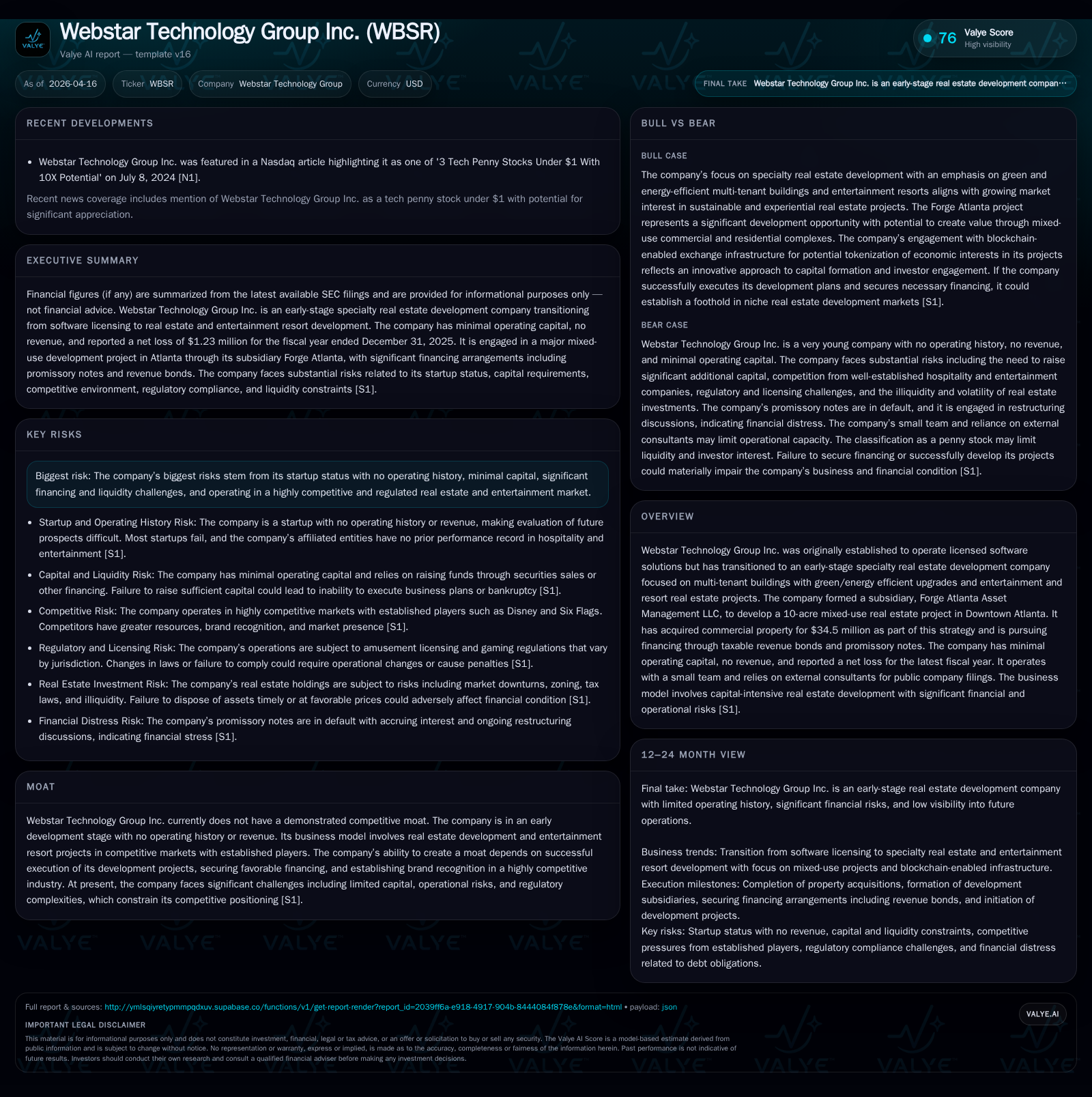

Webstar Technology Group’s Transition from Software to Specialty Real Estate Development

Webstar Technology Group shifted from software licensing to early-stage specialty real estate development, focusing on green buildings and entertainment resorts.

Originally a technology licensor, Webstar Technology Group has transformed into an emerging real estate developer specializing in multi-tenant green buildings and family entertainment resorts, exemplified by its Forge Atlanta project. Financials show persistent net losses with improving trends over recent years amid minimal operating capital and significant liquidity constraints. The company's capital-intensive strategy relies heavily on debt financing and equity raises, exposing it to dilution risks. Execution risks stem from its startup status, substantial financing needs, regulatory complexities, and competitive pressures. Key milestones include land acquisition closings, bond issuance progress, permitting approvals, and construction commencement.

Origins and Strategic Shift: From Software Licensing to Specialty Real Estate Development

Webstar Technology Group Inc., incorporated in Wyoming in 2015 initially focused on licensing proprietary software solutions such as Gigabyte Slayer and WARP-G. In mid-2024, new management acquired controlling interests and redirected the company towards specialty real estate development emphasizing multi-tenant green buildings and family entertainment resorts [S1]. Forge Atlanta Asset Management LLC was formed as a subsidiary tasked with developing a mixed-use project covering roughly 10 acres in Atlanta’s Castleberry Hill district with sustainability upgrades integrated into the design [S24].

Several material agreements throughout 2024 facilitated asset acquisitions including intellectual property related to prior gaming resorts and transfers of contracts to affiliated entities supporting the company’s diversified redevelopment strategy [S1][S20]. The brand identity is evolving away from pure software licensing towards real estate-focused operations.

Financial Performance: Ongoing Losses Amid Limited Operating Capital

The company remains pre-revenue with no reported operating income. Operating losses have narrowed from -$17.07 million in FY2022 to approximately -$495k in FY2025. Net income losses also improved significantly from -$31.02 million in FY2022 to -$1.23 million in FY2025 representing a nearly 73% improvement year-over-year compared to FY2024 [F1]. Operating cash flow remains negative at about -$761k.

Liquidity constraints are acute with cash & equivalents totaling $4,271 against current liabilities near $39.6 million as of December 31, 2025 resulting in a current ratio below one (0.96). This highlights reliance on external funding sources to sustain operations prior to revenue generation [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | -761410 | 0 | +72.7% |

| 2024 | -4 | -111934 | 0 | -391.9% |

| 2023 | -1 | -131929 | -1 | +97.1% |

| 2022 | -31 | -174917 | -17 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 55.8 |

| 2024 | 416.2 |

| 2023 | 20.9 |

| 2022 | 852.1 |

Source: SEC companyfacts cache [F1].

Table illustrates progressive narrowing of losses but sustained negative cash flows consistent with early-stage capital consumption.

Core Projects: Forge Atlanta Development and Green-Efficient Facilities

Forge Atlanta anchors the company’s real estate portfolio secured via a $34.5 million commercial property purchase finalized late 2025 under a Commercial Purchase and Sale Agreement for two land lots in Fulton County Georgia [S11]. Payment obligations are structured through promissory notes bearing escalating default interest rates due to missed maturities; discussions are ongoing for restructuring terms extending maturity into late 2026 [S11].

The Fulton County Development Authority has agreed to issue up to approximately $224 million in taxable revenue bonds aimed at funding planning and implementation phases of the Forge Atlanta project. The bonds’ structure allows the Authority either to lease or sell the project back or loan proceeds directly post-issuance—typical of municipal credit facilitation arrangements balancing risk between public authorities and private developers [S8].

An innovative component emerged on February 3, 2026 when Forge Atlanta entered an Exchange Licensing Agreement with Torch LLC for blockchain-enabled infrastructure potentially linked to tokenized economic interests within the development project—reflecting early-stage adoption of digital asset frameworks for financing or transactional purposes [S10].

Capital Structure: Heavy Reliance on Debt Financing and Equity Raises

Webstar’s capital base includes authorized common stock of up to 500 million shares with roughly 405 million shares outstanding at last reporting—providing capacity for further dilutive issuances during fundraising rounds [S6][F1]. The company’s penny stock classification imposes additional resale restrictions impacting liquidity for retail investors [S7].

Beyond equity raises totaling $500k for preferred stock acquired mid-2024, the firm relies extensively on promissory notes carrying escalating default interest rates due to repayment delays alongside planned multimillion-dollar bond issuances underscoring refinancing pressures [S7][S11][S28]. These financing dependencies elevate dilution risk as new investors or creditors may obtain preferential rights affecting existing shareholder value.

Risks: Emerging Developer Without Operating Revenue Facing Regulatory and Market Challenges

SEC filings highlight multiple risks associated with Webstar’s startup status including absence of operating history or proven hospitality expertise among management or affiliates [S1][S14]. Notable risk factors include:

- Regulatory hurdles obtaining liquor licenses essential for resort operations; failure could materially impair business prospects or expansion plans [S21].

- Exposure under dram shop liability statutes posing potential punitive damages beyond insurance coverage; currently the company lacks insurance policies addressing such exposures increasing financial vulnerability if claims arise [S21][S22].

- Compliance challenges related to amusement game licensing amid evolving legalized gambling laws which may require operational modifications adversely impacting offerings [S22].

- Illiquidity of real estate holdings may delay asset disposals or force sales at unfavorable valuations especially if leisure sector downturns occur affecting financial condition [S25].

- Intense competition from established industry leaders including Disney and Six Flags limiting market penetration while consumer preferences remain volatile undermining demand predictability for new venues [S13].

- Legal exposure heightened by affiliated party transactions raising conflict-of-interest concerns alongside concentrated governance reducing investor influence over strategic decisions; historical internal control weaknesses also reported by auditors increasing uncertainty around execution oversight [S26][S27].

Collectively these factors underscore high operational uncertainty elevating insolvency risk absent successful capital raises or milestone achievements.

Outlook: Critical Milestones Include Fundraising Progress and Permitting Approvals

Absent explicit guidance or revenue forecasts publicly provided by the company analysts must monitor key milestones that will inform valuation prospects:

- Completion of additional land acquisitions critical for phased project expansion beyond initial Castleberry Hill site.

- Advancement of Fulton County Development Authority’s taxable revenue bond issuances exceeding $200 million necessary for construction funding under favorable terms minimizing cost overruns.

- Attainment of requisite zoning changes and permitting approvals enabling permitted resort operations aligned with construction schedules.

- Securing necessary liquor licenses enabling full facility openings while managing risks associated with gaming regulation compliance preserving operational flexibility.

- Initiation of construction activities demonstrating capital deployment capability alongside prudent cost containment reflecting disciplined capital stewardship over extended development horizons.

These operational inflection points provide tangible markers for investors assessing execution capabilities ahead of first revenue generation.

Capital Allocation: No Dividends or Buybacks; Dilution Risk Persists

Reflecting ongoing net losses coupled with reinvestment priorities Webstar maintains no dividend payments nor share repurchase programs consistent with early growth phase realities lacking distributable cash flows [F1][S6]. All available capital is directed toward project development costs.

Given substantial authorized common stock alongside persistent liquidity shortfalls necessitating further equity issuances shareholders should anticipate dilution risks inherent in ongoing capitalization efforts essential for corporate survival but potentially adverse for per-share value absent commensurate operational scaling or profitability improvements.

This analysis is based exclusively on publicly filed SEC disclosures without extrapolation or predictive valuation assumptions. Early-stage companies like Webstar Technology Group face significant variability across operational dimensions rendering future outcomes uncertain.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments