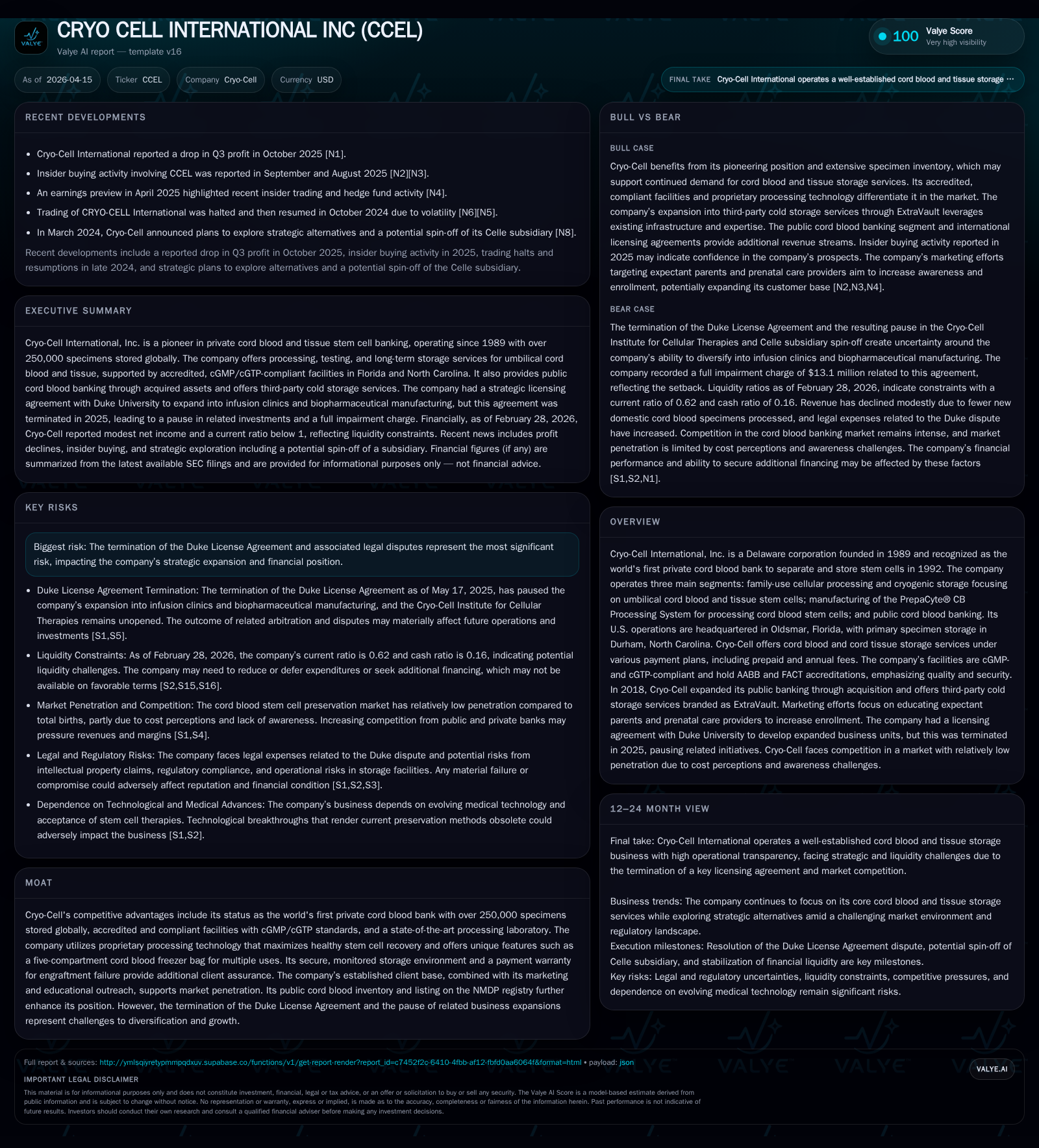

CRYO CELL INTERNATIONAL INC Navigates Legal Challenges and Liquidity Pressures Amid Stable Core Operations

While Cryo-Cell’s foundational cord blood storage business remains consistent, ongoing arbitration and capital constraints pose significant near-term headwinds.

Cryo-Cell International, Inc., the pioneer private cord blood bank, maintains a robust specimen base but faces substantial challenges from arbitration with Duke University following a key license termination. Its traditional cellular processing and storage segments continue as cash flow drivers, yet FY2025 saw sharply reduced operating income and expanded net losses amid investments and legal costs. Liquidity is constrained with cash under $250K as of early 2026, prompting reliance on credit facilities. Near-term growth depends on resolving legal disputes and advancing new service initiatives.

Background and Historical Performance

Established in 1989, Cryo-Cell International is recognized as the first private cord blood bank to separate and store stem cells starting in 1992 [S1]. The company operates through three main segments: cellular processing and cryogenic storage for family use focusing on umbilical cord blood and tissue stem cells; manufacturing of its proprietary PrepaCyte® CB Processing System; and public cord blood banking including assets acquired from Cord:Use [S1][S22].

Between fiscal years 2014 and 2017, the company’s revenue grew from approximately $20.1 million to $25.4 million, representing an annual growth rate near 9.8% [F1]. More recent top-line data beyond FY2017 is not available in the cited records.

Operating income has shown volatility with a peak above $4 million in FY2022 followed by a steep loss exceeding $12 million in FY2023 before recovering to $482 thousand in FY2025. Net income similarly swung between profits and losses, culminating in a net loss of approximately $2.43 million for FY2025 [F1]. These fluctuations largely reflect increased operating expenses tied to research and development initiatives, legal costs related to ongoing arbitration with Duke University concerning patent licenses, and infrastructure investments.

Business Model Stability Through Core Segments

The family-use cellular processing segment remains the company’s primary revenue source, driven by contracts involving prepaid or multi-year fees for cord blood and tissue processing and cryogenic storage recognized over time [S1][S25]. Marketing efforts leverage national field educators alongside online enrollment platforms targeting expectant parents [S16][S25].

Public cord blood banking via listings on the National Marrow Donor Program registry enhances reach with a diverse inventory valuable for transplant centers domestically and internationally [S22][S25]. The manufacturing of proprietary PrepaCyte® CB units supports technology differentiation.

The company operates cGMP- and cGTP-compliant facilities accredited by AABB and FACT, meeting FDA regulatory requirements critical for cellular therapy products [S6][S14]. Its ExtraVault biologic sample storage service represents strategic diversification targeting biopharmaceutical clients seeking cost-effective cold chain solutions [S22].

Legal Disputes Impacting Growth Prospects

A significant near-term challenge stems from arbitration involving Duke University following termination of a Patent and Technology License Agreement effective May 17, 2025. This agreement had been aimed at advancing novel treatments using umbilical cord stem cells for conditions such as cerebral palsy and autism through Celle Corp., a wholly owned subsidiary [S1][S6][S17][S21].

The arbitration scheduled for April 2026 has delayed expansion plans including clinical trials financing, biopharmaceutical manufacturing development, infusion clinic establishment, and related software enhancements [S6][S20][S21]. Capital expenditure plans related to this initiative have been suspended except for a limited comparability study capped at $350K [S20]. The timing and outcome remain uncertain.

Financial Condition and Liquidity Constraints

As of February 28, 2026, Cryo-Cell held cash and equivalents totaling approximately $249,672 against current liabilities near $17.76 million versus current assets around $11.08 million — reflecting liquidity stress with a current ratio roughly 0.62 [F1].

The company maintains financing arrangements including an amended revolving credit facility reduced to an $8 million commitment with maturity extended to October 18, 2027; term loans mature in July 2032 bearing interest rates indexed primarily to SOFR plus margins ranging from about 2.75% to 4.25% per annum [S4][S5]. Recent quarters involved repayments partially offset by drawdowns.

Operationally, FY2025 produced operating cash flow near $5.48 million while capital expenditures were controlled at approximately $230 thousand — substantially lower than prior years possibly due to suspended development projects amid legal uncertainties [F1].

Despite net losses, management continued dividend payments totaling about $3.23 million during FY2025 alongside modest share repurchases of roughly $169 thousand indicating commitment to shareholder returns within capital constraints [F1].

Competitive Positioning and Industry Context

Cryo-Cell competes against around twenty-five other U.S.-based private cord blood banks some possessing greater financial resources that may intensify competition especially for new customer acquisition through marketing investments [S16].

Its competitive advantages derive from proprietary processing technologies such as the PrepaCyte® CB system enhancing stem cell yield efficiency; extensive accreditation ensuring quality assurance; plus long-term specimen security capabilities providing consumer trust over decades-long storage horizons.

Regulatory oversight under FDA mandates requires compliance with evolving cGMP/cGTP standards which could increase operational complexities or costs if inspections reveal deficiencies. Cybersecurity remains an area of vigilance given sensitive healthcare data handling though direct HIPAA applicability is limited due to service nature [S6][S14][S15].

Future Outlook Considerations

No explicit forward-looking guidance has been provided amid prevailing uncertainties around ongoing litigation outcomes involving Duke University.

Potential upside catalysts include:

- Favorable resolution enabling advancement or spinout of Celle Corp.’s pipeline,

- Commercial traction for ExtraVault biologic sample storage targeting biopharmaceutical customers,

- Stabilized or growing core family-use processing/storage driven by marketing or pricing optimization,

- Expansion success or setbacks within international licensing agreements affecting royalty streams.

Conversely, downside risks remain elevated including unfavorable legal rulings potentially terminating therapeutic development plans permanently; regulatory changes increasing compliance burdens; emergent disruptive technologies diminishing relevance; or negative public perception impacting consumer demand.

Returns & Capital Allocation Summary Table

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | 5 | 0 | 0 | -704.2% |

| 2024 | 0 | 6 | 3 | 2 | +104.2% |

| 2023 | -10 | 9 | -12 | 7 | -443.6% |

| 2022 | 3 | 9 | 4 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 3 | 169502 | 5 |

| 2024 | 2 | 1423871 | 4 |

| 2023 | 0 | 799036 | 2 |

| 2022 | 8 | 1819915 | -4 |

Source: SEC companyfacts cache [F1].

Note: Figures rounded; operating income YoY compares FY2025 to FY2024; operating cash flow remains solid despite profit variability largely due to non-cash adjustments.

Conclusion

Cryo-Cell International continues as a foundational player anchored by its family-use umbilical cord blood banking business generating positive operational cash flows supporting dividend payments despite recent bottom-line pressures driven primarily by litigation with Duke University curtailing strategic regenerative medicine initiatives.

Liquidity constraints underscore the need for careful capital management given low cash reserves relative to short-term liabilities necessitating reliance on debt facilities while development projects are paused pending legal clarity.

Competitive strengths include proprietary technology platforms combined with accredited quality systems fostering customer retention but must be balanced against regulatory complexities alongside intellectual property disputes affecting growth outlook.

Investors should monitor developments related to the April arbitration ruling alongside progress on ExtraVault adoption and any updates regarding Celle Corp.'s potential spin-off or therapy commercialization as key milestones influencing future trajectory.

This analysis is based solely on publicly available SEC filings dated through April 14, 2026 without forward-looking investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments