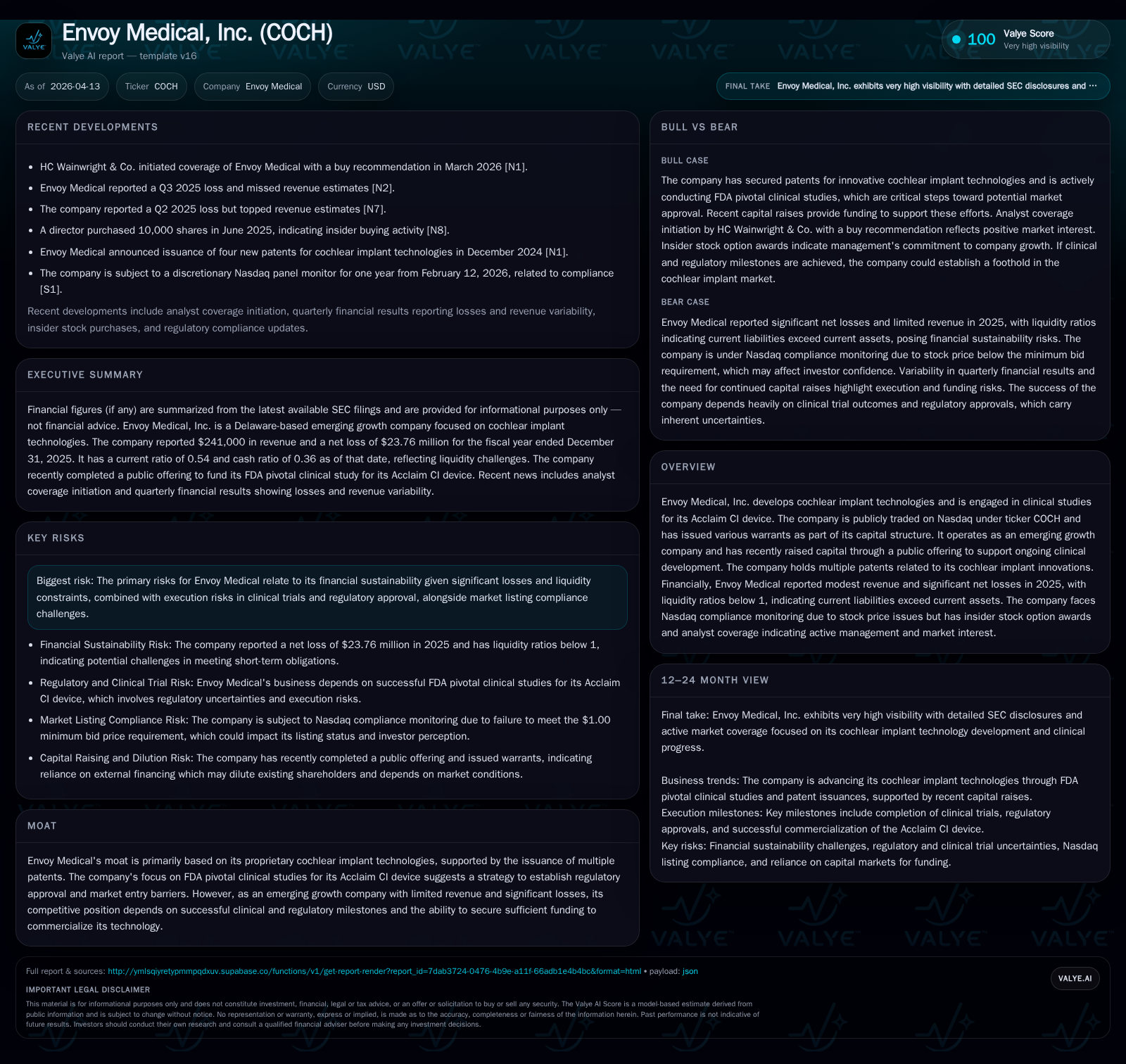

Envoy Medical's Path to Commercializing Innovative Cochlear Implant Technology

Envoy Medical advances its Acclaim CI device through FDA pivotal trials while managing capital raises and liquidity challenges.

Envoy Medical, Inc. operates as an emerging player developing patented cochlear implant technology centered on its Acclaim CI device currently in pivotal FDA clinical studies. Despite minimal revenue and heavy losses totaling over $23 million in 2025, the company has raised approximately $30 million through equity offerings and associated warrants to fund ongoing trial activities. Liquidity constraints reflected in a sub-one current ratio and Nasdaq stock price compliance monitoring underscore operational risks. Capital allocation reveals continued dividend payments despite negative free cash flow, highlighting tensions between shareholder returns and financing needs. Key near-term catalysts include regulatory milestones tied to clinical trial progress, pivotal for transition toward commercialization.

Track Record of Development: Revenue and Loss Trends

Envoy Medical's financial trajectory reflects a classic emerging biotechnology profile characterized by minimal revenue generation and steep operational investment. Fiscal year (FY) 2025 recorded revenues just above two hundred forty thousand dollars ($241K), showing modest growth of roughly 7% year-over-year from FY2024's $225K but representing a decline from FY2023’s higher $316K levels [F1]. Concurrently, the company recorded significant operating losses expanding from $19.3 million in FY2024 to $22.3 million in FY2025—a deterioration of nearly 16%—reflecting intensifying R&D efforts centered on its Acclaim cochlear implant technology [F1]. Net losses followed a similar trend, deepening by about 14% year-over-year to nearly $23.8 million.

Operating cash flows (CFO) remain deeply negative around -$18.2 million in FY2025 with a sharp drop in capital expenditures (capex) suggesting clinical trial-focused spending rather than physical asset investments [F1]. The latest fiscal data capture Envoy’s heavily developmental-stage status with lack of scale in commercial revenues yet sizable expenses underpinning innovation and impending regulatory submissions.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 241000 | -24 | -18 | -22 | +7.1% | -14.2% |

| 2024 | 225000 | -21 | -18 | -19 | -28.8% | +30.5% |

| 2023 | 316000 | -30 | -18 | -18 | -255.5% | |

| 2022 | 19 | -3 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 2 | -18 | 195.4 |

| 2024 | 2 | -19 | 110.4 |

| 2023 | -18 | 1697.4 | |

| 2022 | -107.4 |

Source: SEC companyfacts cache [F1].

The moderate revenue trajectory coupled with steep losses indicates heavy investment phase ahead of any commercial launch.

Clinical Advances in the Acclaim CI Device and Regulatory Journey

Envoy’s foundational value proposition rests on the Acclaim cochlear implant system—a patent-protected acoustoelectric innovation that aims to improve auditory outcomes for patients suffering hearing loss [N1][S1]. The device is actively enrolled in pivotal FDA clinical trials intended to generate necessary evidence for marketing approval under the Premarket Approval pathway.

This phase is critical; success would provide Envoy with a regulatory moat reinforced by its IP portfolio encompassing multiple issued patents covering novel aspects of cochlear implant design [S1]. However, this period also presents substantial execution risks typical of medical device clinical developments—ranging from enrollment challenges to achieving clinically meaningful results acceptable for FDA standards.

Progressing through these trials is paramount not only for validating the device’s therapeutic claims but also locking in first-mover advantages within the ultra-competitive neurotology implant market where incumbents continuously innovate around signal processing and biomaterials integration.

Capital Raises Fueling Trials: Overview of Recent Financings and Warrants

To sustain costly clinical trial operations without meaningful product sales revenue, Envoy has intermittently tapped public markets since late 2025 [S4][S5][S6][S8][S20]. Its latest equity raise concluded around February 2026 comprised common stock issuance alongside complex warrant instruments totaling gross proceeds near $30 million upfront.

These financings include pre-funded warrants exercisable at nominal prices alongside Series A-1 and A-2 warrants priced at higher strike points ($11.50) strategically engineered to incentivize eventual conversion upon successful trial milestones or market uplisting events.

Notably underlying these offerings are restrictive ownership clauses limiting beneficial ownership percentages for large investors to preserve orderly share distribution—a common protective structure that may mildly constrain liquidity but reflects measured governance execution amid volatility risks.

Should all warrants convert fully—which remains uncertain—the company could realize an additional substantial inflow approaching $48 million [S4], crucial given ongoing negative cash flow trends.

Liquidity Constraints and Nasdaq Compliance Risks

Despite recent capital influxes Envoy operates under tight liquidity conditions with financial statements revealing only about $6.3 million in current assets against liabilities nearly double at $11.6 million as of December 31, 2025—a current ratio near 0.54 evidencing pronounced short-term funding risk [F1][S29].

Adding pressure is Nasdaq’s formal compliance monitoring triggered by sustained share price dips below minimum required thresholds ($1 per share), although the company has engaged mechanisms including panel monitors aimed at restoring compliance over provided grace periods extending into mid-2026 [S24].[S25]

Failure to regain compliance could impair trading status or restrict access to institutional investors emphasizing listing rule adherence—factors integral to future capital raising endeavors.

Analyzing Capital Allocation: Dividends, Share Repurchases, and Cash Flow Dynamics

While generally unexpected for early-stage development firms facing continuous net losses exceeding $23 million annually with negative free cash flow close to -$18.4 million (operating cash flow minus capex), Envoy paid dividends amounting to approximately $1.82 million during FY2025 [F1][S6][S7][S16].

The rationale behind dividend distributions amid constrained cash resources suggests a balancing act by management targeting investor confidence or fulfilling legacy obligations rather than strategic shareholder returns typical at this stage.

Furthermore, capex reductions from nearly one million USD in FY2024 down to approximately $179K in FY2025 align with a shift towards clinical spending focus rather than new physical assets expansion.

The combined picture reveals prioritization of financing clinical milestones over aggressive infrastructure investments or buybacks reflecting capital discipline aligned with emergent growth phases.

Upcoming Catalysts: What to Watch in Regulatory Milestones and Market Approval

Critical forthcoming events include interim readouts from ongoing pivotal FDA studies on the Acclaim device as well as subsequent submission timelines for formal premarket approval applications—milestones explicitly linked with warrant exercise triggers per offering agreements [N1][S1][S10].

Given the novelty of cochlear implant systems competing on both surgical ease and auditory fidelity enhancement fronts, any positive regulatory feedback could substantially validate Envoy’s commercial strategy enabling a pivot into initial sales channels under a cleared market authorization blueprint.

Monitoring announcements regarding patient enrollment completion rates or safety/efficacy endpoints will prove essential barometers for stakeholder validation going forward.

Balancing Innovation with Financial Discipline: Capital Structure Risks and Strategic Outlook

Envoy's capital structure represents considerable dilution risk stemming from numerous outstanding warrants paired with evolving equity layers which while vital for sustaining operations dilute existing shareholders.

At end-2025 equity sits negatively at approximately -$12.2 million contrasting against significant losses constraining traditional return metrics—albeit ROE remains inflated artifactually due to denominator effects within deficit-equity situations [F1].

However,the recent issuance of insider stock options including significant grants to the CEO and interim CFO signals internal confidence alignment aiming to motivate performance towards milestone achievements that fuel valuation inflection [S18].

Going forward the balance between successfully navigating regulatory approvals while managing resultant capital demands against Nasdaq listing pressures forms the centerpiece strategic tension defining Envoy's pathway toward transforming cochlear implant innovation into commercial presence.

This report synthesizes public filings including SEC documents and market commentary without suggesting investment positions or forecasts beyond documented disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments