DarkPulse, Inc. Revenue Growth Masks Deep Liquidity and Operational Struggles

Despite doubling service revenues in 2025, DarkPulse faces severe liquidity constraints and governance weaknesses.

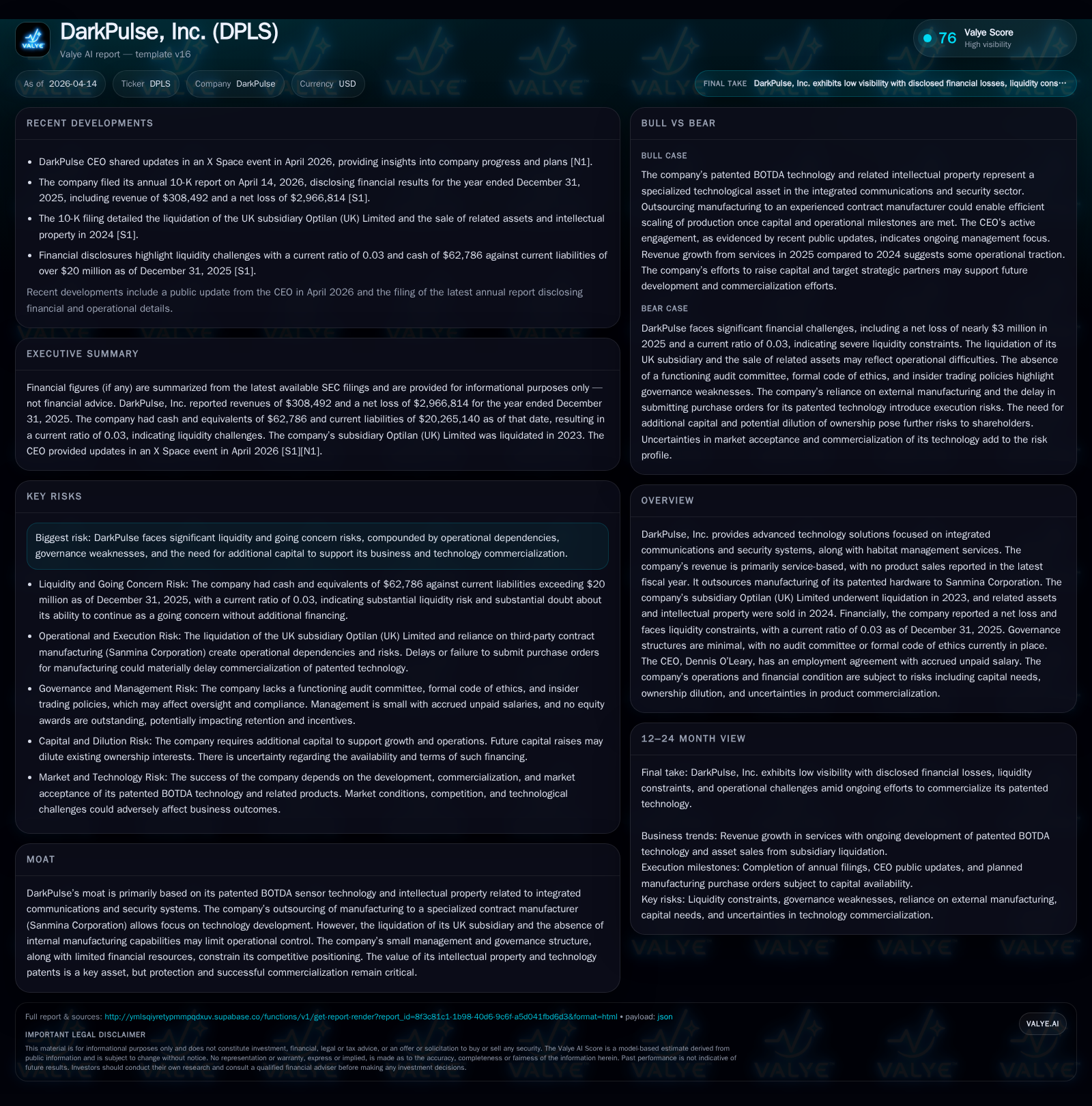

DarkPulse, Inc. reported a revenue increase of over 140% in 2025 driven by service contracts across North America and other regions; however, this growth masks persistent net losses exceeding $2.9 million and a critically low current ratio of 0.03 as of year-end 2025. The company’s business centers on its proprietary BOTDA sensor technology with outsourced manufacturing to Sanmina Corporation. Operational challenges include the liquidation of its UK subsidiary Optilan and ongoing unresolved legal judgments. Capital needs remain urgent amid accrued unpaid CEO compensation and governance shortcomings such as no audit committee or formal ethical policies.

Introduction

DarkPulse, Inc., a technology company specializing in integrated communications and security systems, experienced significant service revenue growth during fiscal year 2025. However, this financial progress contrasts sharply with ongoing liquidity stress, operating losses, and governance challenges detailed in its recent SEC filings [S1][F1]. This analysis reviews the company's historical financial performance, operational context, governance issues, legal risks, and outlook.

Historical Performance

DarkPulse reported consolidated revenues of $308,492 for FY2025, a 143% increase from $126,836 in FY2024, driven entirely by services with no product sales recorded in these periods [F1][S9]. Geographic revenue shifted notably with North America contributing $41,003 and the 'Rest of World' segment accounting for $267,489 in 2025 compared to prior UK concentration [S9].

Despite top-line growth, operating income remained negative at -$2.44 million in FY2025, a deterioration of nearly 30% from -$1.88 million in FY2024. Net losses narrowed somewhat to -$2.97 million but continue to reflect substantial operational expenses relative to revenue levels [F1]. Operating cash flow was negative $66,483 in 2025 versus a larger outflow previously, indicating some improvement though still insufficient for self-sustaining operations [F1]. Capital expenditures dropped to zero after prior years of spending reflecting potential cost management or asset divestitures post restructuring [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -3 | 0 | -2 | +143.2% | +23.6% |

| 2024 | 0 | -4 | -2 | -2 | +81.3% | |

| 2023 | -21 | -6 | -21 | +41.0% | ||

| 2022 | 9 | -35 | -22 | -35 | +16.9% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 0 |

| 2024 | -2 |

| 2023 | -6 |

| 2022 | -24 |

Source: SEC companyfacts cache [F1].

Note: All revenues were service-based; no product sales were reported [S9].

Business Model and Operations

DarkPulse centers its business on advanced technological solutions based on its proprietary Brillouin Optical Time Domain Analysis (BOTDA) sensor technology. Manufacturing operations are outsourced exclusively to Sanmina Corporation allowing the company to focus on intellectual property development rather than production infrastructure [S1].

A key operational challenge is the liquidation of Optilan (UK) Limited—formerly a wholly owned subsidiary involved in communications systems—that entered liquidation proceedings in mid-2023. DarkPulse holds unsecured creditor claims against Optilan amounting to approximately $19.4 million which represent material financial exposure [S1][S12].

In late 2024 DarkPulse acquired rights related to Optilan India PVT Ltd and Optilan Communication & Security Systems Ltd along with associated intellectual property for $65,000 USD as part of restructuring efforts aimed at regaining market foothold in India and Turkey [S16]. These acquisitions may provide strategic avenues but add integration complexity amid liquidity pressures.

Governance and Management

Governance structures reveal notable deficiencies: DarkPulse lacks an active audit committee and has not adopted a formal written code of ethics as of its latest filings; plans exist to implement such policies during fiscal year ending December 31, 2026 [S1]. The absence of insider trading policies further underscores governance gaps.

CEO Dennis O’Leary’s employment agreement stipulates an annual salary of $300,000 that has been fully accrued but remains unpaid as of December 31, 2025 illustrating cash flow constraints impacting executive compensation [S1][S11]. These factors raise concerns regarding internal controls and risk management practices.

Legal Proceedings

DarkPulse faces unresolved legal disputes including judgments against former creditors Carebourn Capital L.P. and More Capital LLC related to convertible promissory notes issued in prior years. Awards totaling approximately $799K plus attorney fees remain unsatisfied according to disclosures [S1]. These outstanding claims contribute additional financial uncertainty.

Other litigation involving FirstFire Global Opportunities Fund continues with mixed outcomes necessitating ongoing legal attention and resource allocation further stressing company finances [S21].

Future Growth Outlook

The company’s future growth depends heavily on successfully commercializing its BOTDA sensor technology alongside expanding integrated security system services within North American and international markets amid increasing competition from established players and startups alike [N1][S13].

Challenges include securing necessary capital for research and development cycles; navigating regulatory licensing requirements which could delay product offerings; managing competitive pricing pressures; and converting intellectual property into sustainable revenue streams.

Management is actively pursuing private placement financing targeting strategic partners to support product development commercialization efforts moving forward [N1][S16]. However, any capital raises may result in shareholder dilution given existing equity structures favoring preferred stockholders with disproportionate voting rights [S1].

Returns and Capital Allocation

Financial returns remain negative with net losses near $3 million alongside modestly negative operating cash flow ($66K) for FY2025 despite increased revenues [F1]. Capital expenditures declined sharply to zero indicating possible cost containment or asset sales following restructuring phases.

The current ratio stands at approximately 0.03 ($544K current assets versus roughly $20M current liabilities), signaling acute short-term liquidity risk requiring urgent recapitalization or operational restructuring for continued viability beyond twelve months absent new funding sources [F1][S16].

No dividends or share repurchases have been recorded given persistent losses and weak cash flows.

Conclusion

DarkPulse holds differentiated patented sensor technology forming the core competitive moat within integrated security solutions markets but faces significant hurdles including poor liquidity metrics, governance weaknesses including lack of audit oversight and formal ethical policies, unresolved legal liabilities from prior creditor disputes, and operational disruption due to subsidiary liquidation.

The company’s ability to achieve sustainable growth will rely on successfully raising additional capital alongside translating their patented technology into steady commercial revenues while managing competitive pressures and regulatory risks.

Investors should closely monitor forthcoming financial disclosures for updates on financing developments, contract wins or scaling partnerships that may improve cash flow profiles.

Disclaimer: This report is for informational purposes only. It does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments