Legato Merger Corp. III’s Transition Strategy: Unlocking Value Through Einride Merger

Legato Merger Corp. III approaches a pivotal transition from SPAC to operating company through its merger with Swedish tech firm Einride AB, navigating financial strengths and inherent execution risks.

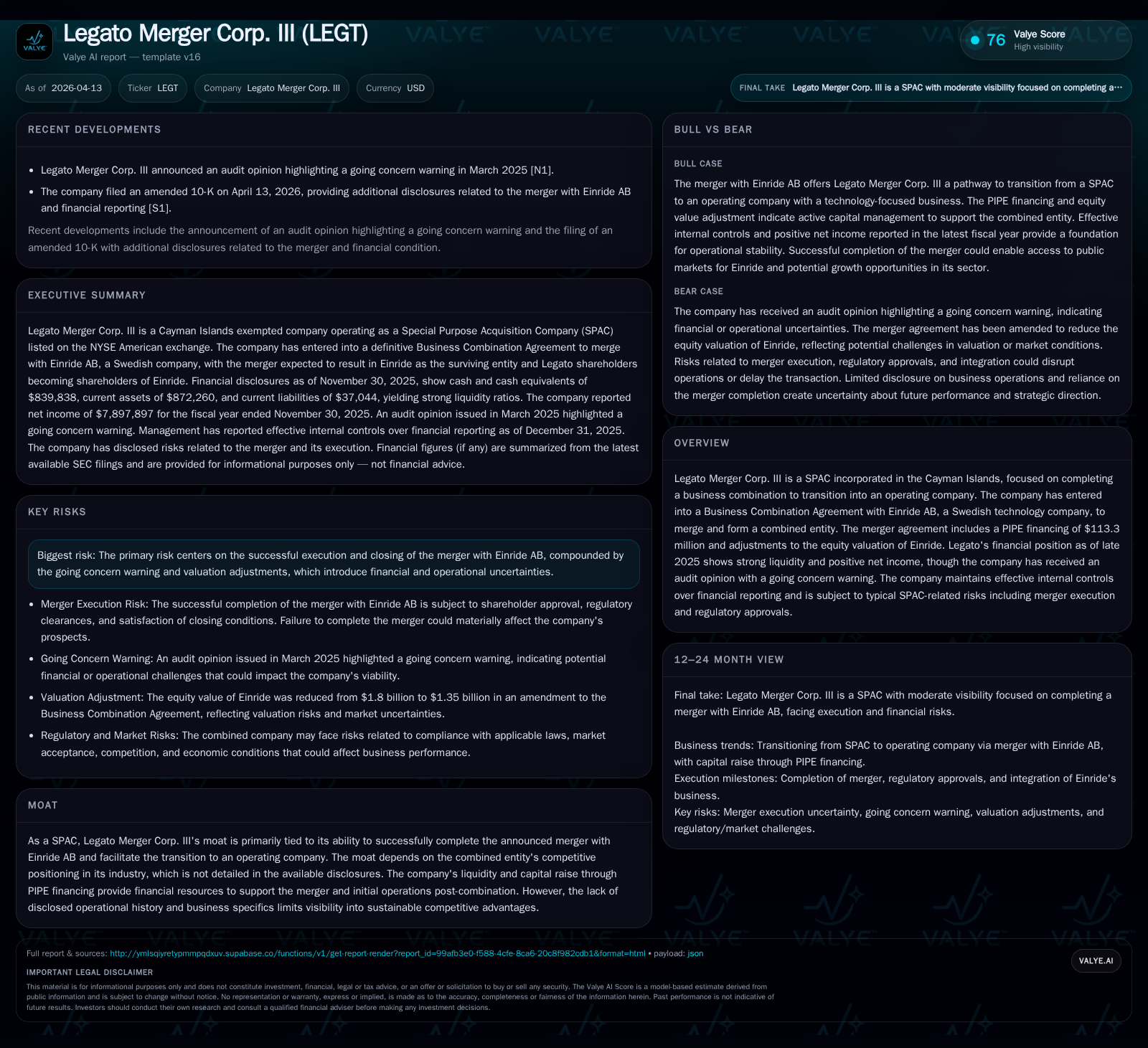

Legato Merger Corp. III, a Cayman Islands-based SPAC, has committed to transforming into a full-fledged operating entity by merging with Einride AB, a technology company based in Sweden. The merger involves significant PIPE financing and equity valuation adjustments reflective of market realities. Legato’s historical financials show typical SPAC characteristics including negative operating income offset by non-operating gains, solid liquidity supported by trust account balances, but negative equity and a going concern audit warning signal caution. Execution risks primarily cluster around successful merger close and regulatory approvals. Post-merger growth potential hinges on Einride's technological positioning amid limited disclosed operational metrics.

Historical Financial Performance and Operational Track Record

Legato Merger Corp. III’s fiscal year ending November 30, 2025 reveals quintessential SPAC financial traits characterized by absence of traditional revenue generation hinged upon pre-merger status [F1]. Operating income fell significantly to -$1.04 million in FY2025 from -$0.67 million in FY2024, registering a steep decline of approximately 54.9%. This drop underscores increased spending typical of SPAC maintenance costs ahead of a business combination.

In contrast, net income remained positive at nearly $7.9 million—down marginally by about 3.9% year-over-year—primarily propelled by non-operating gains such as mark-to-market adjustments or interest income from trust account investments rather than operational profitability [F1]. Meanwhile, operating cash flow improved slightly from negative $844k to negative $786k (a 6.9% enhancement), signifying tighter cash expenditure control even amid ongoing transactional activities [F1].

The company's balance sheet highlights strong short-term liquidity with current assets measured at approximately $872k dwarfing current liabilities at about $37k as of the last reported period–producing an anomalously high current ratio of 23.55 that reflects trust fund conservatism rather than operating asset optimization [F1]. However, negative shareholders’ equity close to -$6.1 million signals accumulated losses and redemption liabilities common in post-IPO SPACs yet to complete their target acquisition [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 8 | -785914 | -1038758 | -3.9% |

| 2024 | 8 | -844493 | -670426 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -130.0 |

| 2024 | -161.2 |

Source: SEC companyfacts cache [F1].

Key Drivers Behind Legato’s Pre-Merger Financials

The negative operating income juxtaposed with positive net income results from the structural nature of SPACs where expenses mainly stem from administrative upkeep and merger-related costs without corresponding operating revenues [F1][S1]. Typical outlays include legal fees for deal negotiations, regulatory compliance expenses especially linked to SEC filings and proxy assists, as well as costs related to maintaining listing standards.

Non-operating items such as interest earned on cash held in trust accounts or investment gains bolster net income figures during this phase since actual operational business activities have yet to commence [F1][S1]. Consequently, despite bottom-line profitability as reported under GAAP accounting conventions, the underlying business remains loss-making per operational metrics prior to the combination event.

Overview of the Business Combination with Einride AB

On November 12, 2025 Legato entered into a definitive Business Combination Agreement with Einride AB—a Swedish technology enterprise specializing presumably in transport automation solutions though exact industry positioning is not elaborated in disclosures [N/A meta][S3][S4]. The transaction entails the merger of Legato with a wholly-owned subsidiary of Einride whereby post-closing shareholders of Legato will become shareholders in the combined corporate entity.

A PIPE financing component accompanies this deal totaling approximately $113.3 million raised from accredited investors contemporaneous with the merger close [N/A meta][S6]. Notably, an amendment dated February 26, 2026 reduced Einride’s agreed equity valuation significantly from $1.8 billion to $1.35 billion—a roughly 25% haircut reflecting market valuations or updated due diligence results [S6]. This adjustment introduces transactional valuation risk impacting potential upside for pre-merger shareholders.

Capital Structure and Liquidity Position Heading into the Merger

Legato holds cash and equivalents around $840k as per latest fiscal data alongside current assets near $872k versus comparatively negligible current liabilities approximating $37k resulting in an exceptionally healthy current ratio of about 23.55 [F1][S21][S26]. This stems mostly from funds held in trust accounts pending transaction completion—typical for blank-check companies.

Capital structure includes ordinary shares outstanding (~25.8 million shares as of February 10, 2026) along with units combining ordinary shares and redeemable warrants exercisable at about $11.50 per share post-combination [S21]. These warrants entail price reset clauses triggered if securities trade below pre-specified thresholds six months after registration effectiveness and include beneficial ownership limitations designed to prevent excessive concentration [S13][S16][S18].

PIPE proceeds inject substantive additional liquidity which will underpin initial operating capacity post-close alongside support for strategic initiatives tied to integration and expansion [S6][S7][S26]. However, despite liquidity strengths on hand currently managing cash flows remains critical given ongoing investment needs anticipated after conversion into an operating company.

Execution Risks and Regulatory Considerations for Deal Closure

Legato explicitly highlights several material risks impacting successful closure including regulatory approvals both domestic and international given Einride's Swedish incorporation; shareholder approval processes; potential litigation arising from deal announcements; and termination rights embedded in the Business Combination Agreement itself [S4]. These factors represent common frictions faced by SPAC mergers but are intensified here by valuation revisions and uncertainty surrounding Einride's scalability.

Market volatility may also influence redemptions which if significant could jeopardize funding sufficiency or trigger adverse adjustments [S4]. Additionally maintenance on listing status involves exchange reviews that necessitate compliance with qualitative and quantitative criteria post-combination—a hurdle that has upended some similar deals recently across sectors.

Post-Merger Growth Outlook and Strategic Constraints

Future growth narratives center around the combined entity’s ability to leverage Einride’s technological offerings within its addressable markets primarily indicated as transport automation though specifics lack clarity [N/A meta]. The PIPE capital infusion provides runway for U.S market entry plans explicitly noted during subscription agreements discussions emphasizing geo-geared expansion.

While no explicit forecasts or guidance accompany filings to date nor detailed synergy quantifications are available—the fundamental strategy pivots on transitioning from shell vehicle status into executing operational scale with anticipated revenue generation emerging post completion [N/A meta]. Absence of disclosed historic revenues or margins constrains thorough analysis rendering growth outlook speculative beyond stated intentions.

Capital Allocation Strategy and Shareholder Returns Prospects

Legato maintains no declared dividend policy or share repurchase program consistent with standard SPAC behavior pre-deal completion given reinvestment priorities dominate capital deployment decisions currently documented [F1][S5][S14].

ROE computed using latest net income relative to negative equity stands near minus 130%, reflecting early-stage accumulation of structural deficits typical before business combination closure when recorded equity reduces through share redemption rights exercised by public investors as appropriate [F1].

Capital preservation through liquidity maintenance is paramount until merged operations generate positive returns supporting possible future distributions or buybacks—which remain unaddressed publicly currently reflecting ongoing transformation phase rather than mature capital return strategy.

Critical Milestones and Market Expectations Moving Forward

Key upcoming events focus squarely on shareholder vote timelines for transaction approval following issuance of definitive Proxy Statement/Prospectus expected imminently post-registration effectiveness [S14][N/A meta]. Concurrent closing deadlines are reliant upon satisfying all contractual conditions precedent notably regulatory clearances.

Post-close monitoring should emphasize quarterly filing updates for signs of integration progress markers along with adherence to exchange listing obligations monitored closely given market sensitivities towards SPAC deals broadly recently [N/A meta][S14]. Investors should also track warrant exercise prices adjustment triggers tied to ADS trading performance impacting capital structure dynamics further downstream.

Disclaimer: This report is intended solely for informational purposes reflecting Legato Merger Corp. III's available financial disclosures and public filings as of April 2026 without offering investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments