Tofutti Brands Faces Operational Disruption as Co-Packer Plant Closure Threatens Growth and Liquidity

The company’s reliance on a primary co-packer representing 80% of sales, combined with ongoing losses and supply chain risks, challenges its growth trajectory and financial stability.

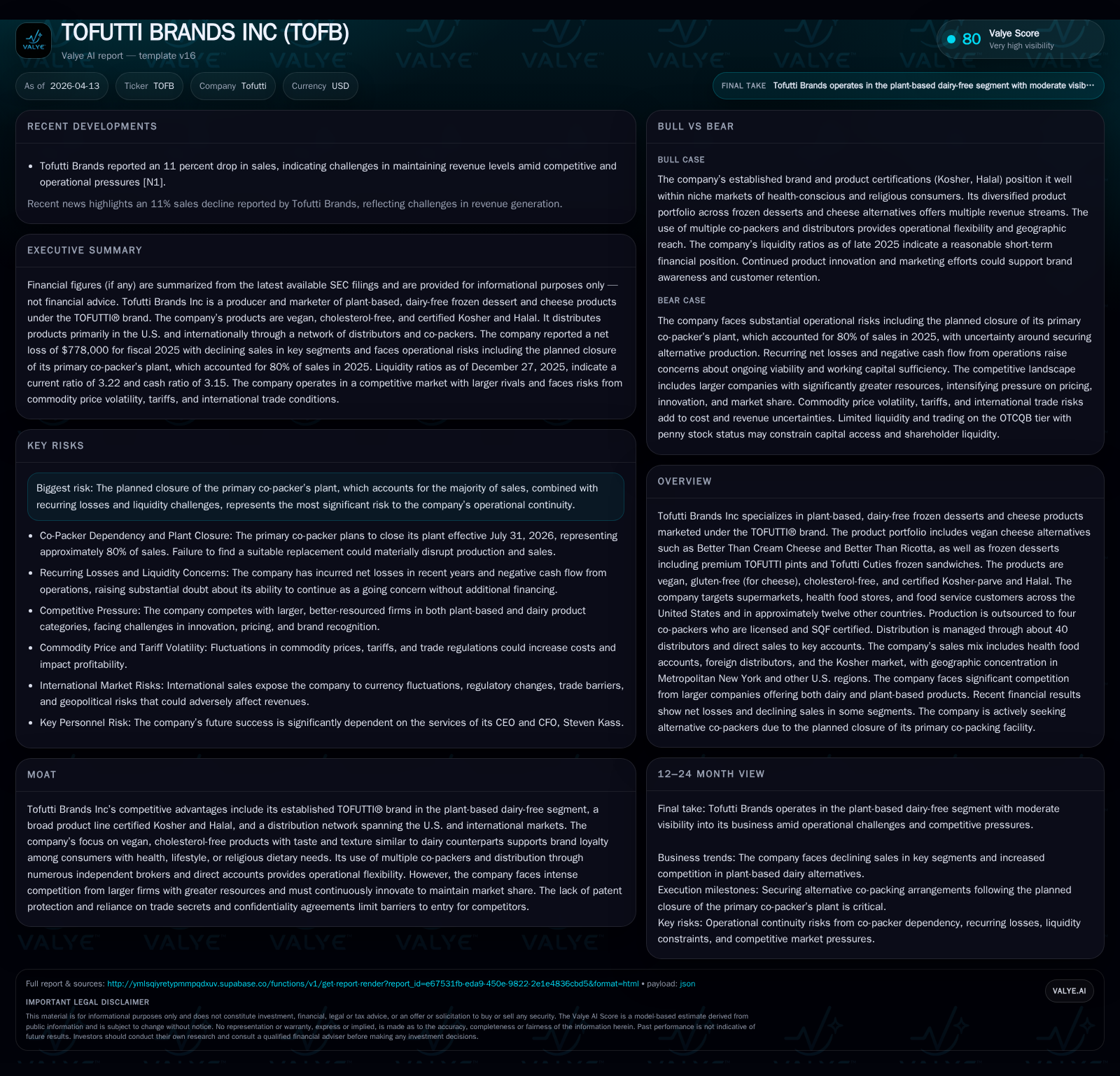

Tofutti Brands Inc, a niche player in plant-based dairy-free frozen desserts and cheeses, reported approximately $14 million in revenue in prior years but has experienced recurring operating losses and negative cash flows through 2025 [F1]. Its core competitive advantages include an established vegan brand with kosher and halal certification and a diverse distribution network spanning the US and international markets [S22][S8]. However, the announced closure of its primary co-packing partner’s production facility in July 2026, which produced roughly 80% of its product volume, poses a significant operational risk and casts doubt on the company's ability to maintain supply continuity [S1]. The company must secure alternative manufacturing arrangements while managing increased cost pressures from commodity volatility and competitive threats amid limited financial resources. With net losses totaling $778,000 in fiscal 2025 and only $347,000 cash on hand at year-end per narrative disclosures [F1][S1], Tofutti’s liquidity situation warrants close monitoring.

Company Overview

Tofutti Brands Inc operates within the plant-based dairy-free segment, manufacturing a range of vegan frozen desserts and cheese substitutes under the TOFUTTI® brand. Founded in the early 1980s and incorporated in Delaware since 1984, Tofutti emphasizes products free from butterfat and cholesterol—primarily formulated with soy and vegetable proteins such as corn and palm oils. Their product portfolio includes hallmark lines like BETTER THAN CREAM CHEESE® available in multiple flavors and formats suited for retail and food service customers. The cheese products are gluten-free while all offerings possess kosher-parve certifications; most cheese items plus popular frozen novelties like Tofutti Cuties also carry halal certification.

The firm relies entirely on third-party co-packers for production—to comply with strict quality standards including Safe Quality Food (SQF) certification—and distributes products through a network of some forty distributors alongside direct sales to key grocery chains domestically. International presence extends to roughly a dozen countries via exports handled entirely in USD transactions.

Historical Financial Performance

While consistent revenue figures close to $14 million per annum since mid-2010s indicate steady albeit slow growth, margins have been under pressure as costs outpaced pricing adjustments. According to latest filings:

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -778000 | -98000 | -773000 | +9.5% |

| 2024 | -860000 | -358000 | -607000 | -135.0% |

| 2023 | -366000 | -225000 | -238000 | +30.3% |

| 2022 | -525000 | -616000 | -916000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -35.2 |

| 2024 | -28.8 |

| 2023 | -9.7 |

| 2022 | -12.8 |

Source: SEC companyfacts cache [F1].

Operating losses widened from -$607k in FY2024 to nearly -$773k in FY2025 despite efforts at cost discipline. Net losses improved marginally likely due to changes in non-operating items or tax effects but remain substantial relative to equity base. Operating cash flow improved significantly from negative $358k to negative $98k suggesting tighter working capital management or reduced business activity.

Current assets at approximately $3 million versus liabilities under $1 million provide a current ratio above three times — indicating short-term liquidity but reflecting mostly receivables/inventory rather than cash reserves. The company held only approximately $347,000 cash at end-2025 per narrative disclosures [S1], underscoring tight liquidity.

Equity has steadily declined over the past three years indicating sustained operating deficits eroding capital.

Growth Drivers and Challenges

Drivers

Tofutti’s growth strategy focuses on expanding penetration among consumers motivated by health (cholesterol-free), lifestyle (vegan), or religious (kosher/halal) priorities. The expansion of plant-based diets nationally combined with growing ethnic markets supporting kosher or halal consumption underpin target consumer segments.

Product innovation continues albeit on a smaller scale than major competitors; marketing efforts rely heavily on word-of-mouth supported by selective trade advertising aiming at natural food stores, supermarket chains with natural foods sections, and foodservice clients.

International sales comprised about 15% of revenues in FY2025 spread across markets including Canada, Australia, Israel, Mexico, France among others—offering diversification potential [S8][S20].

Constraints

However crucial hurdles constrain growth notably:

- Manufacturing Concentration Risk: Approximately half of finished goods come from Franklin Foods co-packer which produces about four-fifths of total volume. Their announced shutdown effective July 31, 2026 creates existential challenges for supply continuity unless suitable alternative partners are onboarded swiftly—a non-trivial undertaking given SQF certification requirements and capacity constraints inland [S1][S26].

- Competition: Larger companies with scale aggressively introduce sophisticated vegan dairy alternatives pressuring TOFUTTI's market share especially in cheese substitutes which historically were drivers but have weakened under competitive incursions [S20][S14].

- Commodity Inflation: Elevated raw material costs (soy protein concentrates, oils) coupled with tariff uncertainties inflate input prices unpredictably. While Tofutti has raised prices somewhat responsively, margin compression remains an ongoing risk given price-sensitive retail environments [S24][S25].

- Financial Constraints: Recurring negative operating cash flows limit marketing budget flexibility required for brand building or new product launches. Reduced working capital restricts promotional activities crucial for defending shelf space against private label incursions and new entrants.

- Regulatory & Safety Risks: Stringent compliance with FDA labeling rules plus emerging food safety standards impose incremental operational overheads that may disproportionately impact smaller producers reliant on outsourced manufacturing setups [S15][S18].

Returns & Capital Allocation

Historically Tofutti has not paid dividends nor undertaken material share repurchases reflecting prioritization of retaining capital to support operations amid profitability struggles [F1][S19].

Return on equity remains negative at an approximate -35% based on FY2025 net loss versus equity narrowed to $2.2 million. Operating cash flows remain negative although improving slightly toward breakeven—free cash flow estimate near negative $127k after minimal capex investment signals ongoing cash burn requiring external support if unaddressed long-term [F1].

Capital expenditures are nominal since production assets reside with contract manufacturers.

The controlling shareholder retains dominant voting power providing governance stability yet potentially limiting external strategic alternatives including mergers or acquisitions meant to address liquidity gaps [S27].

Outlook & Monitoring Points

No explicit forward guidance or formal revenue targets have been provided amidst evident liquidity concerns and uncertainty around transition post-primary co-packer exit. Key milestones investors should monitor include:

- Announcement of agreements with new SQF certified co-packing partners capable of absorbing volumes displaced by Franklin Foods’ plant closure.

- Stability or improvement in monthly shipment volumes post-July 2026 representing successful operational continuity.

- Trends in international sales particularly if expansion into global plant-based segments accelerates.

- Any capital raises or strategic partnerships addressing working capital shortages given weak free cash flow performance.

- Effectiveness of cost pass-through measures against inflation-driven input increases maintaining gross margins.

Absent such developments, continued operating losses due to fixed overhead absorption challenges combined with competitive pressure limiting pricing power appear likely.

This report is for informational purposes only and does not constitute investment advice or recommendations regarding securities issued by Tofutti Brands Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments