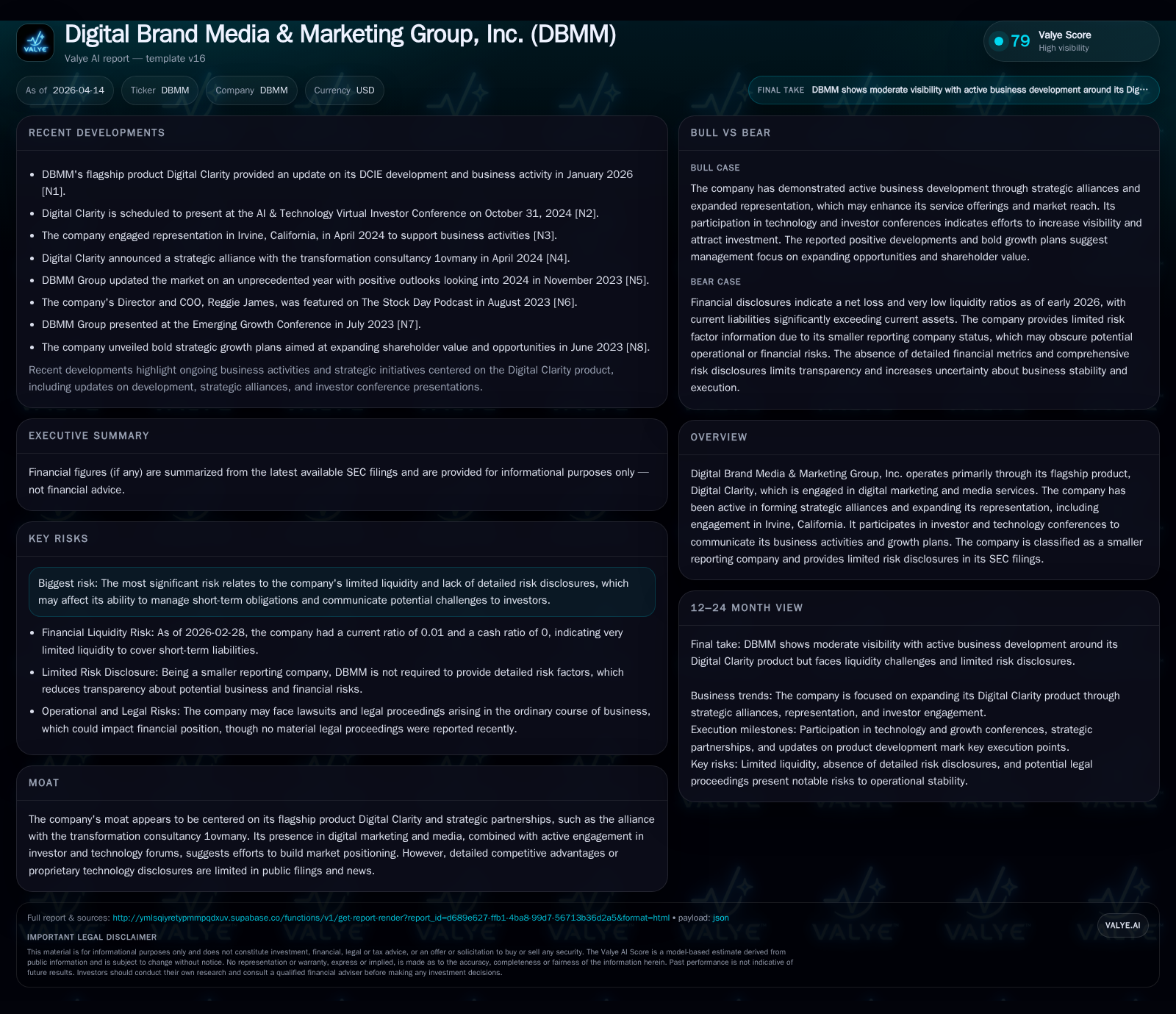

Digital Brand Media & Marketing Group’s Shrinking Revenue and Mounting Liabilities Spotlight Strategic Inflection

DBMM confronts steep revenue declines and severe liquidity constraints even as it seeks competitive footholds through strategic alliances.

Digital Brand Media & Marketing Group, Inc. (DBMM) has experienced a pronounced revenue contraction coupled with escalating operating losses over recent fiscal years, underscoring operational distress. The company's strategic partnerships, notably involving its flagship Digital Clarity platform and an alliance with transformation consultancy 1ovmany, signal attempts to stabilize market relevance amid financial headwinds. However, DBMM's balance sheet portrays acute liquidity stress marked by an alarmingly low current ratio and significant negative equity. Given the absence of explicit forward guidance, monitoring operational cash flows, partnership developments, and contract acquisitions will be central to assessing any pivotal turnaround.

Declining Revenues and Intensifying Losses Signal Operational Challenges

Digital Brand Media & Marketing Group's financial trajectory in recent years clearly illustrates a company under operational strain. Revenue contracted dramatically from $237,868 in FY2024 to $137,998 in FY2025—a near 42% year-over-year decline—reversing modest growth seen earlier between FY2022 and FY2023 [F1]. This reversal manifests despite ongoing efforts to develop market traction for their digital marketing services.

Operating income trends illustrate deepening challenges: the company reported an operating loss of $544,197 in FY2025 compared with $461,907 the prior year, representing an approximate 17.8% increase in operating deficit [F1]. Net losses also escalated slightly to over $1 million annually from FY2024 to FY2025 but have hovered in this range since FY2023 [F1]. Loss expansion outstripping revenue erosion indicates cost structures not scaling down with top-line contraction.

The persistence of negative operating cash flow compounds these operational difficulties; FY2025 saw cash outflows from operations near $537,108 while capital expenditures remained nil across all reported years, signaling no investment-driven offset or asset buildup [F1]. Such negative free cash flow pressures underscore reliance on external financing or capital injections to sustain ongoing operations.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 137998 | -1060220 | -537108 | -544197 | -42.0% | -1.4% |

| 2024 | 237868 | -1045142 | -569264 | -461907 | -23.2% | -46.6% |

| 2023 | 309644 | -713083 | -436785 | -414824 | +37.1% | -13.8% |

| 2022 | 225842 | -626428 | -389220 | -458472 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -537108 | 12.6 |

| 2024 | -569264 | 13.8 |

| 2023 | -436785 | 11.1 |

| 2022 | -389220 | 10.6 |

Source: SEC companyfacts cache [F1].

Table sourced from [F1] summarizing year-over-year changes highlighting contraction trends.

Strategic Partnerships as Anchor Points for Market Relevance

Despite financial headwinds, DBMM is anchoring its go-forward outlook on strategic partnerships and its core product offering — Digital Clarity. The company explicitly references building its consulting ecosystem through alliances such as with the transformation consultancy 1ovmany . This partnership ostensibly aims to blend digital marketing software capabilities with transformational advisory services typical of consultancy ecosystems targeting mid-market clients.

The notion of a "flagship product" centralizes competitive positioning around SaaS-like platform differentiation within digital marketing services. While detailed proprietary technology descriptions are absent in disclosures—limiting assessment—the alliance strategy can be understood as a bid to create synergies typical of combined platform-consultancy models seen increasingly in digital transformation sectors.

By participating actively in investor and technology forums located in hubs like Irvine, California , DBMM signals intent to amplify visibility among tech-savvy stakeholders and potential enterprise customers.

Balance Sheet Constraints Highlight Liquidity Risks

DBMM's balance sheet reveals acute financial stress characterized by extreme liquidity imbalances. Current liabilities ballooned to approximately $8.97 million by early 2026 compared to current assets totaling roughly $58.5K—a current ratio near an alarming 0.01 reflective of severe short-term solvency risk [F1].

This mismatch portrays an inability of liquid assets to cover immediate obligations by over two orders of magnitude according to widely adopted capital markets metrics for operational resilience.

Simultaneously, shareholder equity is deeply negative at around $-8.38 million as of FY2025-end [F1], demonstrating ongoing erosion of net asset values likely accelerated by accumulated losses and deferred liabilities or obligations. This level of negative equity typically limits access to conventional credit avenues absent robust turnaround plans or external capital injections.

Such conditions place operational sustainability under threat unless liquidity management improves markedly or fresh financing sources materialize promptly.

What Analysts Should Watch: Potential Catalysts and Lingering Uncertainties

With no explicit forward earnings or revenue guidance disclosed in SEC filings or news releases , buy-side analysts must track several key inflection points closely:

- Contract Wins: Success securing new service agreements leveraging Digital Clarity and consultancy alliances would indicate traction toward reversing revenue slide.

- Liquidity Management: Signs of balance sheet repair such as renegotiated payables or fresh equity/private financing could mitigate solvency fears.

- Partnership Developments: Expansion or deepening integration with entities like 1ovmany might augment service offerings and diversify revenue streams.

- Operational Cash Flow Improvement: Moving toward positive operating cash generation would signify meaningful progress reducing dependency on external funding.

Absent these developments—increased transparency around risks also remains crucial given currently constrained disclosure norms as a smaller reporting company.

Capital Allocation Overview Amid Financial Pressure

DBMM has not reported dividends or share repurchase activity consistent with constrained capital allocation capacity amid ongoing financial pressure as reflected in publicly available filings [F1]. The company’s persistent operating losses and negative free cash flow (~$537K in FY2025) indicate that resources are primarily directed toward sustaining operations rather than shareholder returns or expansion investments.

This pattern aligns with a company navigating survival mode under significant distress without evident capacity for discretionary capital deployment.

Risk Factors Under Limited Disclosure Framework

DBMM benefits from regulatory accommodations granted smaller reporting companies that exempt it from furnishing comprehensive risk factor disclosures under Item 1A of Regulation S-K [S1][S2][S4][S5]. While the company reports no active litigation at filing dates [S1][S3], it notes standard business risk language cautioning that unpredicted adverse outcomes could occur from legal controversies routinely encountered.

This limited risk narrative hinders thorough institutional risk assessment since granular details on credit exposures, counterparty concentrations or contingent liabilities remain opaque, likely elevating perceived uncertainty among sophisticated investors requiring full transparency for valuation confidence.

Disclaimer: This report is based exclusively on publicly available SEC filings ([F1],[S#]) and company-extracted summaries (). It does not constitute investment advice or recommendations but aims solely at presenting factual analysis grounded in disclosed material.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments