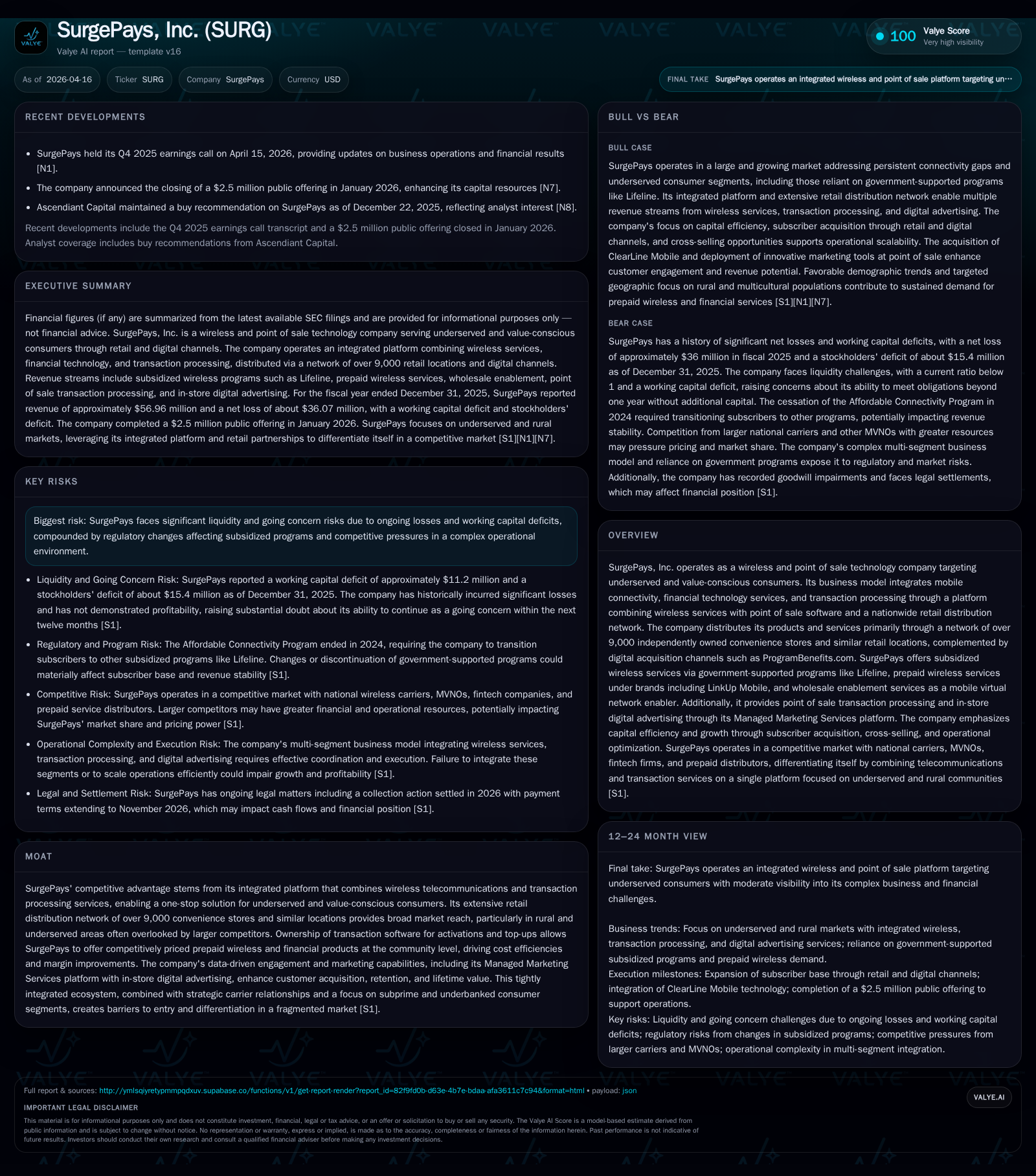

SurgePays, Inc. Reshapes Wireless and Fintech Access with Integrated Retail Ecosystem

SurgePays leverages its retail footprint and integrated platform to serve underserved communities amid subsidy program changes.

SurgePays, Inc. operates a unique integrated wireless and fintech platform targeting value-conscious consumers through a vast network of convenience stores and digital channels. The company experienced a significant revenue shift following the termination of Affordable Connectivity Program subsidies, leading to a steep decline in its MVNO segment but offset by growth in prepaid wireless top-ups and platform services. Despite ongoing operating losses and cash flow challenges, SurgePays relies on its extensive retail partnerships, proprietary software, and data-driven marketing to pursue subscriber retention and expansion into wholesale enablement. Key near-term indicators include subscriber base evolution and regulatory developments affecting subsidy programs.

Historical Revenue Dynamics: The Impact of Subsidy Program Changes

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 57 | -36 | -21 | -34 | -6.4% | +21.1% |

| 2024 | 61 | -46 | -21 | -42 | -55.6% | -321.8% |

| 2023 | 137 | 21 | 10 | 19 | +12.8% | +3128.6% |

| 2022 | 122 | -1 | 1 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -21 | 235.0 |

| 2024 | -22 | -298.6 |

| 2023 | 10 | 73.0 |

| 2022 | 1 | -13.6 |

Source: SEC companyfacts cache [F1].

SurgePays' financial narrative over recent years is dominated by the material impact of government subsidy modifications. In particular, the conclusion of the Affordable Connectivity Program (ACP) funding as of June 1, 2024 caused a sharp contraction in the company's Mobile Virtual Network Operator (MVNO) segment revenues. Revenue from this unit fell from $43.5 million in 2024 to just $13.5 million in 2025—a staggering 69% drop driven by the disappearance of monthly ACP discounts previously paid to subsidize consumer broadband access [F1][S1].

To preserve market presence post-ACP, SurgePays strategically maintained its existing subscriber base of approximately 250,000 users from the discontinued program by absorbing associated wholesale costs estimated at $7-10 per subscriber per month [S1]. The company concurrently transitioned over 80,000 users into the Lifeline subsidized program during 2024 and continued expansion efforts within this government-supported offering in 2025.

Overall consolidated revenue slipped modestly by 6.4% year-over-year to about $57 million in 2025, reflecting this significant tradeoff between subsidy-driven MVNO services losing ground while other segments partially compensated [F1][S1]. This reallocation evidences a notable shift in SurgePays’ revenue mix under external policy pressure.

Segment Evolution: MVNO Decline Versus Prepaid Services Expansion

SurgePays' business divides primarily into two reporting segments: the MVNO segment providing subsidized wireless plans including Lifeline and non-subsidized prepaid wireless services (e.g., LinkUp Mobile), alongside Point-of-Sale (POS) and Prepaid Services which handle retail top-ups plus transaction processing [F1][S1][S5].

The precipitous fall in MVNO revenues was accompanied by robust growth in Point-of-Sale & Prepaid Services doubling revenues to approximately $43.5 million from roughly $17.4 million the prior year. This expansion is attributed to an increased footprint supporting prepaid wireless top-ups across more than 9,000 independently owned convenience stores nationwide plus digital acquisition via platforms like ProgramBenefits.com [S6][S8].

The shift from heavily subsidized consumer plans to less subsidy-reliant prepaid offerings aligns with SurgePays’ strategic repositioning toward more sustainable revenue streams amid federal funding withdrawals [S7]. The company’s point-of-sale transaction platform also extends beyond wireless services enabling activation of SIM cards, debit/gift card transactions, and real-time data capture that drives marketing initiatives [S9].

Market Positioning: Leveraging Retail Networks and B2B Wholesale Enablement

SurgePays differentiates itself through a comprehensive platform that integrates mobile wireless telecommunications with fintech-enabled transaction processing anchored within an expansive retail distribution network primarily comprised of convenience stores [S4][S6][S7]. This network reach enables service delivery where underserved rural or price-sensitive consumers live and shop.

Ownership of proprietary activation and top-up software embedded within retail POS systems facilitates lower-cost prepaid wireless products right at community level points of sale—capturing value-conscious customers that mainstream carriers often overlook [S4]. More recently, the company has scaled its wholesale enablement via an MVNE platform offering third-party providers SIM provisioning, billing services, and network access without direct carrier agreements—representing an emerging channel for growth leveraging existing carrier relationships [S7].

This multi-channel strategy is further augmented by the Managed Marketing Services platform deploying digital ad displays inside partner stores harnessing transaction data analytics for personalized offers designed to increase customer loyalty while providing added monetization avenues for SurgePays [S9]. This integrative approach creates distinct operational efficiencies few competitors match.

Financial Health Analysis: Operating Losses, Cash Flows, and Capital Resources

Despite strategic shifts supporting top-line stability in certain segments, SurgePays remains unprofitable on an overall basis. The company reported an operating loss of approximately $34 million in 2025—an improvement compared to a $43 million operating loss in 2024 but indicating continued high expenses relative to revenues [F1][S1]. Net losses stood near $36 million similarly reflecting ongoing structural challenges.

Cash flow from operations remains negative at roughly -$21 million annually despite low capital expenditures (about $18 thousand spent on capex in 2025 down sharply from over half a million the prior year) indicating stretched operational liquidity [F1]. The working capital deficit exceeds $11 million coupled with a current ratio below 0.4 highlights pressing short-term obligations exceeding available liquid assets [F1][S16][S27]. Interest expense rose substantially due to increased debt financing commitments further pressuring profitability margins [F1][S27].

While reported return on equity appears anomalously high at approximately 235%, this figure is mathematically distorted caused by negative equity due to accumulated deficits nearing $97 million [F1]. Overall financial health remains fragile with substantial going concern risks acknowledged by management.

Regulatory Risks and Their Consequences for Subscriber Sustainability

Government subsidy programs such as Lifeline represent critical revenue pillars but are plagued by regulatory volatility exposing SurgePays to material risks. The discontinuation of ACP directly triggered dramatic subscriber attrition impacting revenues significantly [S19][S20]. Additionally, changes relating to Lifeline enrollment rules or eligibility criteria could materially erode subscriber count or increase churn.

Legal challenges exist including ongoing litigation such as Blue Skies Connections et al v. SurgePays involving contract disputes that could impose liabilities though current judgments have limited material financial impact based on court rulings so far [S19][S26]. Nonetheless unsettled regulatory frameworks remain primary headwinds limiting foreseeable visibility around sustained subsidized customer engagement.

Operational Adaptations: Targeted Marketing and Ecosystem Synergies

Recognizing price sensitivity within its customer base, SurgePays has embraced data-driven engagement through Managed Marketing Services that apply POS transaction analytics enabling targeted social media campaigns plus customized loyalty offerings [S4][N1]. Such tools help differentiate convenience store partners’ shopping experience while simultaneously improving customer retention rates vital in a segment characterized by high churn risk.

Integrations with prevalent POS hardware providers (e.g., Clover, PAX) allow scalable deployment across various store formats without heavy incremental capital expenditures reinforcing scalability [S12][S13]. This continuous innovation pipeline enhances cross-sell opportunities among wireless subscribers, prepaid services customers, financial services users, and merchant clients creating operational synergies difficult for stand-alone telecom or fintech competitors to replicate.

Near-Term Catalysts and What Investors Should Monitor

Although explicit forward-looking guidance is absent, several milestones warrant attention as potential performance inflection points. Key areas include monitoring Lifeline subscriber growth particularly in geographies like California where additional state-level incentives exist supporting Torch Wireless expansion efforts [N1][S21].

The progression of wholesale enablement contracts leveraging SurgePays’ MVNE infrastructure should be watched carefully as this channel gains scale possibly adding recurring revenue streams outside traditional retail circles [N1]. Additionally, rollout momentum behind LinkUp Mobile’s phone-in-a-box offering through national retail may provide tangible uptake metrics signaling further prepaid segment traction [N1]. Regulatory developments affecting subsidy frameworks remain decisive variables governing future customer base stability.

Capital Deployment Strategy: Cash Management and Investment Focus

The company currently does not pay dividends nor conduct stock repurchases given its sustained net losses and negative free cash flow position (-$21.3 million CFO minus minimal capex equates roughly to -$21.3 million FCF in fiscal year 2025) [F1][N1][S16]. Capital resources appear focused primarily on subsidizing existing subscribers—absorbing wholesale costs post-ACP—and scaling operational capabilities aligned with long-term growth ambitions [S16][N1].

Low capital expenditure underscores emphasis on leveraging existing infrastructure rather than heavy investment cycles. The negative equity position limits typical ROE interpretations as historical losses have eroded shareholder funds substantially while pressuring balance sheet strength [F1][S16]. Overall capital allocation remains conservative given severe liquidity constraints coupled with regulatory uncertainties.

This analysis is based solely on disclosed financial statements and publicly available information as of April 16, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments