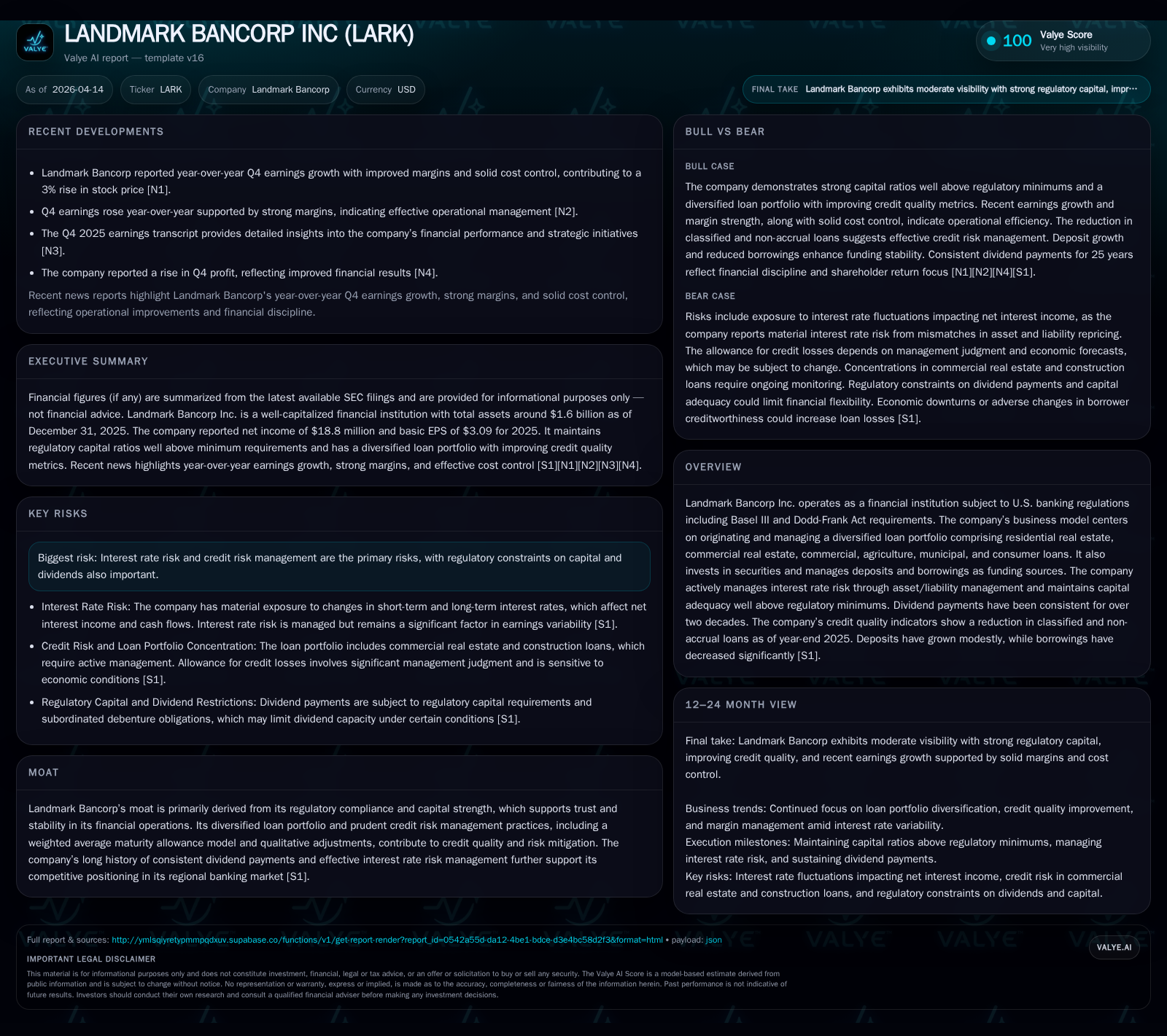

Landmark Bancorp Inc: Earnings Surge Fuels Confidence as Capital Strength Remains Firm

Robust net income growth paired with disciplined credit risk and strong capital ratios underpin Landmark Bancorp’s financial resilience.

Landmark Bancorp Inc. recorded a significant 44.4% increase in net income for fiscal year 2025, propelled by disciplined credit risk management and net interest income expansion. The bank maintains capital adequacy well above Basel III minimums, including a total risk-based capital ratio of 13.96%, underscoring its stability amid regulatory demands. Consistent dividend payments continue, supported by prudent cash flow generation and controlled expenditures, while borrowings have notably declined against steady deposit growth, reflecting enhanced liquidity management. The company’s diversified loan portfolio and stringent asset/liability controls provide a solid foundation for ongoing profitability within a regulated banking framework.

Growth Trajectory: Evolution of Profitability and Loan Portfolio Composition

Landmark Bancorp Inc.'s financial performance in recent years has been characterized by compelling profitability gains alongside strategic loan portfolio management. Net income jumped from $13 million in FY2024 to approximately $18.8 million in FY2025, representing a robust 44.4% year-over-year increase based on companyfacts data [F1]. This marked net income surge was primarily attributed to expansion in net interest income linked to higher asset yields and effective pricing across a diversified loan portfolio.

The bank’s lending activities encompass residential real estate (one-to-four family homes), commercial real estate (CRE), commercial loans, agriculture lending, municipal financing, and consumer loans as core revenue drivers [S1]. During FY2025, gross loans grew roughly 5.7%, rising to about $1.1 billion against the prior year [S11], bolstered by demand within its regional markets despite competitive pressures.

Deposit levels grew modestly from approximately $1.3 billion in FY2024 to $1.4 billion in FY2025, providing stable funding for loan growth [S22]. Importantly, total borrowings contracted significantly by approximately 61.9%, falling from around $88.5 million at end-2024 to $33.7 million at end-2025 due to both deposit inflows and strategic reduction in reliance on external debt sources [S22]. Investment securities available-for-sale declined 6.5% during the same period as market repositioning optimized the balance sheet mix.

Operating expenses excluded from interest cost remain focused on compensation, occupancy, IT systems (notably data processing), professional fees, amortization of intangibles, along with federal deposit insurance costs — all contributing factors monitored closely against earnings growth [S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 19 | 22 | 1 | +44.4% |

| 2024 | 13 | 14 | 2 | +6.3% |

| 2023 | 12 | 13 | 1 | +23.9% |

| 2022 | 10 | 25 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 5 | 338000 | 21 |

| 2024 | 5 | 338000 | 12 |

| 2023 | 4 | 75000 | 12 |

| 2022 | 4 | 1239000 | 24 |

Source: SEC companyfacts cache [F1].

Note: Capex decline driven by completion of system upgrades completed prior years.

Rigorous Credit Risk Management Amid Interest Rate Variability

Since its January 2023 adoption of the Current Expected Credit Loss (CECL) accounting standard for loan loss provisioning, Landmark Bancorp has refined its allowance methodology reflecting expected losses rather than incurred losses under legacy standards [S1]. This shift integrates forward-looking economic forecasts evaluated quarterly alongside historical loss experience.

The allowance for credit losses on loans declined slightly as a percentage of gross loans from about 1.22% at December 31, 2024 to 1.12% at December 31, 2025; numerically dropping from approximately $12.8 million to $12.5 million consistent with improved asset quality metrics including reduced problem loans [S11]. Classified loans — encompassing ‘special mention,’ ‘substandard,’ or ‘doubtful’ categories — decreased from roughly $26 million in late-2024 to approximately $23 million by end-2025 largely driven by one commercial loan charge-off during the year.

Non-accrual loans also diminished from about $13 million or 1.25% of gross loans to roughly $10 million or 0.90%, strengthening overall loan quality profiles [S11][S22]. Loans past due between thirty to eighty-nine days similarly improved both nominally and as a percentage of portfolio.

Landmark Bancorp employs sector-specific risk modeling techniques applying sales comparison approaches with qualitative adjustments ranging between zero up to fifty percent on collateral values depending on loan type — particularly for commercial real estate where valuation sensitivities are most pronounced [S16]. Such detailed diligence supports provisioning accuracy under uncertain inflationary and economic conditions impacting borrower repayment capacity.

Capital Adequacy Above Regulatory Thresholds: Implications for Stability and Growth

Landmark Bancorp’s capital base remains a pillar of its competitive moat within regional banking markets underscored by robust adherence to Basel III regulatory frameworks as implemented through U.S.-specific Dodd-Frank Act mandates [S1][S4]. As of December 31, 2025:

- Total risk-based capital ratio stood at 13.96%, well above the minimum threshold of 10.50% including conservation buffers.

- The leverage ratio was healthy at 9.67%, exceeding the required minimum of 4%.

- Common Equity Tier One (CET1) capital reached 12.92%, surpassing the regulatory floor of 7%.

A significant component of Tier One Capital includes approximately $21.7 million in trust preferred securities issued via wholly owned grantor trusts structured to issue preferred interests backed by subordinated debentures carrying variable rates tied to three-month CME SOFR plus contractual margins ranging between roughly 1%-3% depending on issuance series; these instruments are redeemable starting mid-2030s but contribute positively towards capital adequacy classification [S6][S9][S12][S24].

Such resilient capitalization affords the bank substantial freedom for organic growth investments while maintaining compliance with prompt corrective action requirements that limit activities if undercapitalized; Landmark remains comfortably “well-capitalized” per regulatory definitions.

Dividend Policy: Sustaining Shareholder Returns Through Economic Cycles

Continuity marks Landmark Bancorp’s dividend policy which has paid uninterrupted quarterly dividends for more than twenty-five consecutive years culminating in a consistent payout rate of approximately $0.20 per share during FY2025 compared with $0.19 per share the prior year adjusted for stock dividends [F1][S1].

Total dividend distributions increased slightly year-over-year reaching nearly $4.86 million matching rises in net income while maintaining prudent payout ratios relative to retained earnings.

Regulatory constraints mandate that dividend payments must not reduce capital below adequacy thresholds; Landmark reports available distributable reserves amounting up to roughly $3 million without requiring OCC approval as of end-2025 which aligns dividends sustainably within internal capital projections balancing growth needs versus shareholder returns [S4][S14].

Free cash flow generation estimates derived by subtracting capex from operating cash flows yield approximately $21 million excess cash annually signifying ample liquidity coverage supporting dividends plus reinvestments without excessive leverage build-up [F1].

Leverage and Liquidity Position: Analysis of Borrowings, Deposits, and Off-Balance Sheet Risks

In line with increased deposits driving funding capacity upwards modestly (to ~$1.4 billion end-2025), Landmark aggressively reduced borrowings nearly two-thirds since end-2024 down to approximately $33 million primarily via principal repayments on fixed-rate facilities coupled with investment security sales optimizing balance sheet risk-return profiles [S22][S7].

Borrowings include subordinated debentures issued historically through grantor trusts entailing variable coupon resets tied to SOFR benchmarks plus embedded spreads ranging typically around +0.26%, further anchoring flexible liability cost structures aligned with interest rate environments prevailing near-end periods [S5][S6][S9]. The line of credit balance stood minimal or nil given covenant compliance while liquidity is bolstered through Federal Home Loan Bank advances capacity totaling more than $239 million collateralized yet largely undrawn providing contingent funding buffers [S7][S11].

Deposit mix is diversified across non-interest bearing accounts (26%), money market/checking (47%), savings accounts (11%), and certificates of deposit (16%) offering stable low-cost funding benefiting asset-liability management (ALM) processes aiming at minimizing interest rate risk exposure amidst evolving rate cycles common in regional banking sectors [S22][S25].

Off-balance sheet commitments principally include standby letters of credit amounting around $2.2 million—secured typically against CRE properties and other collateral types—subjected internally to rigorous credit underwriting policies paralleling those applied for direct lending exposures providing mitigants against contingent liabilities materializing unexpectedly [S7][S8].

Active monitoring using multiple interest rate simulation scenarios—capturing twists in yield curves plus basis risks—and dynamic repricing models enhance sensitivity analyses around net interest margin volatility shaping pricing strategies across assets/liabilities segments balanced against customer behavior estimates under changing monetary circumstances [S26].

Outlook and Return Expectations: Balancing Expansion Against Regulatory Constraints

While Landmark Bancorp’s latest results showcase solid momentum reflected through earnings acceleration alongside disciplined credit management underpinning sound asset quality trends, future growth will likely balance between organic loan book expansion within core regional markets against supervisory capital adequacy ceilings limiting rapid payout expansions or aggressive buyback programs .

Absent explicit updated guidance disclosures post-FY25 filings,[N* unavailable] investors should monitor evolving metrics such as:

- Sustained low levels or further improvements in classified/non-accrual loan proportions indicating ongoing asset quality strength.

- Stability or modest increases in net interest margins signaling effective asset repricing vis-à-vis liabilities funding costs amid interbank rate variability.

- Capital ratios holding comfortably above regulatory minimums ensuring no constraints impeding dividend policies or enabling measured strategic acquisitions/expansions.

- Quarterly reports confirming controlled operating expense growth relative to revenue expansions maintaining efficiency ratios supportive of ROE improvement.

Current modest repurchase activity (circa $0.34 million annually)[F1] despite meaningful free cash flow reflects balance sheet conservatism prioritizing capital buffer maintenance over aggressive share buybacks amid prevailing economic uncertainty factors impacting broader financial institutions.

In conclusion, Landmark Bancorp’s demonstrated capacity for profitable growth rooted deeply in risk-sensitive underwriting processes combined with strong capital positions engenders confidence in its steady-state business model geared toward long-term resilience within a highly regulated environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments