SemiLEDs Corp Navigates Rapid Revenue Growth Amid Ongoing Losses and Capital Challenges

An in-depth look at SemiLEDs’ remarkable revenue expansion alongside persistent operating losses, liquidity constraints, and evolving debt arrangements within a complex LED industry IP framework.

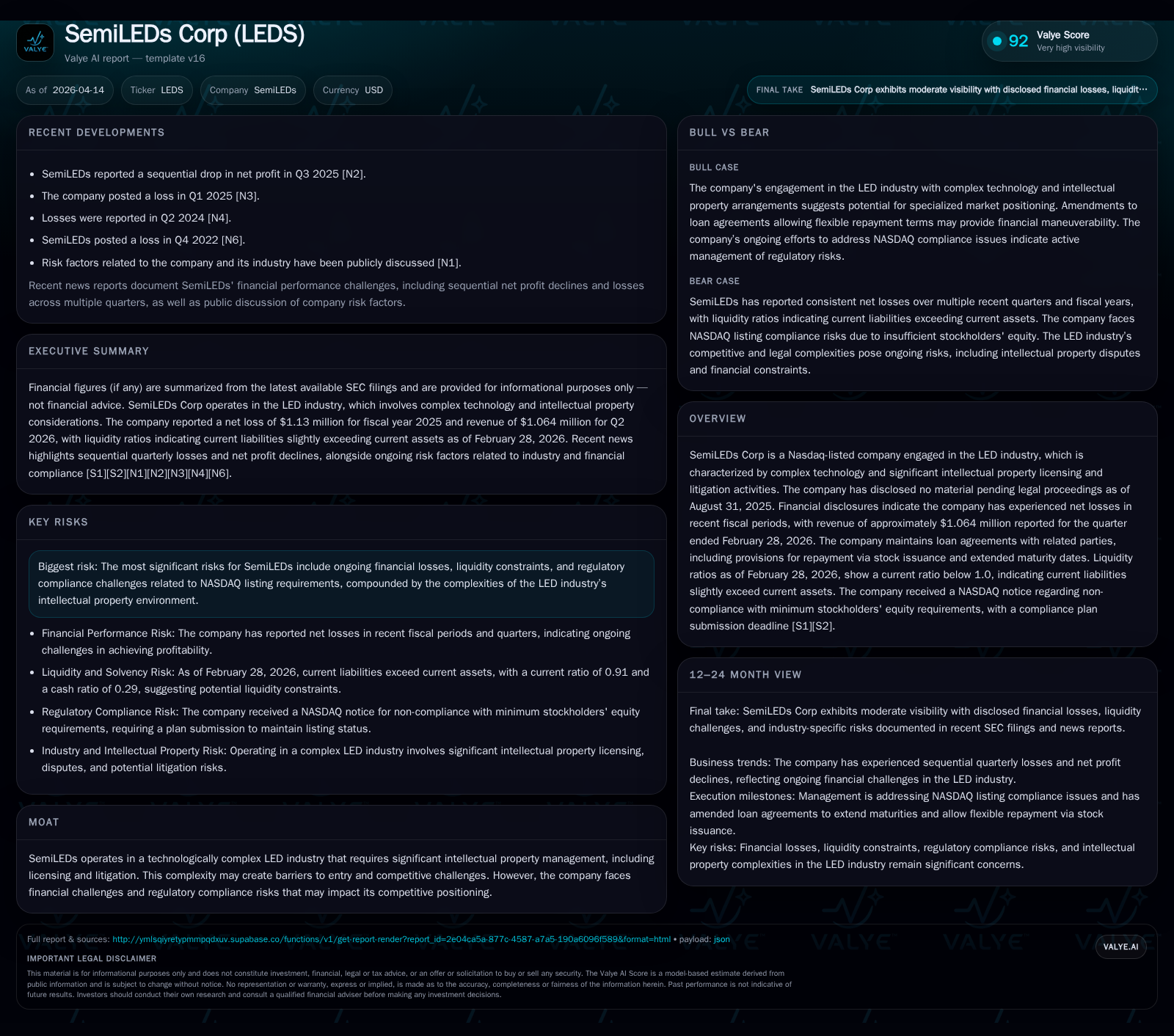

SemiLEDs Corporation reported a substantial revenue increase from $5.18 million in FY2024 to $43.0 million in FY2025, an approximate 730% year-over-year rise [F1]. Despite this growth, the company continues to operate at a loss with operating income at -$1.60 million and net income at -$1.13 million for FY2025, though both show improvement from prior years [F1]. Liquidity pressures persist with a current ratio below 1 as of February 28, 2026 [F1], compounded by NASDAQ listing compliance challenges due to insufficient stockholders’ equity [N1][S15]. SemiLEDs manages capital structure via secured loans from related parties extended through January 15, 2027, featuring provisions for partial repayment through common stock issuance [S7][S11]. The firm operates in a technology-intensive LED sector with ongoing intellectual property negotiations but no material litigation as of August 31, 2025 [S1][S4].

Historical Financial Performance: Accelerated Revenue Growth during Continued Losses

SemiLEDs Corporation experienced extraordinary revenue growth from $5.18 million in FY2024 to $43.0 million in FY2025—a nearly 730% increase year-over-year—demonstrating significant expansion within its market niche in the LED industry [F1]. Despite this surge, the company has not yet achieved profitability; operating income remained negative at -$1.60 million in FY2025 but improved compared to -$2.95 million the prior year. Net income losses similarly narrowed to -$1.13 million from -$2.04 million over the same period [F1].

The improvement suggests enhanced operational leverage as fixed costs are absorbed by higher revenues; nonetheless, ongoing investments likely necessary for R&D and sales efforts continue to weigh on margins.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 43 | -1 | 2 | -2 | +729.8% | +44.5% |

| 2024 | 5 | -2 | 0 | -3 | -13.3% | +24.3% |

| 2023 | 6 | -3 | -1 | -3 | -15.2% | +2.0% |

| 2022 | 7 | -3 | -2 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 1643000 | -40.6 |

| 2024 | -488000 | -92.5 |

| 2023 | -1184000 | -233.7 |

| 2022 | -1788000 | -79.5 |

Source: SEC companyfacts cache [F1].

Source: SEC filings and company financial disclosures [F1]

Intellectual Property Landscape: Competitive Moat during Industry Complexity

Operating within the LED industry entails navigating complex intellectual property rights involving patents on semiconductor structures and manufacturing processes essential for performance improvements [S1]. While SemiLEDs reported no material pending litigation as of August 31, 2025, it operates amid frequent licensing negotiations and potential disputes typical of this technology-intensive sector [S4]. This environment can serve as both a competitive moat and a source of risk affecting margins and commercialization strategies.

Liquidity Position and Capital Structure: Loan Amendments Reflect Ongoing Challenges

As of February 28, 2026, SemiLEDs held cash and equivalents of approximately $3.98 million against current liabilities of $13.64 million resulting in a current ratio near 0.91—a sign of tight liquidity conditions [F1]. Since January 2019, the company has engaged in secured loan agreements totaling around $3.2 million with related parties including its Chairman and largest shareholder bearing an annual interest rate near 8% [S7][S8]. These loans have undergone multiple amendments extending maturity dates through January 15, 2027.

Crucially, amendments permit repayment of portions of principal or accrued interest via issuance of common stock up to specified limits—providing flexibility but also raising potential equity dilution concerns for shareholders [S7][S11][S12]. This reflects an effort to manage debt obligations amid constrained cash flow.

NASDAQ Compliance Notice: Stockholders’ Equity Deficit and Response

On January 30, 2026, NASDAQ issued a notice that SemiLEDs did not meet the minimum stockholders’ equity requirement of $2.5 million under Listing Rule 5550(b)(1), triggering compliance deadlines and heightened scrutiny [N1][S15]. As of fiscal year-end August 31, 2025, book equity stood at approximately $2.78 million but was pressured by cumulative losses over prior periods [F1]. The company has submitted a compliance plan aiming to regain adherence within prescribed timeframes.

Outlook: Growth Hinges on IP Management and Financial Stability

While SemiLEDs’ rapid revenue growth signals market opportunity capture within specialized LED applications, sustained profitability depends on successfully managing intellectual property complexities without protracted disputes that could hinder commercialization efforts [N1][S2][S5]. Additionally, liquidity constraints and equity deficits present material risks requiring careful capital allocation and operational execution.

Capital Allocation Trends: Positive Operating Cash Flow Supports Measured Investment

FY2025 marked a return to positive operating cash flow at $2.21 million following several years of negative cash generation—a key indicator of improving underlying business dynamics despite net losses continuing [F1]. Capital expenditures increased moderately to $569 thousand consistent with cautious investment aligned with financial capacity.

Return on equity remains deeply negative at approximately -40%, reflecting net losses relative to a diminished equity base impacted by accumulated deficits over previous years [F1]. Free cash flow calculated as operating cash flow minus capex was positive at roughly $1.64 million for FY2025.

Key Developments to Monitor

- Extension of loan maturities through January 15, 2027 provides temporary relief but necessitates refinancing or repayment planning amid ongoing cash constraints [S11]

- Progress on NASDAQ compliance plan approval critical for maintaining listing status and access to public capital markets [N1][S15]

- Absence of material new litigation noted but ongoing IP licensing landscape demands vigilant risk management given potential impact on operations and margins [S4]

- Quarterly updates on revenue trends versus cost control measures will be essential indicators for sustainable profitability transition.

This report integrates publicly filed SEC documents through April 14, 2026 along with Nasdaq commentary without speculative forecasts or opinion.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments