Mag Mile Capital's Surge in Deal Volume Reinforces Niche Real Estate Finance Strategy

Recent record financing executions evidence Mag Mile Capital’s expanding deal footprint amid persistent liquidity challenges.

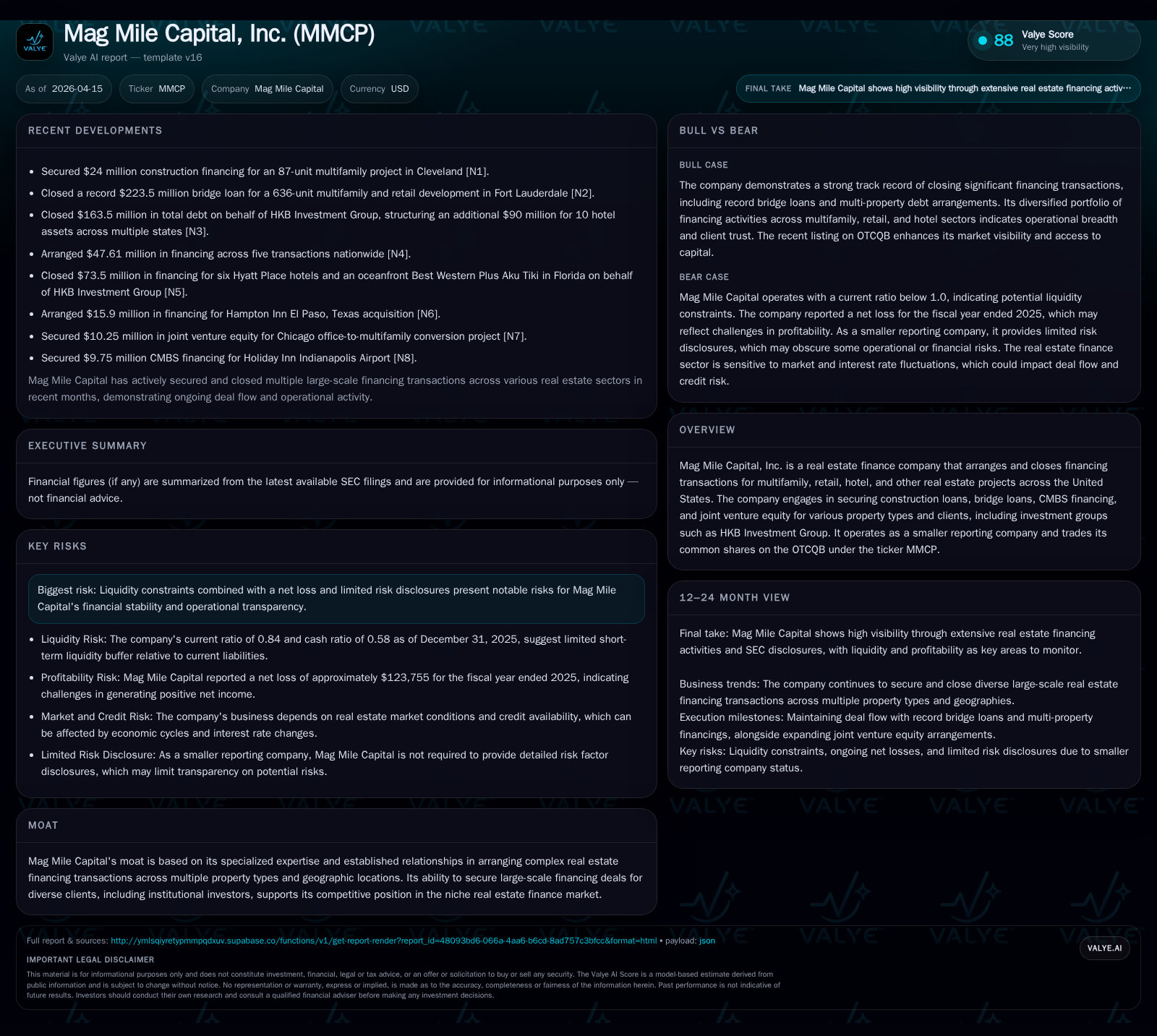

Mag Mile Capital, Inc., an emerging player in U.S. real estate finance, recently closed several landmark loans across multifamily, retail, and hotel sectors, underscoring its growing operational traction. Despite these transactional successes highlighted by a $223.5 million bridge loan for Fort Lauderdale and significant construction and debt financings, the company continues to wrestle with suboptimal liquidity metrics and recurring net losses. Historical financials reveal rapid revenue growth juxtaposed with ongoing operating deficits and a constricted current ratio. The firm’s niche expertise in structuring complex multi-jurisdictional financings remains a differentiator, but capital allocation remains conservative amid earnings pressure. Forward monitoring should focus on sustained deal flow, profitability trends, and balance sheet strengthening maneuvers.

Recent Landmark Financings Define Growth Trajectory

Mag Mile Capital has demonstrated notable momentum through several high-profile real estate financing transactions during early 2026. The company announced closing a $223.5 million bridge loan financing package for a large-scale mixed-use development located in Fort Lauderdale featuring 636 multifamily units combined with retail space [N2]. Within days, it secured an additional $24 million construction loan supporting an 87-unit multifamily complex in Cleveland [N1]. Further expanding its product range, Mag Mile also facilitated $163.5 million in total debt procurement for hotel assets managed by HKB Investment Group across multiple states [N3]. These deals emphasize Mag Mile’s capacity to originate and structure significant multi-jurisdictional financing solutions across diverse real estate categories, leveraging its specialized expertise in bridge loans, construction lending, and CMBS transactions.

The breadth of property types—multifamily housing, mixed-use retail components, hospitality—and geographic diversification underscore the firm’s ability to penetrate different market verticals within the U.S. real estate landscape. This expanded execution footprint cements Mag Mile’s position as a go-to arranger among institutional investors requiring complex debt and equity structuring.

Historical Financial Performance and Impact on Profitability

Examining Mag Mile Capital’s financial journey over the past three fiscal years reveals strong revenue acceleration counterbalanced by persistent operating losses albeit at diminishing magnitudes (see table below).

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4 | 0 | 513293 | 0 | +98.0% | +56.3% |

| 2024 | 2 | 0 | -210738 | 0 | +6.9% | +90.9% |

| 2023 | 2 | -3 | -537869 | -3 | -4651.4% | |

| 2022 | 0 | -65288 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 42.6 |

| 2024 | 170.1 |

| 2023 | -2668.1 |

| 2022 | 172.9 |

Source: SEC companyfacts cache [F1].

[F1]

Revenue witnessed a near doubling (+98%) from approximately $2 million in FY2024 to over $4 million in FY2025 as Mag Mile scaled deal executions clearly reflected in the recent large financings discussed earlier. Operating income losses have substantially narrowed—from deep negative territory exceeding $3 million in FY2023 to approximately -$115 thousand in FY2025—a positive signal of enhanced cost discipline and operational leverage despite remaining unprofitable.

Notably the net loss trajectory follows similar improvement trends but Mag Mile has yet to reach profitability on the bottom line level. Its operating cash flow position turned positive appreciably in FY2025 from prior years’ use of cash resulting from increased fees collected from completed transactions offsetting operating expenses.

This mix suggests that while operational scaling is underway via higher transaction volumes and fee income growth, margin expansion has not fully materialized possibly due to upfront costs associated with deal origination or administrative overheads typical within specialized real estate finance activities.

Operational Challenges: Addressing Liquidity and Net Losses

Scrutiny of Mag Mile’s balance sheet indicates liquidity pressures consistent with its small scale and recent loss-making operations. The current ratio stands at approximately 0.84 at the end of FY2025 ([F1]), revealing that current liabilities exceed current assets—a classical liquidity red flag for potential short-term funding constraints.

Equity was reported negative $290 thousand at FY-end ([F1]), reflecting accumulated losses eroding shareholder capital over time since FY2023 when equity was positive $117 thousand but declining materially thereafter.

Compounding challenges is the company’s smaller reporting entity status which exempts it from comprehensive risk factor disclosures typically seen with larger firms ([S1], [S3]). This lack of granular visibility limits external assessment of contingent liabilities or operational risks beyond publicly available financial statements.

With limited cash reserves just above half a million dollars at year-end ([F1]), reliance on continued successful deal closure cycles appears crucial for sustaining working capital adequacy amid net losses that reduce retained earnings.

Strategic Positioning Within a Competitive Real Estate Finance Niche

Mag Mile Capital occupies a specialized niche focused on arranging complex financing solutions such as bridge loans—which provide interim capital pending longer-term refinancing—and construction loans essential for new developments’ cash flow needs.

Its clientele includes sophisticated institutional investors like HKB Investment Group who utilize Mag Mile’s capabilities to structure flexible debt packages tailored across property types including hotels and mixed-use projects ([N3], valye_report_excerpt). The firm’s emphasis on multi-jurisdictional deal origination enhances its competitive moat by enabling offerings across multiple regional markets rather than single market concentration.

This depth of expertise combined with established lender-borrower relationships facilitates access to diverse capital sources including conduit lenders for commercial mortgage-backed securities (CMBS), further broadening product offerings.

Capital Allocation Approach Amid Financial Constraints

Analyzing returns shows an approximate return on equity around +42.6% due largely to the fact that net income is negative but shareholders’ equity is also deeply negative at year-end—yielding distortions common when book value diminishes below zero ([F1]). This metric should be interpreted cautiously as it does not reflect true profitability strength but rather mathematical artifact from eroded equity.

Capital expenditures remain minimal indicating that Mag Mile operates a capital-light model typical of independent real estate finance arrangers prioritizing deal structuring over asset ownership or extensive physical infrastructure investment ([F1]).

The absence of dividend payments or share repurchase programs aligns with the company’s focus on conserving liquidity and reinvesting effort into scaling transaction volume amid financial tightening.

Positive operating cash flow generation observed recently provides some cushion for working capital requirements though maintaining this trajectory will depend heavily on sustained business inflows.

Outlook: What Should Investors Monitor Next?

No explicit future guidance from management has been identified within filings or news releases requiring investors to rely on qualitative indicators and subsequent quarterly disclosures ([N1], [N2], [N3]). Key areas to watch include:

- The consistency of large-scale loan closings comparable to recent $223.5 million bridge deals signaling ongoing revenue pipeline robustness;

- Expansion or diversification of financing products beyond bridge and construction loans potentially enhancing margin profiles;

- Any movement toward profitability inflection points manifested through narrowing net losses or sustained positive operating income;

- Improvements or deterioration in liquidity ratios and shareholders' equity reflecting efforts to stabilize the balance sheet;

- Potential updates or changes in risk factor disclosures which could reveal latent operational vulnerabilities.

Given the cyclical nature of real estate finance markets intertwined with macroeconomic interest rate environments affecting credit availability and borrower demand dynamics—monitoring external economic signals alongside company-specific developments remains prudent.

Disclaimer: This analysis is based solely on publicly available information provided through SEC filings and market news sources as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments