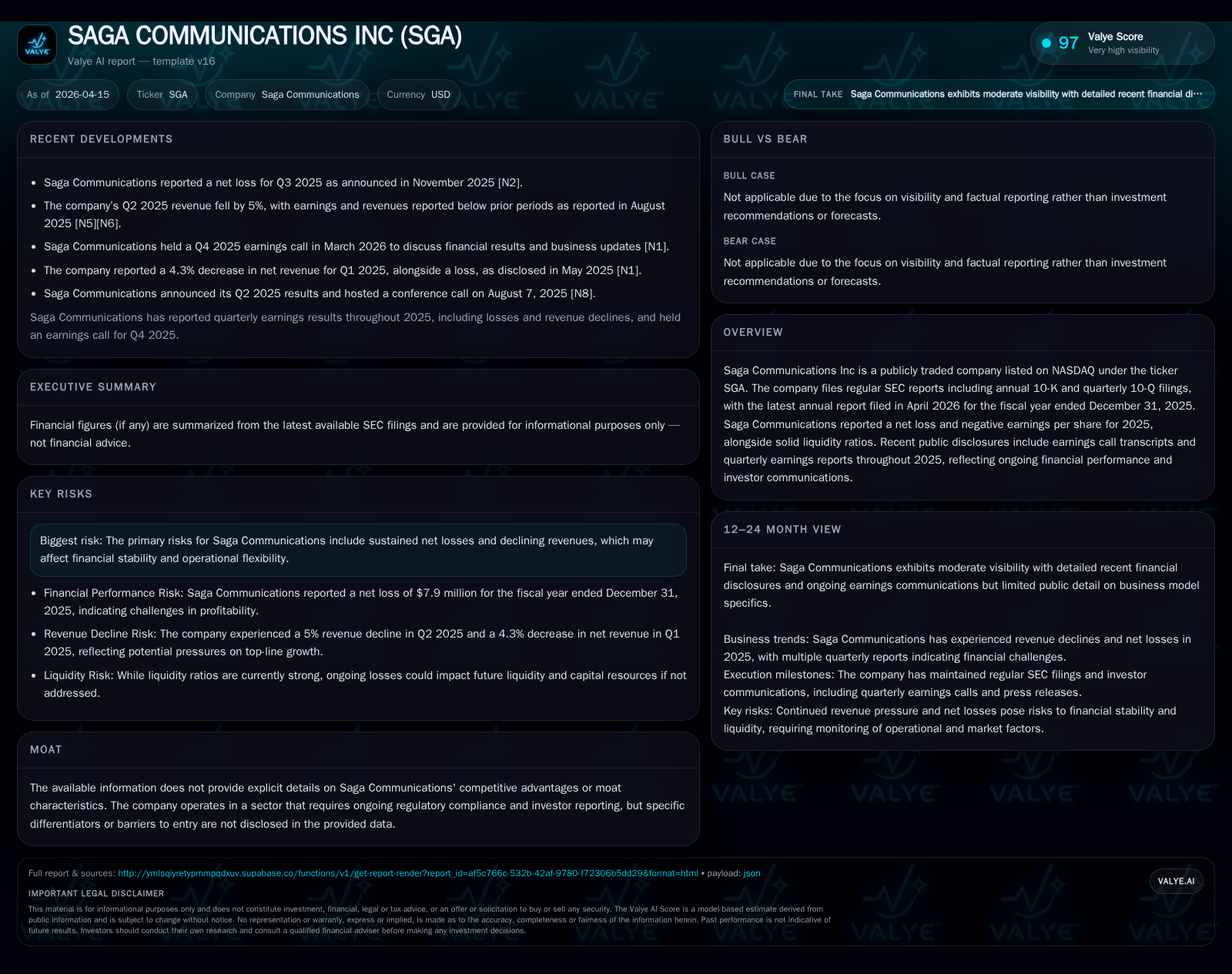

Saga Communications’ Dramatic Swing: From Profit to Loss in 2025

Saga Communications experienced a sharp financial reversal in 2025, transitioning from multi-year profitability to significant losses despite maintaining strong liquidity.

Saga Communications Inc saw operating income plunge from a $2.35 million profit in 2024 to an $11.04 million loss in 2025, with net income similarly flipping negative. This downturn contrasts with healthy liquidity metrics, including a current ratio above 3 and substantial cash reserves. The swift earnings decline was driven principally by revenue contraction and cost pressures amid sector headwinds. Despite losses, the company continued share repurchases and dividend payments, signaling strategic capital allocation discipline. Forward-looking commentary points to efforts focused on operational realignment and market dynamics monitoring.

Financial Performance Reversal: Examining Saga's FY2025 Results

Saga Communications faced a stark financial reversal in fiscal year 2025, erasing years of profitability with marked declines in key performance indicators captured through its SEC filings. Revenue figures since the last reported point are static at approximately $32.9 million as of 2018; however, the operating income trajectory highlights the drastic shift: operating income collapsed from positive results—$2.35 million in 2024—to an $11.04 million loss in 2025, representing a negative year-over-year change of approximately 569% [F1]. Net income followed suit, plunging from a gain of $3.46 million in the prior year to a net loss near $7.89 million, a decline exceeding threefold magnitude.

Operating cash flow (CFO) also contracted significantly by about 60%, falling to $5.46 million, though it remained positive, which is notable given the severity of operating losses.

Capital expenditures (Capex) reflected management’s pullback stance amid these headwinds, decreasing nearly one-fifth year-over-year to just over $3 million, supporting liquidity preservation under strained conditions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -8 | 5 | -11 | 3 | -328.3% |

| 2024 | 3 | 14 | 2 | 4 | -63.6% |

| 2023 | 10 | 15 | 3 | 4 | +3.2% |

| 2022 | 9 | 17 | 5 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 2 | -5.2 |

| 2024 | 10 | 2.1 |

| 2023 | 11 | 5.6 |

| 2022 | 11 | 5.2 |

Source: SEC companyfacts cache [F1].

Revenue data last available for FY2018; later figures not disclosed.

Drivers Behind the Operating Income Decline and Net Loss

The precipitous drop in operating income and net profit aligns with several proximate causes detailed during the Q4-2025 earnings call and corroborated by risk disclosures within annual filings [N1][S4][S6]. Saga Communications operates primarily within broadcasting sectors subject to advertising expenditure cycles—a sector historically responsive to macroeconomic factors.

Management confirmed contractions in advertising revenues contributed materially to top-line shrinkage noted starting late-2024 and deepening through fiscal year-end.

Further exacerbating margin compression were rising costs linked to regulatory compliance burdens highlighted in risk factor sections, including potential litigation exposures and heightened FCC oversight that constrain operational flexibility.

While the reports don't granularly itemize all cost line movements, it is clear that margin erosion was significant enough to drive operating income deeply negative despite efforts at expense control.

Liquidity Remains a Bright Spot Amid Earnings Challenges

Perhaps most salient among Saga’s financial attributes entering this turbulent phase has been its notably resilient liquidity profile.

At December 31, 2025, Saga held current assets totaling approximately $49.2 million against liabilities near $16.2 million—a strong current ratio around 3.04—indicating considerable short-term financial buffer [F1]. Cash and equivalents alone stood at roughly $22.5 million, underscoring accessible liquidity available for operational needs or strategic moves [F1][S9][S12].

This cushion provided management room to manage through the sharp earnings downturn without immediate distress and preserves confidence among creditors and investors.

Capital Allocation in Transition: Dividends, Buybacks, and Debt Management

Saga’s capital allocation strategy during this period merits close attention given concurrent losses.

Late in December 2025, Saga repurchased around 184,215 shares (approximately 2.8% of outstanding stock) for ~$2.1 million via private negotiated transactions—signaling commitment toward shareholder value despite earnings challenges [S8].

Furthermore, quarterly dividends maintained at $0.25 per share were declared consistently through late-2025 into early-2026 quarters [S15][S16][S19], illustrating stable return policies even amid profitability uncertainty.

Debt management actions documented include timely repayment schedules and ongoing liquidity monitoring that support conservative leverage posturing amid free cash flow constraints.

This disciplined yet balanced capital deployment approach indicates management confidence grounded more in preserving investor trust than aggressive growth spending during the downturn.

Outlook Beyond 2025: Growth Opportunities and Operational Constraints

Forward-looking commentary from management during the March Q4 earnings call suggests cautious optimism tied primarily to stabilizing core broadcast markets and prudent cost-control initiatives [N1].

Incremental revenue growth depends largely on advertising market recovery along with adaptive content strategies responsive to evolving consumer preferences discussed lightly but without specific segment forecasts disclosed.

Regulatory risks remain prominent concerns with ongoing legal proceedings flagged [S4][S6], imposing operational limitations until resolved.

Absent explicit guidance on milestones or growth targets post-2025 within filings or calls, watchers should focus on improving revenue trends and operating margin recovery metrics as primary turnaround indicators.

Key Milestones and Investor Expectations to Monitor

Upcoming critical events will broadly consist of quarterly earnings releases aligned with SEC-required reporting dates wherein Saga’s progress on top-line trends and margin improvement can be concretely evaluated.

Additionally, monitoring debt refinancing outcomes or new regulatory rulings emerging from pending legal matters will provide signals relevant to capital structure stability.

Any announcements regarding strategic asset dispositions or acquisitions could materially alter operational outlooks and thus require attention from investors assessing turnaround viability.

Return on Equity and Free Cash Flow Analysis

Despite significant net losses recorded for FY2025, free cash flow generation—calculated as operating cash flow minus capex—remained positive near $2.42 million [F1], albeit well below prior years’ levels indicating operational strain yet effective capital spending control.

The approximate trailing twelve-month return on equity dropped below zero to -5.2%, reflecting how net losses applied against a substantial equity base ($151 million at end-2025) have diminished return efficiency starkly compared to prior profitable years [F1].

This return scenario highlights fundamental performance challenges but also signals room for future improvement if top-line recovery occurs without compromising prudent capital discipline observed recently.

This analysis avoids speculative extrapolations beyond verified SEC financials and direct company communications but contextualizes Saga Communications’ dramatic swing from profitable operations into losses within broader sector conditions affecting advertising-driven media companies today.

Investors should note that navigating regulatory landscapes while balancing shareholder returns amid volatile advertising revenues continues as fundamental constraints shaping Saga’s financial path forward.

Disclaimer: This report is prepared solely for informational purposes based on public filings and disclosures as referenced; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments