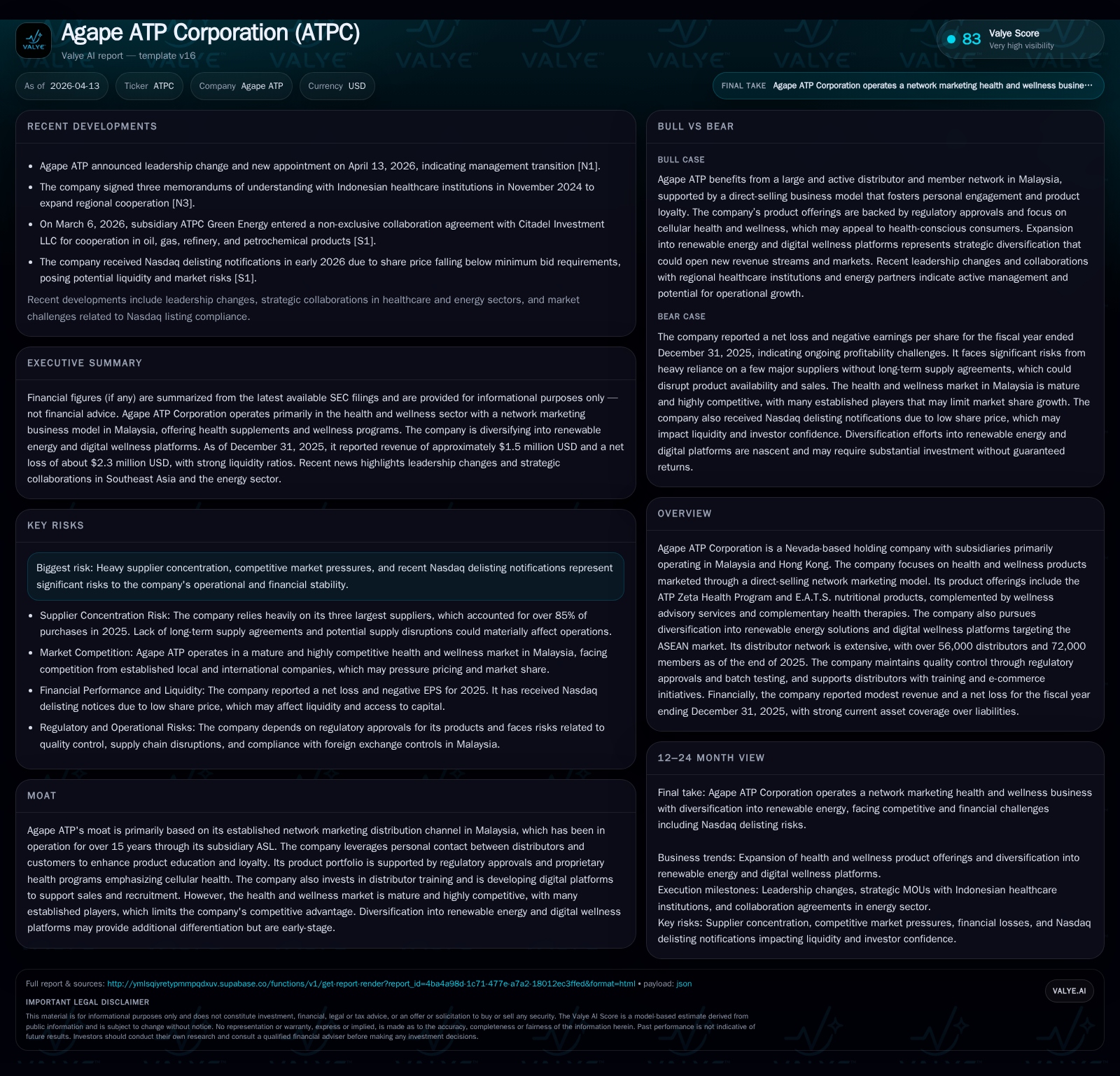

Agape ATP Corp’s Struggle with Profitability Amid Expanding Distributor Base

Agape ATP balances its entrenched health network marketing growth with emerging renewable energy ventures under mounting financial pressures and supplier dependencies.

Agape ATP Corp has built and expanded a substantial direct-selling network in Malaysia’s health and wellness space, reaching over 56,000 distributors by the end of 2025. Despite top-line growth driven by this expanding network, the company continues to report sizable operating losses and cash burn, highlighting challenges in converting scale into profitability. Supplier concentration risk remains significant with no long-term contracts, adding vulnerability to supply disruptions. Simultaneously, Agape ATP is embarking on a nascent diversification into renewable energy solutions, though these remain early-stage ventures without material financial impact yet. The company faces critical near-term milestones around stabilizing supply chains, advancing green initiatives, and navigating leadership changes amid Nasdaq delisting notifications.

Network Marketing Roots: Historical Growth and Revenue Trends

Agape ATP Corp operates primarily through its Malaysian subsidiary Agape Superior Living Sdn. Bhd. (ASL), which has maintained a network marketing distribution model exceeding 15 years according to SEC filings [S1][S12]. Its portfolio centers around health supplements like the ATP Zeta Health Program and E.A.T.S nutritional products designed for cell metabolism enhancement, detoxification, improved blood circulation, and anti-aging benefits [S8]. This model depends heavily on personal contact fostering distributor loyalty and sales.

The company reported sequential revenue fluctuations from FY2022 through FY2025 with an initial decline from $1.86 million in FY2022 down to $1.43 million in FY2023 before rebounding to $1.32 million in FY2024 and expanding again to $1.52 million by the end of FY2025 (a 15.2% YoY increase) [F1]. This volatility contrasts with steady growth in the distributor base that reached over 56,000 distributors and a total combined membership exceeding 128,600 across Malaysia by December 31, 2025 [S20]. A membership discount program incentivizes customer conversion into distributors upon achieving purchase thresholds [S20]. In addition to direct selling branches in Kuala Lumpur and Ipoh, product distribution leverages independent stockists whose inventory performance is centrally monitored via proprietary stock tracking systems [S7][S12].

Despite seasonal neutrality stated by management [S7], revenue oscillations suggest that challenges such as market competition or consumer spending patterns are influencing sales momentum even as distributor recruitment expands.

Financial Struggles Despite Scaling Distributor Network

The operating income trajectory signals deepening losses through four consecutive years ending FY2025: a loss widened from approximately $-1.53 million in FY2022 to $-3.26 million or a -26.6% worsening YoY from FY2024 to FY2025 [F1]. Net income figures modestly improved from a loss of nearly $-2.47 million in FY2024 to $-2.28 million in FY2025 (+7.7%), partially reflecting non-operating items or expense reclassifications [F1]. Nonetheless, ongoing losses illustrate difficulties converting growth into profitability.

Operating cash flow trends reinforce liquidity challenges; CFO burned nearly $2.41 million in FY2025 despite slight improvement over the prior year’s deficit ($-2.73 million) [F1]. These negative cash flows typify capital inefficiency common within direct selling companies confronted with inventory load, return policies offering satisfaction guarantees within ninety days [S7], and timing mismatches between receivables and payables.

Agape ATP's return on equity (ROE) is calculated at approximately -10% for FY2025 based on net loss relative to reported equity levels [$22.46 million] reflecting unremediated operational losses at scale [F1]. This negative profitability underscores that expansion costs including distributor incentives, training programs, e-commerce upgrades, and product testing requirements are outpacing revenue gains [S8][S12][S13].

Supplier Concentration Risks Undermining Stability

A significant operational risk emanates from supplier dependency concentration detailed for FY2025: three suppliers accounted respectively for approximately 55.6%, 20.3%, and 11.1% of total purchases amounting collectively to $572k USD of total procurement cost [S1][S5]. Notably, no long-term supply agreements exist with these key providers; purchase orders are placed ad hoc leading to potential disruptions.

This leaves Agape vulnerable to any supply chain interruption caused by labor disputes, pandemics affecting supplier facilities, or changes in export strategies which could delay product availability or increase input costs [S1][S5]. Delays inherently affect downstream deliveries to customers thereby impacting working capital cycles adversely given delayed receivables versus fixed payment obligations [S1]. Moreover, risks that suppliers could appoint competitors as additional dealers or increase prices limit Agape's bargaining power with repercussions for gross margin control.

Such supplier risks amplify the competitive challenges the company faces within Malaysia's mature wellness segment where brand perception is tightly linked to consistent product quality adherence enforced via Ministry of Health certifications [S8][S12][S26].

Diversification into Renewable Energy: Early Steps and Strategic Intent

In an apparent move toward sustainability-driven diversification, Agape ATP established ATPC Green Energy Sdn. Bhd., wholly owned since March 14, 2024 (formerly OIE ATPC Holdings), focusing on solar power generation, energy management systems, storage solutions for commercial clients across industry sectors within Malaysia [S4][S6]. This segment is positioned as complementary but is nascent with limited disclosure on financial impact thus far.

The strategic rationale centers on environmental responsibility coupled with long-term value creation aligned with ASEAN markets’ increasing commitment toward green energy transition goals [S4]. Partnerships extend across government bodies and technology firms compliant with international sustainability standards serve as foundational pillars for this venture [S4]. However due to its infancy stage and absence of measurable revenues or profits attributable directly to this sector at present time per latest filing [F1], its role remains largely aspirational.

Digital Wellness Platform: Potential Growth Driver or Distraction?

Augmenting traditional direct selling channels with digital innovation, Agape has developed digital wellness initiatives through Cedar ATPC Sdn. Bhd., previously Wellness ATP International Holdings Sdn. Bhd., launched in September 2020 to promote community-wide wellness lifestyles via online editorial content, wellness campaigns, programs, and events targeting engagement enhancement [S8][S12].

Further efforts include investments made since 2019 toward an e-commerce platform facilitating online product sales along with distributor recruitment functionalities intended for national scalability once proven successful locally [S7][S8]. The integration aims to address modern retail trends where omnichannel access enhances distributor retention rates—a key metric within network marketing ecosystems often correlated with sustainable organic growth provided support infrastructure is adequate.

Nevertheless, these technological developments require upfront resources while core business segments struggle financially raising questions whether such diversification represents an innovative competitive edge or diverts limited capital away from operational stabilization.

Capital Deployment, Returns, and Shareholder Considerations

The following table summarizes key fiscal indicators from FY2022 through FY2025 consolidating revenue trajectories alongside profitability measures and cash generation:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1524262 | -2 | -2 | -3 | +15.2% | +7.7% |

| 2024 | 1322747 | -2 | -3 | -3 | -7.6% | -17.5% |

| 2023 | 1431088 | -2 | -2 | -2 | -22.9% | -24.6% |

| 2022 | 1856564 | -2 | -1 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | -10.2 | |

| 2024 | 93889 | -127.8 |

| 2023 | 93889 | -48.1 |

| 2022 | -109.4 |

Source: SEC companyfacts cache [F1].

No dividends were declared over this period nor material capital expenditure reported beyond nominal amounts preceding FY2022 filings indicating conservative investment posture amid operating strains [F1]. Buyback programs occurred modestly (~$94k per annum) during calendar years overlapping fiscal periods ending December 31 of FYs 2023 and 2024 but likely insufficient given ongoing negative cash flows contextually signaling cautious shareholder distributions prioritizing liquidity preservation [F1]. Equity surged significantly between FY2024 ($1.93 million) and FY2025 ($22.46 million), probably driven by share issuance or other equity transactions unrelated directly to earnings improvements given simultaneous rising losses recorded [F1].

This dynamic frustrates shareholder value creation objectives short term though may better hedge against balance sheet deterioration amidst liquidity risks noted as the current ratio stands strongly above one (>11x), suggesting comfortable short-term asset coverage but not necessarily translating into positive free cash flow given operating inefficiencies.

What to Watch Next: Milestones and Market Signals

Critical near-term developments include progress updates on renewable energy project rollouts within Malaysia’s commercial sectors where government incentive policies may accelerate adoption rates if executed timely; digital platform traffic metrics measuring user acquisition velocity post-launch will be instrumental gauge points demonstrating response efficacy; monitoring supply chain contracts or alternate sourcing arrangements will be paramount given existing supplier concentration vulnerability hindering operational predictability.

Leadership transitions announced publicly in April 2026 may pivot company strategy or accelerate restructuring efforts aimed at restoring Nasdaq compliance post notices received earlier in calendar Q12026 [N1][S3]. No explicit forward guidance has been issued emphasizing conservative anticipation scenarios subject heavily to macroeconomic conditions within Malaysia alongside global health supplement competitive pressures maintaining considerable challenges ahead.

Overall trajectory hinges on balancing legacy network marketing strength against the expensive demands of emerging business verticals while addressing fundamental cost structure troubles intensified by concentrated suppliers—execution outcomes here will define sustainability prospects over the medium term.

This analysis synthesizes available disclosures without presuming undisclosed company plans or speculating beyond reported data points respecting regulatory filing constraints.[F1][N1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments