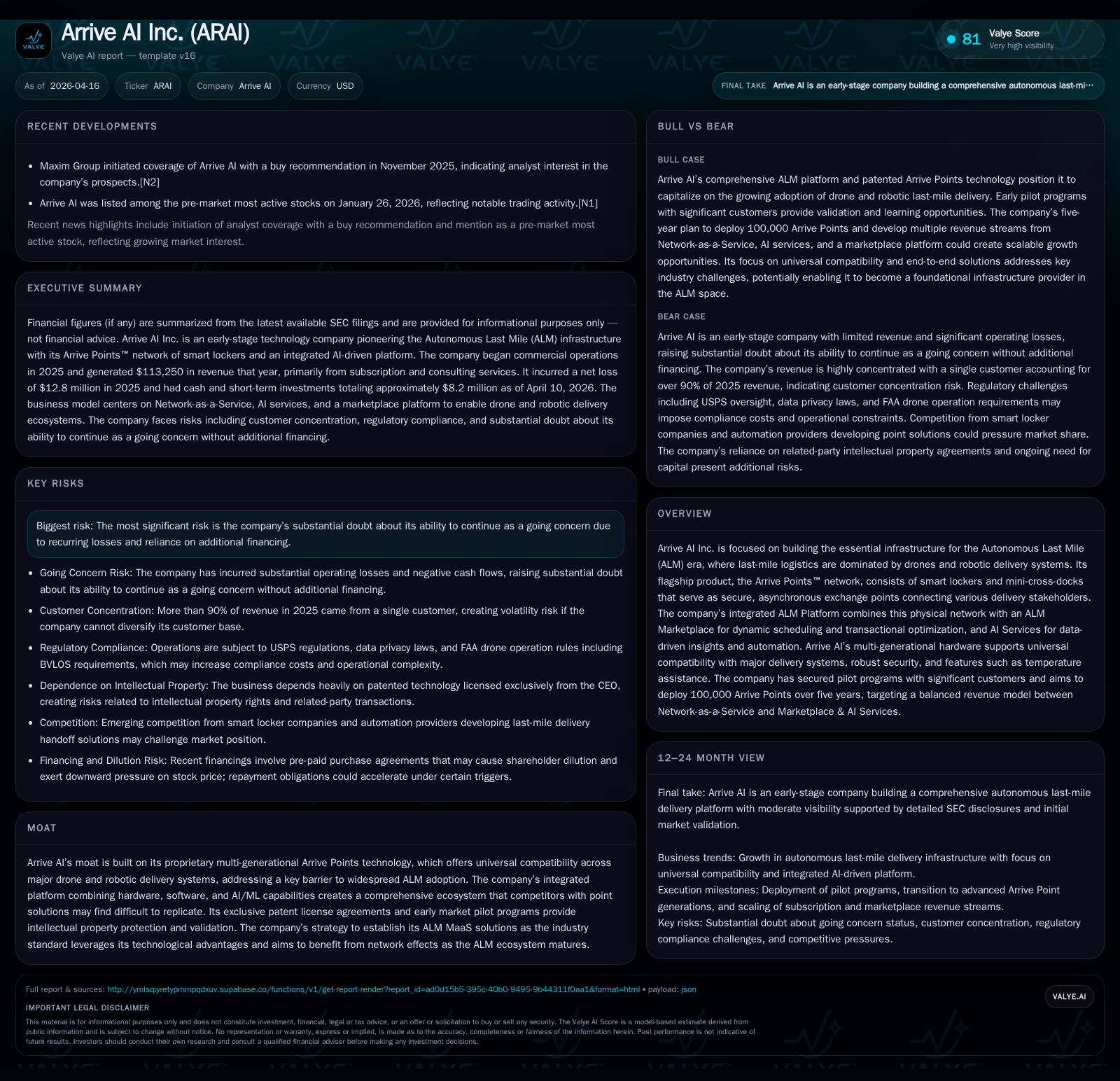

Arrive AI Inc. is pioneering infrastructure for autonomous last-mile delivery through its proprietary Arrive Points smart lockers and an AI-driven platform combining logistics, marketplace, and data services. Since commencing operations in 2025, revenue generation has begun but remains highly concentrated with a single customer. The company aims to deploy 100,000 units over five years to balance subscription services with transactional marketplace revenue. Despite technological progress and pilot validations, recurring losses and substantial liquidity risks present significant barriers to sustainable growth. Monitoring capital raises, milestone deployments of next-gen hardware, and customer diversification will be critical going forward.

Company Overview and Historical Performance

Arrive AI Inc., incorporated in April 2020 (initially as Dronedek Corp.), positions itself as an essential infrastructure provider for the Autonomous Last Mile (ALM) era where last-mile logistics increasingly rely on drones and robotic delivery systems [S1]. Its core innovation is the Arrive Points™ network—a system of smart lockers and mini cross-docks facilitating secure asynchronous exchanges among drones, robots, businesses, and consumers.

Commercial operations only commenced in 2025 after multiple iterations of proprietary hardware culminating in the third generation (AP3) units installed late 2024 [S1]. Previously the company reported no revenues as it focused on R&D and pilot validations. Revenues recognized since have predominantly arisen from subscription-based access to these Arrive Points alongside installation and support contracts.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Revenue figures are not explicitly detailed beyond disclosures that Hancock Health accounted for more than 90% of total sales in 2025 [S17]. Substantial operating losses and negative cash flows reflect ongoing investments in technology development and commercial expansion [F1]. Capital expenditures surged more than tenfold year-over-year indicating scale-up efforts underpinned by larger hardware deployment initiatives. Share repurchases were limited relative to the authorized $10 million program reflecting prioritization of liquidity preservation [S12].

Revenue Streams and Growth Outlook

Arrive AI’s business model targets three principal revenue streams:

Subscription Services: Recurring fees for access to Arrive Points networks including installation and maintenance support. This network-as-a-service approach enables customers—businesses or eventually end consumers—to leverage turnkey smart lockers deployed strategically.

Data Monetization: Advanced machine learning (ML) and artificial intelligence (AI) models extract insights from IoT data collected via Arrive Points operations. The AP4 and AP5 units embed edge computing capabilities enabling localized environment monitoring and interactions with delivery drones/robots while broader transactional data is analyzed centrally [S1].

Autonomous Last Mile Marketplace: An ALM platform operates akin to an advertising auction model optimizing scheduling and utilization of dock space across the network. The integrated marketplace manages real-time delivery logistics including micro-weather inputs, regulatory compliance, notifications, transactional updates, and automation issue resolution [S1]. Full marketplace economics are expected with AP5 rollout.

The five-year plan targets deploying approximately 100,000 Arrive Points balancing revenues evenly between Network-as-a-Service subscriptions (50%) and Marketplace/AI services (50%) [S16]. Early pilots with regional hospitals and pharmaceutical delivery firms provide validation though recurring costs remain elevated [S1][S16]. Expansion depends on scaled rollouts combined with AP4/AP5 hardware upgrades unlocking advanced marketplace functionalities.

Financial Performance Analysis

Net loss increased to approximately $12.8 million in 2025 driven by sustained R&D spending ($600K), general administrative expenses including stock-based compensation ($2.5M), interest expense related to convertible debt (~$687K), alongside costs associated with expanding physical infrastructure such as manufacturing Arrive Points [S15][S24][F1].

Operating cash flow was negative at over $8 million reflecting nascent commercial demand relative to fixed costs; free cash flow also remained negative near $8.75 million after accounting for capital expenditures which rose significantly compared to prior periods [F1][S7].

A January 26, 2026 convertible note financing raised net proceeds of $9.6 million under terms allowing up to $40 million gross borrowings subject to conditions including minimum market capitalization ($100 million) currently unmet — creating uncertainty around further draw availability [S4][S6][S9].

As of April 10, 2026 cash plus equivalents stood at approximately $8.2 million following financing inflows; however, a current ratio near 0.34 highlights short-term liquidity pressures given liabilities exceed working assets substantially [F1]. Accumulated deficits surpassing $24 million since inception underscore challenges sustaining operations without additional funding [S2].

Capital Structure & Allocation

Arrive AI carries significant convertible debt primarily via Streeterville Capital arrangements structured as prepaid purchase agreements translating into future equity dilution at discounts relative to market prices — exerting downward pressure on share valuation alongside accelerated repayment triggers if stock price or covenants falter [S2][S11][S25]. Post fiscal year-end conversions issued over thirteen million common shares significantly diluting existing shareholders [S20][S25].

Capital allocation priorities emphasize liquidity preservation: approximately $495K spent on capital expenditures contrasted with modest share repurchases ($75K spent versus a $10 million authorization), reflecting funding constraints rather than shareholder returns such as dividends which remain absent given losses [F1][S12]. Research expenses support progression toward AP4/AP5 products critical for unlocking marketplace economics while advertising spend moderated contributing to contained sales & marketing costs [S15][S24].

Business Risks & Regulatory Challenges

Recurring losses raise material uncertainty about Arrive AI’s ability to sustain operations absent further funding rounds which are uncertain given market conditions tied also to share price thresholds affecting Streeterville draws availability [S4][S19][S21]. Customer concentration risk persists with one client providing over ninety percent of revenue limiting visibility until diversification occurs across verticals such as healthcare deliveries or e-commerce autonomous last mile networks [S17].

Regulatory uncertainties regarding drone/robot deployment permissions at municipal levels may delay or limit geographic expansion or impose costly compliance impacting unit economics negatively versus initial growth assumptions [S13][S20]. Supply chain constraints affecting component availability pose risks slowing production ramp or inflating costs compressing margins during scaling phases [S8].

Intellectual property rights rely heavily on exclusive licenses from CEO Daniel O’Toole alongside pilot validations underpinning a competitive moat built around universal compatibility; exposure remains around patent disputes and related-party conflicts requiring robust governance to sustain technological advantage against emerging competitors [S1][S22]. Multiple ongoing litigations including employment claims represent contingent liabilities currently not expected to materially threaten viability but require resource allocation for legal defense [S11][S13].

Outlook & Monitoring Milestones

Explicit guidance is limited beyond strategic ambitions targeting network scalability over five years with full ALM marketplace functionalities anticipated via AP5 rollout milestones. Key indicators for monitoring progress include:

- Deployment trajectory toward tens of thousands of installed smart lockers aligned with incremental subscription revenues.

- Successful rollout of fourth- and fifth-generation hardware embedding edge computing essential for distributed ML inference powering advanced automation.

- Client base diversification beyond healthcare into retail/e-commerce sectors stabilizing revenues.

- Achievement of Nasdaq minimum valuation metrics influencing access to further financing under Streeterville agreements.

- Effective management of supply chain risks balancing inventory commitments against deployment urgency impacting top-line growth.

- Resolution or mitigation of litigation exposures strengthening IP defense.

- Movement toward positive free cash flow driven by economies of scale reducing reliance on dilutive convertible financing.

Conclusion

Arrive AI occupies a promising niche intersecting robotics, logistics automation, AI analytics, and last-mile delivery infrastructure presenting systemic value creation potential through its integrated ALM ecosystem combining smart hardware assets with software marketplaces supported by advanced analytics.

However, the company faces significant financial strain marked by escalating losses amid formative investment phases coupled with liquidity risks reliant on convertible debt facilities conditioned on market performance not yet realized posing existential risks without timely capital infusions or operational improvements.

Stakeholders should closely monitor capital adequacy updates including availability under Streeterville agreements alongside validation catalysts such as multi-customer rollouts beyond healthcare pilots paired with activation of next-generation platform capabilities unlocking diversified monetization streams beyond subscriptions.

Disclaimer: This analysis is based solely on publicly filed documents without any recommendation regarding investment decisions or securities transactions related to Arrive AI Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments