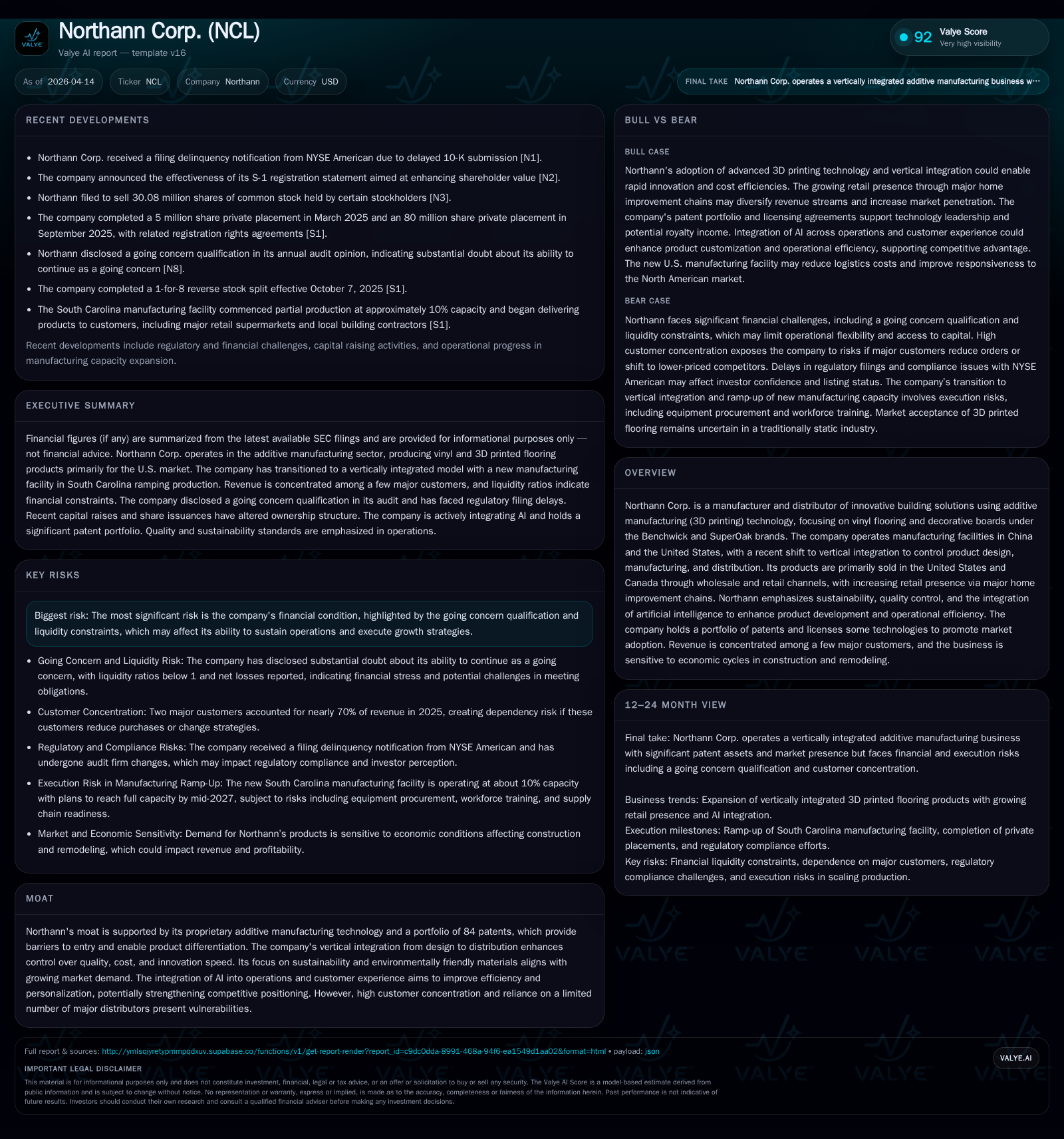

Northann Corp. Confronts Liquidity Stress While Advancing Vertical Integration and Retail Expansion

Innovative 3D printing solutions bolster Northann’s niche in vinyl flooring amid mounting financial and operational risks.

Northann Corp. has demonstrated revenue growth with a nearly 10% increase in 2024 driven by expansion of its proprietary 3D printed vinyl flooring products, particularly the SuperOak line gaining traction in U.S. retail chains. The company’s strategic pivot toward vertical integration and domestic manufacturing in South Carolina aims to shorten delivery times and control product quality but currently operates at limited scale. Financially, persistent net losses and negative operating cash flows underscore significant liquidity concerns, including a going concern qualification. Share issuances to support advisory agreements and asset purchases indicate reliance on equity capital to fund operations and strategic initiatives.

Historical Financial Performance

Northann Corp.'s revenue rose from approximately $13.97 million in FY2023 to $15.35 million in FY2024, representing a 9.9% increase supported by expanded wholesale and retail sales primarily in North America [F1]. Retail sales notably increased from a negligible share (0.19%) of total revenue in FY2024 to over 7% in FY2025, reflecting growing presence through major home improvement retailers [S13].

Profitability remains challenged; operating losses narrowed from -$4.76 million in FY2023 to -$1.67 million in FY2024 [F1], while net losses improved from -$7.13 million to -$4.38 million over the same period [F1]. Operating cash flow remained negative but improved significantly year-over-year (-$1.23 million vs -$4.68 million) indicating some stabilization [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2024 | 15 | -4 | -1 | -2 | +9.9% | +38.6% |

| 2023 | 14 | -7 | -5 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | -168.5 |

| 2023 | -1224.2 |

Source: SEC companyfacts cache [F1].

Equity increased modestly from $0.58 million in FY2023 to $2.6 million in FY2024, reflecting capital infusions during this period [F1]. Despite improved results, losses persist consistent with investment into product development, market expansion, and vertical integration transition costs.

Business Model and Industry Positioning

Northann leverages additive manufacturing (3D printing) for vinyl flooring production under Benchwick and premium SuperOak brands [S7][S26]. Manufacturing occurs primarily at a Chinese facility equipped with 88 proprietary printers capable of producing nearly 20,000 square meters daily, alongside a new South Carolina facility operating at about 10% capacity as part of vertical integration efforts targeting full capacity by mid-2027 [S7][S8].

Vertical integration aims to accelerate innovation cycles and reduce logistics costs by consolidating design, manufacturing, and distribution domestically [S8][S26]. Additive manufacturing supports sustainability by reducing material waste up to 40% and energy consumption over 50% compared to traditional methods [S26].

The company maintains a portfolio of roughly 84 granted or pending patents supporting proprietary technology; some are licensed externally to encourage broader adoption [S7][S11][S13]. Competitive advantages include infinite pattern customization enabled by AI-driven algorithms, rigorous quality control certified under FloorScore and ISO standards, and recognized sustainability initiatives such as Greenstep nominations for ocean-reclaimed plastic innovations [S11][S19].

Customer Concentration and Market Channels

Two major wholesale distributors accounted for nearly 70% of revenues in FY2025, down slightly from about 77% in FY2024, presenting concentration risk if these customers shift purchasing approaches [S5][S6][S13].

Distribution remains predominantly wholesale (93%) but retail sales have grown (7%), driven by online storefront Dotfloor.com and agreements with large home improvement chains aiming at revenue diversification [S7][S13].

Geographically, over 99% of revenue derives from North America—mostly the U.S.—with minimal exposure (<1%) outside this region [S4][S13]. This concentration exposes the company to trade policy risks affecting imports from China where much raw material sourcing occurs [S10][S23].

Supply Chain Considerations

Key raw materials include UV ink imported mainly from Japan, coatings and resins sourced largely from China, sound padding, and glue essential for the additive manufacturing process [S6]. Two suppliers accounted for approximately 44% of total cost of goods sold during the latest fiscal year, highlighting supplier concentration risk [S12].

Efforts toward diversification include expanding sourcing into Southeast Asia (Vietnam, Thailand) to mitigate tariff impacts and pandemic-related supply disruptions [S12][S23][S26]. However, dependence on global petrochemical derivatives introduces potential margin pressure if costs rise without ability to pass through price increases.

Capital Structure and Liquidity Profile

As of September 30, 2025, Northann's current liabilities ($9M) exceeded current assets ($6.57M), resulting in a current ratio around 0.73 indicative of short-term liquidity stress [F1]. Cash on hand was minimal at roughly $40k at that time [F1]. These factors contributed to a going concern qualification disclosed in the latest annual report highlighting operational viability uncertainties absent capital raises or rapid profitable scaling [S1][S19].

To fund growth initiatives including plant ramp-up and supply chain improvements, the company has issued shares tied to consulting agreements compensating advisors through stock issuance alongside strategic asset acquisitions [S16][S18][S24]. There are no declared dividends or share repurchase programs reflecting prioritization of reinvestment amid constrained cash flow ([F1],[S14],[S20]).

Outlook Considerations

Key growth drivers include:

- Achieving full operational capacity at the South Carolina facility by mid-2027 aiming for reduced logistics costs and improved delivery times.

- Expanding retail penetration via vendor agreements with major U.S.-based home improvement retailers.

- Leveraging AI tools for enhanced product customization improving consumer experience.

- Continuing R&D backed by extensive patent holdings introducing innovative vinyl flooring products balancing durability with aesthetics.

Risks include:

- High customer concentration risking revenue volatility if major partners alter purchasing behavior.

- Integration challenges associated with scaling new domestic production facilities.

- Cyclical construction market dynamics affecting demand.

- Raw material cost inflation or supply disruptions constraining margins.

- Trade policy uncertainties impacting cross-border sourcing.

- Persistent liquidity constraints necessitating capital raises potentially dilutive to shareholders.

Milestones such as reaching full-capacity production domestically within planned timelines alongside retail revenue growth will be critical indicators of execution success.

Returns and Capital Allocation Summary

Return on equity remains deeply negative at approximately -168%, reflecting recurring net losses relative to modest equity base [F1]. Operating cash flows remain negative though improved year-over-year signaling gradual operational stabilization but no free cash generation yet [F1].

Capital allocation focuses on equity issuance funding strategic initiatives including consultant compensation via stock awards as well as investments into technology development; no shareholder distributions have been made given financial constraints ([S14],[S16],[S24],[F1]).

Conclusion

Northann Corp.'s innovative additive manufacturing approach coupled with sustainability commitments differentiates it within a mature flooring industry dominated by conventional producers. Its patent portfolio underpins defensible technology moats while vertical integration offers potential long-term efficiencies.

However, financial strain marked by ongoing losses alongside critical liquidity challenges poses execution risks requiring close monitoring of production ramp-up progress and retail channel expansion effectiveness.

Customer concentration further underscores need for continued diversification efforts.

Investors should watch milestones around domestic facility scaling and retail growth as key barometers validating Northann's transformation strategy going forward.

This analysis is based solely on publicly available SEC filings through April 14, 2026 ([F1], [S#]) without speculative forecasts or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments